The great mystery of our time deepens daily. Fed mouthpiece, Jon Hilsenrath reckons:

Fed Chairman Ben Bernanke in June set out a three-part test—based on employment, growth and inflation—for reducing the $85 billion in monthly bond buys. He said the Fed’s policy committee wants to see progress in the job market, supported by improving economic activity and an inflation rate rising toward its 2% target.

“If the incoming data are broadly consistent with this forecast, the committee currently anticipates that it would be appropriate to moderate the monthly pace of purchases later this year,” Mr. Bernanke said at a news conference.

Recent data show progress on the first two criteria, but not on the third. The inflation rate has been persistently below the Fed’s objective and reflects weak consumption and wage growth, which bode poorly for the economic recovery. Fed officials will likely differ on whether the gains overall are good enough to clear Mr. Bernanke’s hurdles.

Maybe, but that sounds like a ‘no’ to me. What’s the point in having hurdles if your going to barge through them? Then again, the Fed is made of human beings, who agree on nothing.

On the data front, the pro-taper case got a boost from industrial production in November which finally got above its pre-GFC high:

Industrial production increased 1.1 percent in November after having edged up 0.1 percent in October; output was previously reported to have declined 0.1 percent in October. The gain in November was the largest since November 2012, when production rose 1.3 percent. Manufacturing output increased 0.6 percent in November for its fourth consecutive monthly gain. Production at mines advanced 1.7 percent to more than reverse a decline of 1.5 percent in October. The index for utilities was up 3.9 percent in November, as colder-than-average temperatures boosted demand for heating. At 101.3 percent of its 2007 average, total industrial production was 3.2 percent above its year-earlier level. In November, industrial production surpassed for the first time its pre-recession peak of December 2007 and was 21 percent above its trough of June 2009. Capacity utilization for the industrial sector increased 0.8 percentage point in November to 79.0 percent, a rate 1.2 percentage points below its long-run (1972-2012) average.

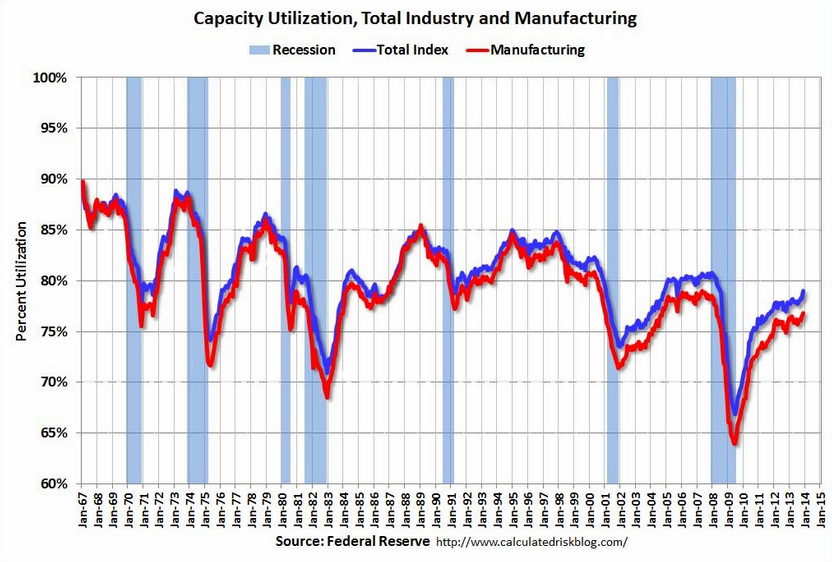

That data still looks shutdown muddied to me. Anyone wondering why there is no inflation need look no further than the chart by Calculated Risk:

Check out those historic steps down in capacity utilisation! Truly this is an oversupplied world.

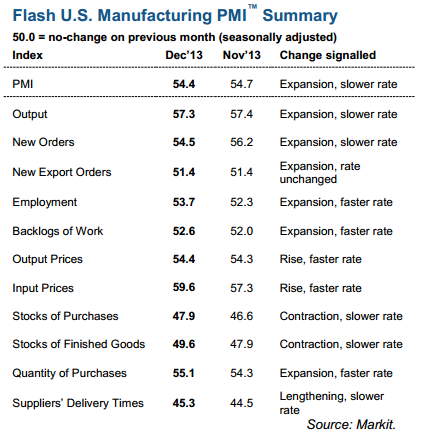

Also taper supportive, the Markit Flash PMI eased but held up with solid internals:

Less taper favourble data included the Empire State PMI which did nuthin’:

The December 2013 Empire State Manufacturing Survey indicates that manufacturing conditions were flat for New York manufacturers. The general business conditions index rose three points but, at 1.0, indicated that activity changed little over the month. The new orders index inched up, but remained negative at -3.5…Labor market conditions remained weak, with the index for number of employees holding at 0.0 for a second month in a row and the average workweek index dropping six points to -10.8. Indexes for the six-month outlook generally conveyed a fair degree of optimism about future conditions.

And housing is still slowing, at least in the bellwether state of California. From DataQuick:

Southern California’s housing market downshifted last month, with sales falling well below a year earlier as investor activity waned again and buyers continued to struggle with higher prices and a thin supply of homes for sale. The median sale price held nearly steady for the sixth consecutive month, though it was still almost 20 percent higher than a year ago, a real estate information service reported.

…The median price paid for all new and resale houses and condos sold in the six-county region last month was $385,000, up 0.3 percent from $383,750 in October and up 19.9 percent from $321,000 in November 2012. Last month’s $385,000 median price ties June, July and August as the highest for this year. The last time the median was higher than $385,000 was in February 2008, when it was $408,000 (the median was $385,000 in March and April of 2008).

“November sales were pretty underwhelming. The exact cause is tough to pinpoint, but we see likely culprits: The inventory of homes for sale still falls short of demand. Also, any pullback in home buying during the early-October fiasco in Washington D.C. would have undermined November closings, and we know investor and cash buying continued to drop,” said John Walsh, DataQuick president.

“Meanwhile, home prices aren’t soaring anymore but they’re also proving to be sticky,” Walsh said. “The price jumps we saw earlier this year were driven in large part by the supply-demand mismatch. This spring could bring a substantial surge in inventory as more homeowners look to cash in on higher values. If that happens it’s going to make big price jumps less likely.”

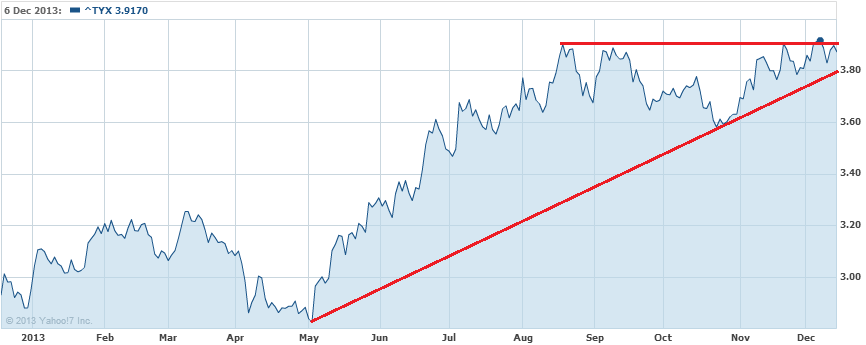

Sticky for now, but not if more interest rate rises emanate from the long bond and they will post-taper. The 30 year yield again spent the evening banging its head against the glass ceiling at 3.9%. The ascending triangle looks good odds to break upwards if taper comes:

Stocks rebounded firmly with the S&P up a little more than half a percent, the US dollar eased a touch, gold added half a percent and the Aussie went sideways. It’s a holding pattern, waiting on the Fed.