Another bearish gold note today, this time from Macquarie Bank:

Recent commentary suggests the Fed’s position on tapering has seemed to harden. We still expect it in 1Q 2014, but that is now the latest it will be, in our view, and it could even be in December if forthcoming economic data is positive.

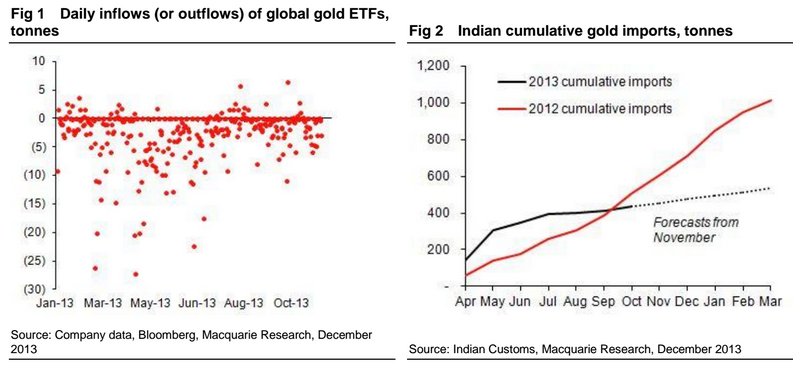

In 2014 gold will therefore have to deal with tapering being a reality, continued Indian weakness and even, we think, another year of higher mine output. China will continue to be a large consumer, although possibly not on this year’s levels if some demand was central bank related. We therefore think the gold price will continue to decline. The risks to the upside are if inflationary signs pick up, or if Indian policy changes, potentially after May’s election.

Outlook

With the gold price unlikely to provide significant respite for the gold producers in the coming 18 months we are focussed on those companies who are cash generative and with manageable balance sheets.

For those investors who are seeking exposure to the gold space, while limiting the risk to the downside we believe that with their low cost operations and free cash flow generation Beadell Resources and OceanaGold are the stand-outs in the sector. Within the explorer’s we believe that Papillon is a stand-out for the quality of its project, coupled with a proven management team.

With the high degree of volatility in the gold price driving large fluctuations in the revenue of gold companies we are of the view that gearing of >20% is a flag for concern across the sector. This risk is heightened where operating costs are >A$1,000/oz. (Although the higher cost operators have significantly more earnings upside to any positive moves in the gold price, we believe that the risk/reward is skewed to the downside for several of these companies.) As such we highlight Newcrest, Kingsgate and St Barbara as stocks which, on our production forecasts, will not generate significant cash to reduce gearing below 20% over the coming 18 months.

We continue to see the gold sector underperforming the broader market with gold stocks continuing to drift sideways to down until the Fed makes its announcement on tapering.

That said, for those investors with a longer time horizon or those willing to trade the volatility in between, we believe that the opportunity to derive significant returns from the space will present itself. Namely in the chance to buy quality names at cyclical lows.

That’s right, I think. There’s pain ahead for producers but its cyclical not secular. The end of this global cycle will see another round of destabilised monetary and fiscal policies as the many bubbles now growing go “pop”.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.