Not much data overnight from the US but plenty of good news. A Budget deal has been reached that reduces the sequester. From the NYT:

The agreement eliminates about $65 billion in across-the-board domestic and defense cuts while adding an additional $25 billion in deficit reduction by extending a 2 percent cut to Medicare through 2022 and 2023, two years beyond the cuts set by the Budget Control Act of 2011.

…Under the agreement, military and domestic spending for the current fiscal year that is under the annual discretion of Congress would rise to just over $1 trillion, from the $967 billion level it would hit if spending cuts known as sequestration were imposed next month. Spending would be capped at $1 trillion in fiscal year 2015 as well.

That’s an implicit acknowledgement of how badly the Tea Party stuffed itself in October.

Anyways, it’s another barrier to tapering removed. FTAlphaville has the nice list of the Fed’s options now:

1) Tapering

In his recent speech on communications, Ben Bernanke said there was “greater uncertainty about the costs and efficacy of LSAPs” relative to its forward guidance on short rates. He further added that “to the extent that the use of LSAPs engenders additional costs and risks, one might expect the tradeoff between the efficacy and costs of this tool to become less favorable as the Federal Reserve’s balance sheet expands.”

Bernanke’s intent was ostensibly to convince the markets that a slowdown in the pace of asset purchases would not be a signal of an impending rate hike, or even of a necessarily less-accomodative stance for overall monetary policy. The emphasis was on the tradeoff between marginal costs and marginal benefits for the continued use of this specific tool, Quantitative Easing.

The latest readings for GDP growth and the unemployment rate were better than the Fed’s projections earlier in the year. Yet both are problematic as indicators of renewed economic vigour. The new estimate for third-quarter GDP growth was bolstered mainly by inventory accumulation, while there continues to be debate about the factors behind the decline in labour force participation these past few years.

Furthermore, the core and headline versions of the Fed’s preferred inflation measure have continued to run beneath its projections and (to an appalling extent) beneath its 2 per cent target…

2) A change to the forward guidance thresholds:

This would most likely consist of lowering the unemployment rate threshold to adjust for the lack of clarity on the labour force participation rate (and suggesting that the decline in the unemployment rate has overstated labour market momentum). Along with the other ideas suggested here, it would be considered a dovish move to encourage a distinction between tapering and tightening. The idea received support in a much-discussed Fed staff paper last month…

3) Adding an inflation floor to the existing thresholds:

Bernanke referred to this policy during the September presser as a “sensible modification or addition to the guidance”. The idea is to add a lower inflation floor, perhaps 1.75 per cent or higher, to the extant thresholds. The Fed would be agreeing not to begin raising rates until inflation had climbed above 1.75 per cent even if the unemployment rate threshold is crossed…

4) A small reduction in IOER

Because of the Fed’s new reverse repo facility, a reduction in the 0.25 per cent interest paid on reserves is more of a legitimate possibility than it was in the past, when Fed officials considered and then dismissed the idea. The reverse repo facility can help keep short rates positive and further compress secured and unsecured rates. (Earlier coverage here and here.)…

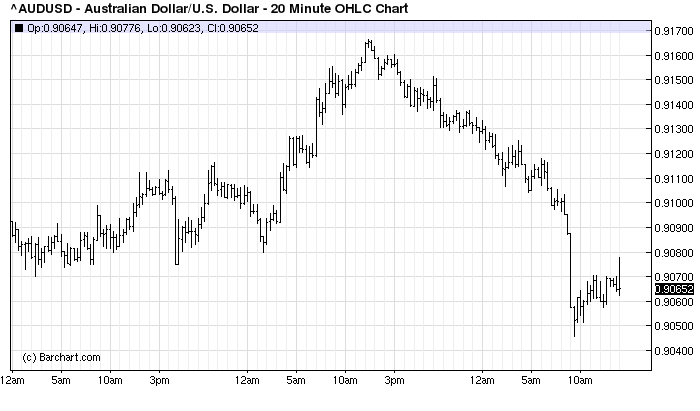

The early months of next year remain my favourite but I still expect it too hurt the economy pretty quickly as bonds sell and housing slows. Long bonds lost much of their recent gains last night with yields rising 1.5% to 3.88%. Stocks didn’t like it, down the better part of 1%. Complicating the picture, gold was down only a little and so was the US dollar but the Aussie was pulverised 1.6%:

There’s some GMHolden in there I’ll wager.