There’s a mini taper panic on. Last night’s us data was mixed but markets ran for the door anyway. November retail sales were strong:

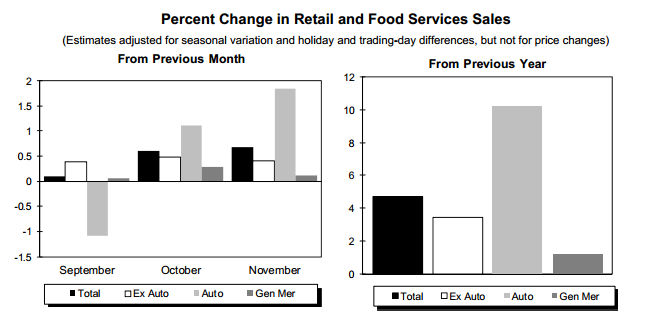

The U.S. Census Bureau announced today that advance estimates of U.S. retail and food services sales for November, adjusted for seasonal

variation and holiday and trading-day differences, but not for price changes, were $432.3 billion, an increase of 0.7 percent (±0.5%) from the

previous month, and 4.7 percent (±0.7%) above November 2012. Total sales for the September through November 2013 period were up 4.1

percent (±0.5%) from the same period a year ago. The September to October 2013 percent change was revised from +0.4 percent (±0.5%)* to

+0.6 percent (±0.3%).

Retail trade sales were up 0.6 percent (±0.5%) from October 2013, and 4.6 percent (±0.7%) above last year. Auto and other motor vehicle

dealers were up 10.9 percent (±2.1%) from November of 2012 and nonstore retailers were up 9.4 percent (±2.1%) from last year.

Good, but that looks like some shutdown snap back to me. Weekly unemployment claims were very weak:

In the week ending December 7, the advance figure for seasonally adjusted initial claims was 368,000, an increase of 68,000 from the previous week’s revised figure of 300,000. The 4-week moving average was 328,750, an increase of 6,000 from the previous week’s revised average of 322,750.

The advance seasonally adjusted insured unemployment rate was 2.1 percent for the week ending November 30, unchanged from the prior week’s unrevised rate. The advance number for seasonally adjusted insured unemployment during the week ending November 30 was 2,791,000, an increase of 40,000 from the preceding week’s revised level of 2,751,000. The 4-week moving average was 2,793,500, a decrease of 4,750 from the preceding week’s revised average of 2,798,250.

Advertisement

But there may also be shutdown distortions here and seasonal adjustment affected by hurricane Sandy last year.

In short, I wouldn’t trust last night’s data in trend terms. But Wall St, it seems, sees taper everywhere it looks now so stocks fell heavily before recovering and then selling again to be down half a percent of so. The US dollar firmed 0.3% and gold was pounded 2%. The 30 year yield climbed again into its recent 3.9% ceiling.

I still can’t see taper next week, if for no other reason than the data is still shutdown muddied, but who knows!

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.