JPMorgan has a neat note that follows up yesterday’s Freeport LNG approval:

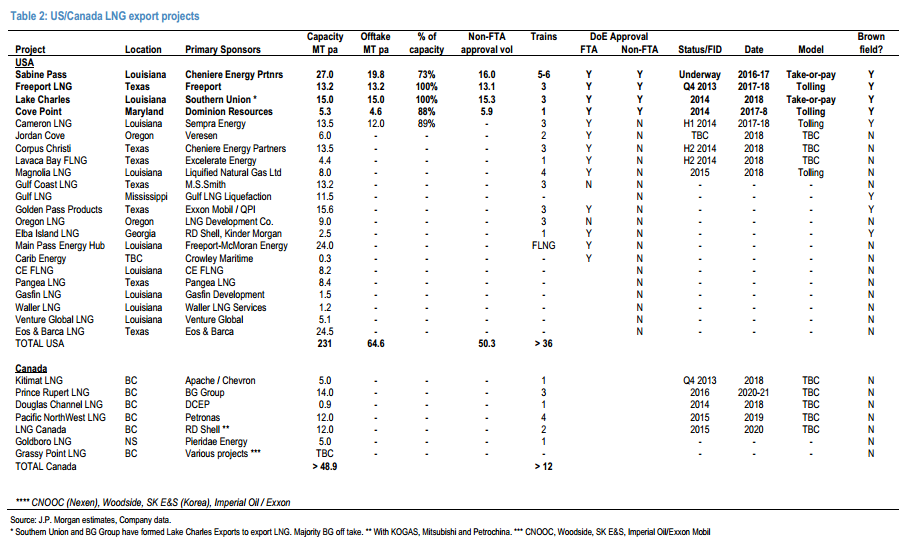

…greenfield US export proposals are likely to face greater scrutiny and more challenges than brownfield proposals. The four projects that have received non-FTA licenses are all existing regas operations which we believe provides significant brownfield economics when converting to a

liquefaction facility, specifically storage tanks, jetties, pipeline access and civil works. Of the remaining 18 proposed export projects, only four are existing regas facilities meaning the other 14 are greenfield projects which are likely to have materially higher capacity charges than the US$2.25- 3/mmbtu that we have seen from brownfield projects.

A fair assessment. Remember that the IEA sees 60mpta as enough to drive the north Asian price to $14. The top five meet that criteria and some. Cameron LNG is expected to get approval next for exports to non-FTA nations (that is, Japan).

There are two other ways of looking at this list. The remaining brown fields and FLNG projects looking for export approval constitute another 52 mpta, more than enough on the IEA’s reckoning to bring the north Asian price down to $12mmbtu.

Advertisement

Or, we could look at the projects that are in a more advanced stage of planning which constitute 33 mpta, again enough to drive down the north Asia price to $12mmbtu.

Any way you cut it, it’s an unpleasant list for those at the wrong end of the cost curve.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.