The IEA has released its 2014 Annual Energy Outlook and it sees a lot of US gas:

The Annual Energy Outlook 2014 Reference case released by the U.S. Energy Information Administration (EIA) presents updated projections for U.S. energy markets through 2040.

“EIA’s updated Reference case shows that advanced technologies for crude oil and natural gas production are continuing to increase domestic supply and reshape the U.S. energy economy as well as expand the potential for U.S. natural gas exports,” said EIA Administrator Adam Sieminski. “Growing domestic hydrocarbon production is also reducing our net dependence on imported oil and benefiting the U.S. economy as natural-gas-intensive industries boost their output,” said Mr. Sieminski.

Some key findings:

Domestic production of oil and natural gas continues to grow.Domestic crude oil production increases sharply in the AEO2014 Reference case, with annual growth averaging 0.8 million barrels per day (MMbbl/d) through 2016, when domestic production comes close to the historical high of 9.6 MMbbl/d achieved in 1970. While domestic crude oil production is projected to level off and then slowly decline after 2020 in the Reference case, natural gas production grows steadily, with a 56% increase between 2012 and 2040, when production reaches 37.6 trillion cubic feet (Tcf). The full AEO2014 report, to be released this spring, will also consider alternative resource and technology scenarios, some with significantly higher long-term oil production than the Reference case.

Low natural gas prices boost natural gas-intensive industries.Industrial shipments grow at a 3.0% annual rate over the first 10 years of the projection and then slow to a 1.6% annual growth over the balance of the projection. Bulk chemicals and metals-based durables account for much of the increased growth in industrial shipments. Industrial shipments of bulk chemicals, which benefit from an increased supply of natural gas liquids, grow by 3.4% per year from 2012 to 2025, although the competitive advantage in bulk chemicals diminishes in the long term. Industrial natural gas consumption is projected to grow by 22% between 2012 and 2025.

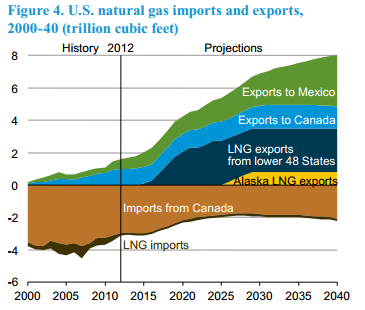

Higher natural gas production also supports increased exports of both pipeline and liquefied natural gas (LNG). In addition to increases in domestic consumption in the industrial and electric power sectors, U.S. exports of natural gas also increase in the AEO2014 Reference case. U.S. exports of LNG increase to 3.5 Tcf before 2030 and remain at that level through 2040. Pipeline exports of U.S. natural gas to Mexico grow by 6% per year, from 0.6 Tcf in 2012 to 3.1 Tcf in 2040, and pipeline exports to Canada grow by 1.2% per year, from 1.0 Tcf in 2012 to 1.4 Tcf in 2040. Over the same period, U.S. pipeline imports from Canada fall by 30%, from 3.0 Tcf in 2012 to 2.1 Tcf in 2040, as more U.S. demand is met by domestic production.

That’s 70 million tonnes in LNG exports plus another 50 million tonnes of gas to Canada and Mexico, plus another 20 million tonnes in displaced imports from Canada that’ll have to go somewhere. North America is awash with gas and it’s going to end up in North Asia from 2018 onwards.

BG Group is to begin commissioning its LNG processing “trains” on Curtis Island in Queensland after the project received its first coal-seam gas supplies from the Surat Basin.

It is the first of the three LNG gas export projects worth $70 billion scheduled to come into production, dramatically altering the shape of eastern state gas markets in the process.

…The first supply of gas to its Curtis Island plant was a “key milestone”, BG said.

“Delivery of first gas to the island marks the successful completion of a two-year task to lay more than 46,000 lengths of one-metre diameter steel pipe over 540km — the longest large-diameter buried pipeline in Australia,” BG said.

The arrival of first gas will enable commissioning work to begin on the first of two LNG production trains being developed by BG. The commissioning work is expected to begin in the first quarter of 2014.

Meanwhile, we need more gas plant operators or we’ll miss out on more investment, apparently:

Warnings of an emerging severe shortage of oil and gas plant operators in the next five years have sparked worries Australia could miss out on billions of dollars of investment because of a failure to invest in industry skills, training and productivity.

David Byers, head of the Australian Petroleum Production & Exploration Association, said Australia had to “aim much higher” on skills and training, especially particularly with the potential for another $180 billion in investment in the oil and gas industry over the next 20 years.

He said Australia needed to get serious about improving international competitiveness, increasing flexibility in the labour market and eliminating duplication in regulatory processes for major projects.

The report from the Australian Workforce and Productivity Agency, released on Monday, found resource construction jobs could slump as much as 90 per cent from a peak of more than 83,000 in 2014 to as few as 7700 by 2018 in the weakest economic scenario.

However, the demand for workers in the oil and gas industry is set to jump by 57 per cent to 61,212 in 2018, with 25 per cent of occupations set to be in short supply, including drillers, mining engineers and LNG plant operators.

Keith Spence, the spokesman for the agency, said the shortage exposed serious gaps that could compromise safety and reduce productivity.

Advertisement

With respect, if the industry can’t train it’s own people I’m not sure why the taxpayer should be doing it. And that’s the rub, really, this appeal is not about future possible investment. That’s already buggered. This is about rescuing the existing projects from the cost bubble they blew themselves. It will need to be done.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.