Advertisement

Citi has a great update today on Australia’s productivity growth as we head into our great adjustment. Sadly, productivity is slowing across the economy once more:

- Recent official data provide less encouragement on labour productivity trends. The consensus view has been that financial pressure on companies from the strong AUD has driven a renewed focus on productivity. However, the National Accounts showed that labour productivity was again slowing . In the first nine months of this year labour productivity rose at an annual rate of ½%-¾%.

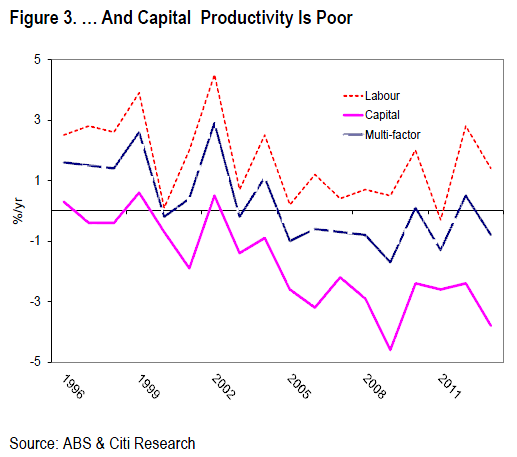

- Which isn’t good news for broader productivity trends. Annual estimates of multi factor productivity (MFP) had looked like they had turned the corner due to the pick-up in labour productivity, but on the most recent data that looks less secure. Meanwhile, capital productivity remains very poor.

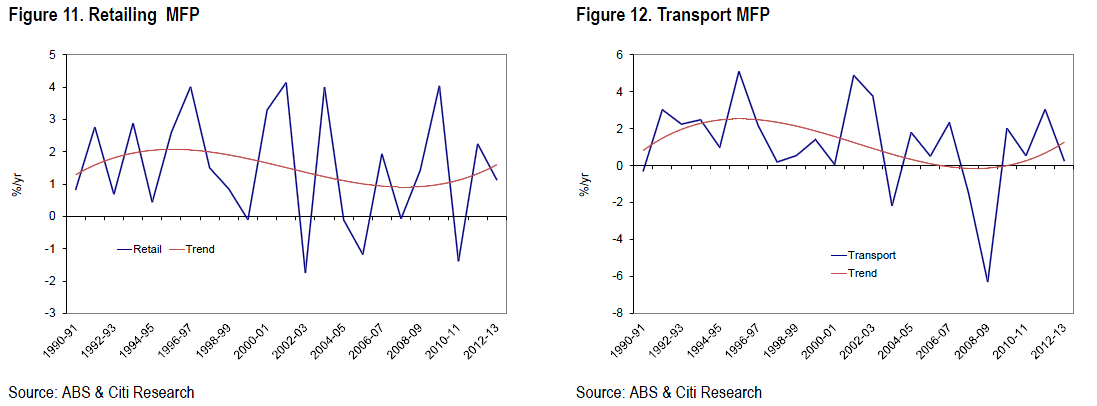

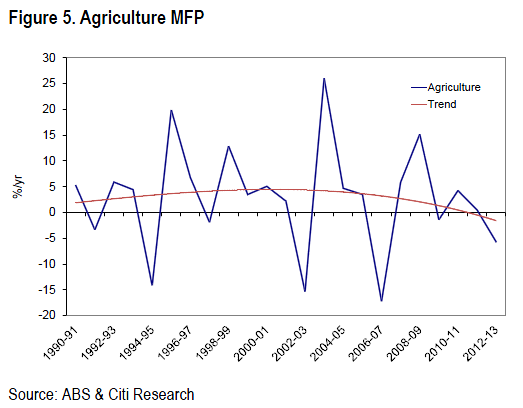

- Few sectors doing well. New ABS data show there are only a few sectors with both improving trends and moderate sustained positive productivity growth in the post GFC period, notably retailing and transport.

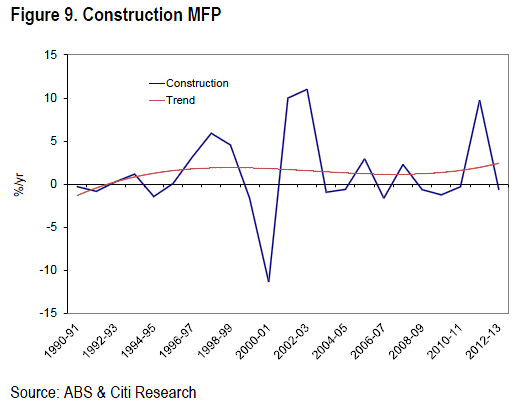

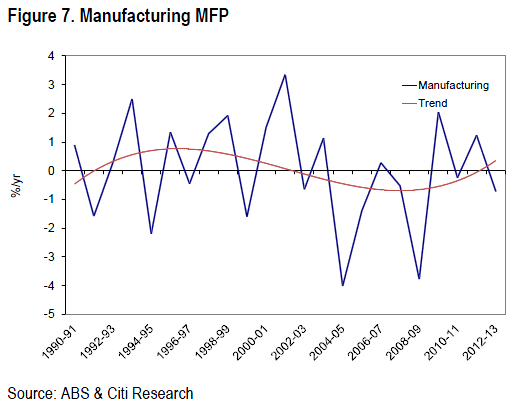

- Sectors which are mixed. Productivity in finance was hit by the GFC but finally rebounded strongly in FY13 and the long term trend remains strong. Construction and manufacturing had a very strong year in FY12, but not in other post GFC years.

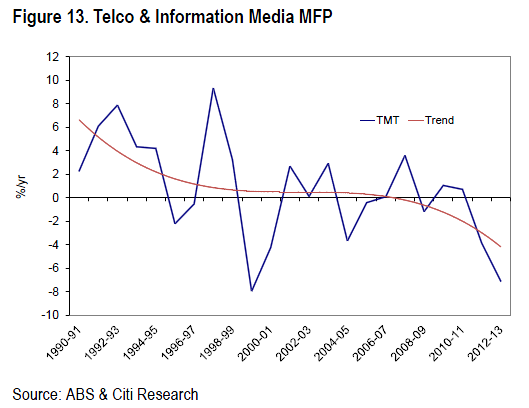

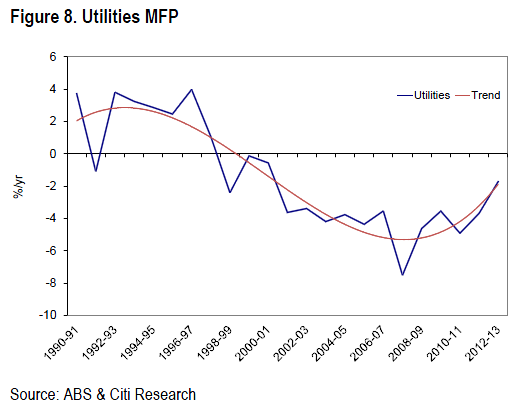

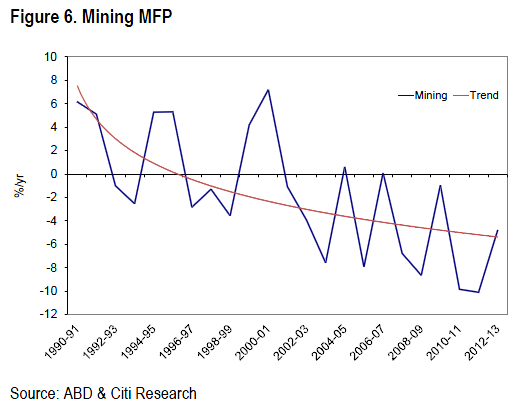

- Sectors doing poorly. Sectors with both a declining trend and negative productivity growth since the GFC include mining, TMT and entertainment. MFP in utilities is still declining but the trend is now improving.

- Reasons to be cheerful. One reason why capital productivity in a number of sectors has been so weak is that investment has been strong. The standouts are mining and utilities. But once investments are adjusted for varying rates of depreciation, there also has been strong investment in other weak capital productivity sectors such as TMT and entertainment. Provided the investment has been wise, productivity should improve. This seems a safe assumption for mining, but it is less clear elsewhere. The NBN? Casinos? Electricity networks? Water?

- Price signals and regulation also matter. Sound investment and hiring decisions depend in part on businesses and consumers having the right price signals. The flexibility to adjust operations and work practices quickly as circumstances change also partly depends on the quality of regulations. The Productivity Commission’s “to do” list highlights areas where pricing and regulatory reforms could lift productivity materially, but this will require a willingness of governments to use political capital.

- Global factors. The productivity surge in Australia during the second half of the 1990s paralleled the pick-up in the US attributed to the onset of a 3rd industrial revolution (computers). Debate in the US has centred on whether the current slowdown in productivity will give way to renewed fast productivity growth. Optimists point to recent advances in manufacturing and energy technologies, pessimists to declining quality of new inventions and education standards. The jury is still out. Australian productivity levels are below those in the US so there is scope for Australian productivity to catch up through reform, but if US productivity doesn’t return to the boom years it will harder for Australia to do so.

About the author

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

Advertisement