2013 was a banner year for returns in all asset classes (except bonds!). It was the triumph of the central banks as debt and deleveraging crises worldwide subsided, financial repression and liquidity reigned, and the great rotation from defensive assets to cyclical and risk plays dominated returns.

Coming in to the year, stock markets had recovered some of the deep sell offs of the global financial crisis, but it was this year that they began to discount a real recovery in the global economy. Property markets in developed economies joined them. The developed economy recovery meme put a sizable dent in yesteryear’s boom theme of emerging markets growth as they too fell before the great rotation via jumping bond yields.

It was such a strong year for developed market asset classes, in fact, that the question is now rightly being asked, have we returned to our pre-crisis bubble condition?

The answer to that depends upon whether or not you believe the underlying story. Are developed economies recovering and able to deliver high earnings growth that will rationalise this year’s higher valuations?

There are two answers to that question which are contradictory and both are right.

The first is “yes”. In cyclical terms, the US, UK, European and Japanese economies are all better placed going into 2014 than they were 2013. The US especially may creep closer to a respectable 3% growth, at least for a little while. That will boost profits, although it’s hard to see margins improving any further as we move deeper into the cycle and employment improves. Europe and the UK are also clearly recovering although their growth prospects are lower than those of the US. Japan looks like a star at this point as its reflation policies work in the short term.

The second answer is “no”. In structural terms, we are nowhere near healthy economies and sustainable growth. The US has passed the low point of its private sector develeraging but in front of it stretches the near endless task of stabilising deep (but improving) budget deficits. The UK has engineered a renewed housing and consumption surge that only proves it has nothing else to offer. Europe is worse still, with its structural problems half resolved through a spaghetti bowl of cross-border agreements on bank and fiscal equalisation that is nowhere near a functional Federation despite the ongoing pressures of a single currency and monetary policy. Japan has engaged in a radical monetary policy experiment that has trashed its own currency and re-inflated exports. And behind all of that, the deflationary pressures emanating from emerging markets, who are still able to produce everything from sneakers to rockets at a fraction of the price of the West, has everyone neck deep in currency wars.

These structural inhibitions are played out most obviously in the need for zero interest rates which give the appearance of a recovery.

So, the question one must ask going into 2014 is which of these two answers will hold sway for the next year? Will it be the cyclical momentum that is currently apparent? Or will it be the structural headwinds that have slowed only marginally? My view is that it is the former for 2014.

The cycle wins

What does that mean for assets? If cyclical momentum wins through, the shift towards stocks from defensive asset classes will continue. Within stock markets, the general shift towards cyclicals and growth stocks will also resume.

But it won’t be smooth. Certainly not as smooth as this year. The major macro theme for the year ahead will be the challenge of “policy normalisation”. That is, central banks in the US, the UK and, to a lesser extent in Europe and Japan, will toy with exits from extraordinary monetary support. Stock markets will have to climb a “wall of worry” around interest rate tightening, as muted as it will be.

The key will be the US Treasury market, where falling prices have already pushed yields up on the 30 year bond to almost 4% from 2.5% in late 2012. Most US mortgages are fixed rate and bench-marked to this bond rate so prospective buyers of US housing have already faced the equivalent of six typical Australian rate hikes in a year. Not surprisingly, US housing is slowing and its prospects are one of my key risks in the year ahead.

If the Fed tapers its bond purchases, and an attempt seems probable, then the 30 year yield will rise further, to around 4.5%. That is likely too high to sustain US house price rises and its recovery will stall, meaning the Fed will either have to slow its tapering or reverse it.

I expect stock markets will shift around these movements in US monetary policy and housing but of one thing we can be fairly certain, if asset prices falter, the Fed will resume its quantitative easing program with gusto and so in the main I see the S&P500 higher over the year.

Of course, if I’m wrong, and growth disappoints sooner, there will be no taper then the S&P will be higher anyway.

It is a bald-faced play on the Bernanke/Yellen “put”.

Australia is different

In theory you would expect Australian stocks to benefit from a bullish S&P500. But increasingly that is not the case. For two years, Australian stocks have been diverging from the tearaway returns on Wall St. Our more subdued performance has been the result of an over-weaning attachment to China, which is sliding as developed economies rise.

While our domestic cyclical sectors have been enjoying stellar valuation improvements on interest rate cuts, the huge resources sector has been punished as China has slowed. The other big market segment, the banks, has manged to straddle the divide as it has moved from a defensive yield play in difficult times to a growth play on a credit recovery theme.

Whether this split between Australia and other developed market returns continues in 2014 is the key question one must ask of the Australian market. I think it probably will. There are three reasons why.

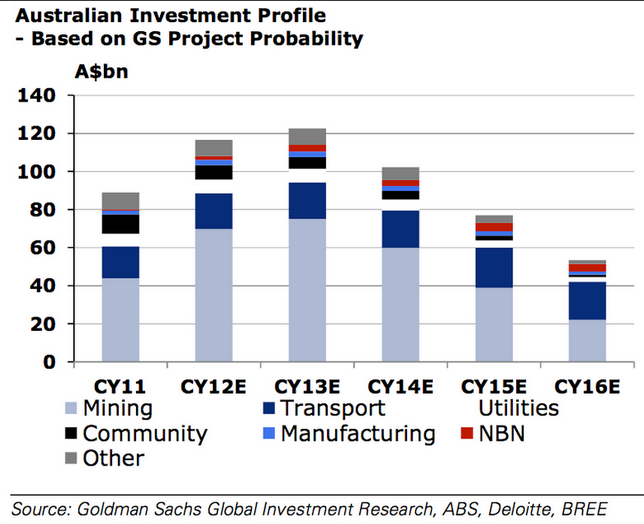

First, Australian growth faces a torrid time in 2014. The year ahead will be dominated by falling mining and related investment. It’s impossible to pinpoint how much and how fast but it is definitely coming and over the next few years is going to tumble from 8% of GDP to probably 2%. Needless to say that is an enormous downdraft. I could mount a case that it will be worse in 2015, largely because the LNG projects that are being completed are showing such huge cost blowouts that they self-replenish the capex pipeline, but it doesn’t really matter. The capex cliff is before us. We will go over it next year and that will keep growth materially below trend. The following Goldman Sachs chart sums it up neatly:

There is no hope of non-mining sectors filling the business investment hole for the next two years and probably not in the third year either with Ford and Holden leaving, though public investment will kick in strongly in 2016 to make up the difference.

The majority of analysts still see growth at a decent at 2-2.5%, largely because of the so-called “third phase” of the mining boom, when construction turns to production. And they’re right that net exports will be a potent driver of growth, just as it was in the past year contributing 1.9% of our 2.3%. But even if the headline figure is reasonable, the internals will be very painful for households because this composition of growth does not support employment. As unemployment rises, cyclical stocks will struggle to deliver high profit growth.

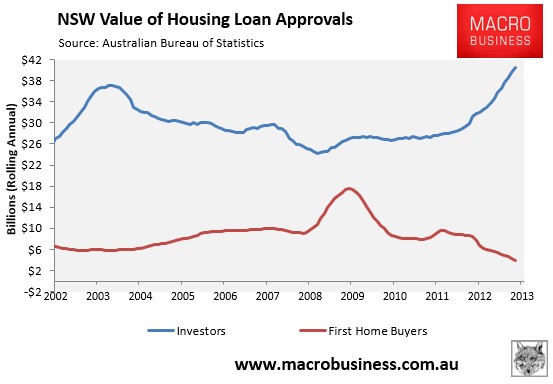

The second reason that Australian stocks will struggle to match the US is that the Reserve Bank’s attempt to rebalance the economy away from this mining investment cliff is building a nasty imbalance in the Sydney property market, without producing much of a growth dividend in return. Although the RBA is putting a brave face on its campaign to reinvigorate housing construction, it is largely failing outside of apartments. But not so with Sydney house prices, where the speculative horse has well and truly bolted:

The RBA cannot and will not raise interest rates because it desperately needs a lower dollar to stimulate investment in tradable sectors to fill the mining hole (it needs 80 cents at least and probably 70 cents). Instead the RBA’s incipient jawboning campaign is likely to ramp to up to a near scream next year as it attacks the dollar carry traders. The campaign will increasingly take in property investors as well and you can expect much more talk of macroprudential policy (LVR speed limits and the like) in an attempt to subdue Sydney’s property maniacs without hiking rates. The bank is loath to install such tools but will be forced to if property does not slow in Sydney.

You can add to this fiscal instability as the new Liberal Government identifies and then addresses a huge deficit.

Thus consumers are going to be pushed and pulled by authorities’ efforts to control what they’ve unleashed. I expect only a modest loosening of the purse strings in households.

The third reason Australian returns are likely to lag the US is that the Chinese rebalancing so often discussed remains an open question. Markets have been happy to give Chinese growth some benefit of the doubt since the Plenum announced many liberalisation measures aimed at catapulting China out of the “middle income trap”.

But the fact remains, if they are going to unleash the consumer, China will have to endure painful restructuring in its fixed asset investment economy, which has been its major past growth driver. There is no way around this. To boost household incomes, interest rates must rise. But to raise interest rates will expose the bad debts that have funded so much dodgy infrastructure.

China has ways of recapilising its banks that the West does not so I don’t expect a credit crunch leading to a crash. But activity will fall if they are serious about rebalancing and any attempt to support the process with stimulus (that is, more building) means, by definition, no rebalancing.

This year’s 2 trillion yuan stimulus is passing. Chinese growth is going to slow in the first half of next year as the infrastructure pipeline empties. Will it be replenished again? A pragmatist might say “yes”. An historian may say “no”. We still don’t know which the new Chinese leaders are, though they tell us they’re the latter. If so, as Australia’s iron ore supply deluge builds to a crescendo in Q2 next year, the pillar of Australian exports strength will crash, and with it, the economy.

Conclusion

A decent rally in Australian stocks is possible next year. The sell side bulls that dominate commentary are pushing for 6000 points as the consumer rebounds with housing and growth stocks lead the way. This discounts the structural headwinds I’ve described almost completely.

A much better risk reward equation lies in playing the Australian dollar. One way or another the dollar must fall. Either the RBA will be able to muscle it down past 80 cents earlier, or the economy will remain weak enough that interest rate cuts will do it later. As well, the dollar will fall materially in the event that a shock hits global share markets so it’s a built-in hedge for offshore stock market investors. If all goes well it will amplify capital gains as the currency falls.

Local investors should tread very carefully. Cyclical and growth stocks will be the play, as will dollar-exposed industrials (not miners). But so long as the capex cliff falls away beneath us, there is an unusually high risk of a real recession overtaking the Australian economy in the event of a shock.

This article was composed for Intelligent Investor and does not, as always, constitute investment advice.

—————————————————————————————-

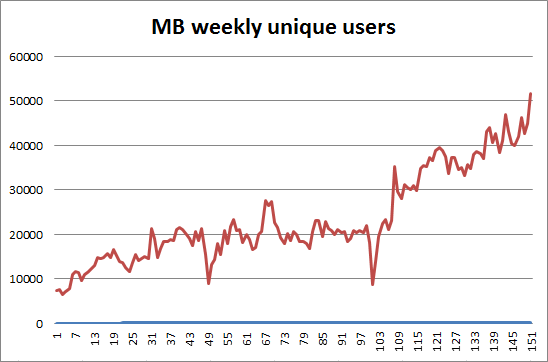

Here is the final readership update for the year. I’m pleased to report that the traffic breakout augured by the recent ascending triangle formation delivered in spades last week: