It’s been a while since I visited one of my key asset allocation themes of the past two years, that is Australian stocks exposed to a falling dollar. This has been due to the pause in the currency’s fall and the obvious rise of cyclical plays as the RBA fires up housing bubble enthusiasts.

But I retain my medium term view of the inevitibility of a much lower dollar – whether by choice earlier or hollowing out later – and my basic thesis for dollar-exposed stocks still applies.

Mac Bank has a useful note today on those Australian stocks with ready exposure to the US economy:

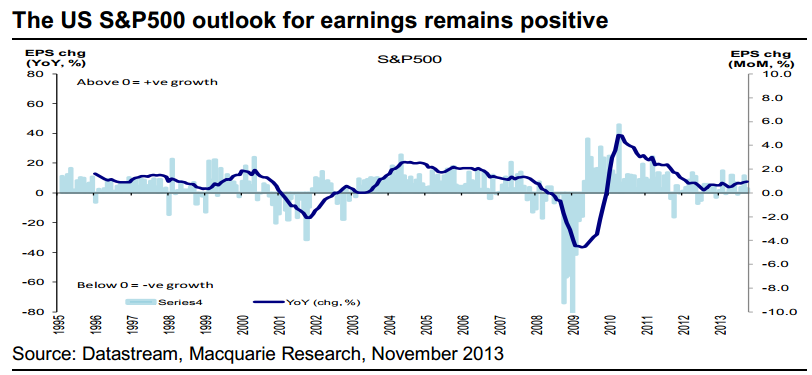

US 3Q13 EPS grew +6.6% year-on-year (+2.5% on 2Q13). CY2013 EPSg is currently annualising growth of +5.8% to date YoY. The S&P500 is expected to accelerate further in 4Q13 to +9.1% (driven by Consumer Discretionary, Financials, IT & Industrials sectors) to drive CY2013 consensus EPSg forecast at +6.5%.

Margins were the key driver of surprise again this reporting season. For the Industrials (ex Fins) EBITDA and profit margins are at near peak levels of 17.9% & 8.8%. Revenues for the overall sector grew at +3.4% YoY in line with expectations and a slight acceleration from 2Q13 (+0.8% QoQ). Revenue growth on a constant currency basis would have been higher still however USD strength had negative translation impacts on offshore reported revenues.

Our analysis of 3Q13 US reporting season suggests that the outlook for US corporate earnings remains positive. This bodes well for those US-exposed Australian-listed stocks. We think the premium valuations of the majority of these stocks to the market is commensurate with the higher EPS growth outlooks and the 3Q13 reporting season gives us comfort that US corporate earnings remain healthy with upside risks still present from here.

Our analysis of 3Q13 US reporting season suggests that the outlook for US corporate earnings remains positive. This bodes well for those US-exposed Australian-listed stocks. US stocks have been one of the strongest performing stocks within the S&P/ASX200 listed stocks over the last 6-12 months taking their lead from the S&P500.

Advertisement

And on companies themselves:

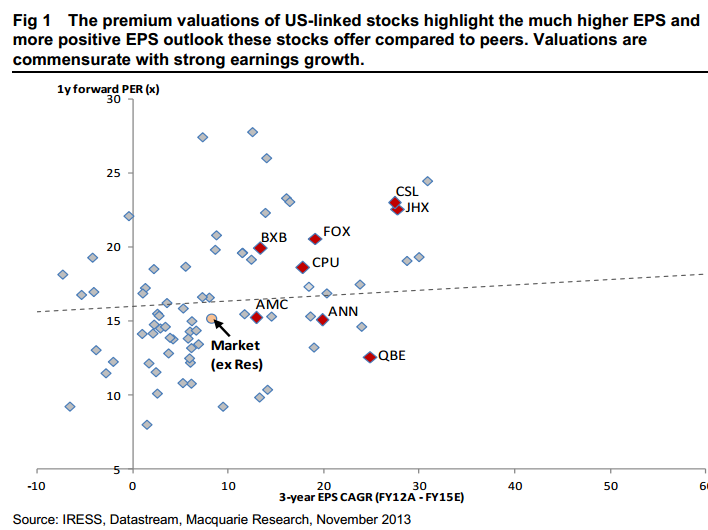

Valuations for the US linked Australian listed stocks still attractive given higher EPS outlooks (see Fig 1 below). Forward PER valuations for these International stocks have risen alongside rising Market PERs. The Market (ex Resources) is currently trading at a 1y forward PER of 15.2x.

The majority of the US linked Australian stocks are trading at a premium to this – CSL (23.0x), JHX (22.6x), FOX (20.6x), BXB (15.2x) CPU (16.5x) while AMC (15.3x), ANN (15.1x) and QBE (12.6x) are trading at market or discount valuations.

We think the premium valuations of the majority of these stocks to the market is commensurate of the higher EPS growth outlooks and the 3Q13 reporting season gives us comfort that US corporate earnings remain healthy with upside risks still present from here.

These stocks will also get the benefit of a lower AUDUSD when “QE3” tapering occurs. The Australian Equity Strategy portfolio has held a significant overweight to Global Industrials since October 2012 (see Equity Strategy – “Improving US outlook means more cyclical exposure”, 22 Oct 2012). We continue to hold this overweight given our positive view of the US economic cycle and earnings growth.

While corporate earnings continue to grow at a healthy rate (US 3Q13 EPSg +6.6% YoY), US economic indicators also point to a stable economy – US 3Q GDPg was stronger than expected (+2.8% vs. consensus +1.8% & Macquarie +1.5%) although reflective of a higher-than-expected build in inventories. Macquarie has maintained CY13 GDPg forecast of +1.7%.

Recent manufacturing and non-manufacturing ISM data point to an economy expanding faster than expected while the labour market also continued to improve (US payrolls increased +204k in October, beating the high of consensus estimates and disregarding the US Government shutdown during the month).

This stronger-than-expected data has raised questions again around the timing of “QE3 tapering”. Our Macquarie US economist is forecasting tapering to begin in March 2014, but regardless of the timing, QE3 tapering ultimately reflects stronger growth.

A guess “value” is all relative. They look damn expensive to me. But the investment rationale is fundamentally much stronger than playing local cyclicals.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.