Macquarie were out with a note yesterday and, not that it is new to MB readers, the news isn’t good for coal in 2014.

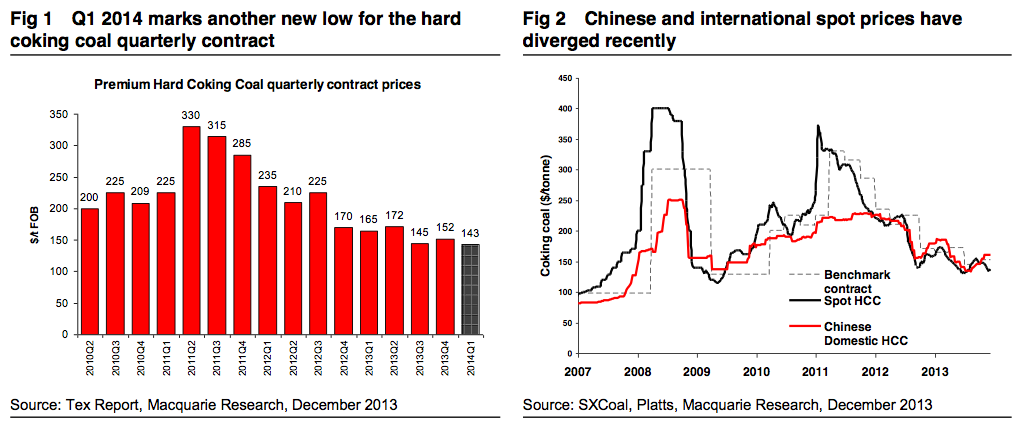

Unlike its peer steelmaking raw material iron ore, hard coking coal prices have had a disappointing 2013, trading significantly lower YoY. Meanwhile, with the Q1 2014 hard coking coal settlement at $143/t, the lowest in the history of quarterly contracts, the stage is set for another tough year in 2014. While there are indications the spot price may firm a little in the near term, the strong impact of supply growth this year will see a considerable hangover in 2014, with sustained price recovery looking longer-dated.

McCloskey and Platts have both reported that Anglo Coal has settled with Asian steel mills at $143/t FOB Australia for its premium hard coking coal German Creek brand, down from $152/t in the current quarter. This is, however, above the current prevailing spot price of $136/t, and at the level BHP priced January tonnes in the past week. We would suggest this is still below market expectations; however, given the supply headwinds at the current time, this is probably a fair result for both sides. It is, however, the lowest ever quarterly settlement since these began in 2010. There has been no confirmation of a PCI settlement as yet; however, this would also be expected to fall towards $114/t FOB Australia from $120.5/t in the current quarter.

And the reason? It’s all about supply.

The major reason for poor met coal price performance this year has been strong supply growth. This year remains on course to be the second highest absolute growth in history (after 2010), with 10.8% growth in seaborne exports. After 2011’s flood-induced drop, 2013 exports will be ~30mt higher than the previous record in a market where the 10-year average annual growth is just 9mt.

A major part of this growth has been Australian exports, which have more than regained the share lost during 2011. Exports from Australia this year will account for 58% of seaborne trade – not as high as in the middle of the last decade, but still reinforcing that met coal remains uniquely leveraged to Australian supply. Next year sees further growth in this area, with expansions continuing to come through at BMA operations; however, from 22mt of growth this year we expect only 6mt next – but growth nonetheless. Meanwhile, our longer-dated Australian supply growth has been pared back over the past year as what were Xstrata growth assets have been put on the Glencore back burner.

The biggest losers in the global market continue to be exporters from the US. Historically, the US has always been the swing supplier to global met markets and this should be the case again Benchmark (particularly as the market shifts further east), even with companies trying to brand themselves as contract structural global players. Finally, we are starting to see some signs of weakness in US exports, with recent shipments annuCahilnisesineg less than 50mt. We remain of the view that US exports have to be sustainably back below this level to help the rebalancing of this market – particularly so should freight rates remain at current levels. The global price will likely remain subdued until this happens.

On the demand side, met coal remains one of the least China-levered commodities in terms of seaborne trade. Here there are some green shoots, with European and Japanese buyers more active in recent times given potential steel output rises. However, this delta is nowhere near enough to offset the supply growth seen, and as a result the market has needed to ‘push’ excess material into China, hence the low spot prices. We see little change to this situation in 2014.

Certainly nothing new there. The big question for Australia is just how much the same dynamics starts to play out in the iron ore market next year as the uplift in supply takes hold.