More evidence of the rising central bank inspired global asset bubble today with the Twitter IPO launching for the moon and Bitcoin making its previous peaks look like adolescent pimples. On Twitter, the IPO went nuts. From Bloomie:

The shares rose as high as $50.09 and were trading at $45.49 at 12 p.m. in New York. The company sold 70 million shares at $26 in its initial public offering yesterday, raising $1.82 billion.

The microblogging service picked a price that valued it higher than rival Facebook Inc. (FB) and still drew more interest than anticipated. The San Francisco-based company, which is unprofitable and has one-fifth as many users as Facebook, is benefiting from investors’ thirst for companies that will grow quickly in expanding markets like mobile advertising.

“The company did everything to secure the most cash for itself while leaving some money for the IPO buyers,” said Josef Schuster, the founder of IPOX Schuster LLC, a Chicago-based manager of about $1.9 billion. “You need a pop at the opening to leave a good taste with everyone. They did a pretty good job managing the whole situation.”

At its opening price of $45.10, Twitter is valued at $24.6 billion, or 22 times estimated 2014 sales of $1.14 billion, according toanalyst projections compiled by Bloomberg. That compares with 11.6 times that Facebook was trading at yesterday andLinkedIn Corp. (LNKD)’s 12.2 times sales.

..The company received orders for about 30 times as many shares as it offered at the $26 IPO price, a person familiar with the matter said. About 8 million of the shares, or 11 percent of the total in the IPO, were allocated to retail investors, the person said, asking not to be named because the information is private. A typical retail allocation is 10 percent to 15 percent.

The Bloomberg IPO Index says it all. From Zero Hedge:

If the mooted listings for the rest of the year proceed, 2013 could be the best year for floats in Australia since 2007…

According to James Katzman, a managing director in Goldman Sachs’ US investment banking division, private equity is charging for the exits.

“Why do private equity funds, who have tonnes and tonnes of money to invest, sit on $16 billion of funds and not spend a lot of it?” Katzman asks.

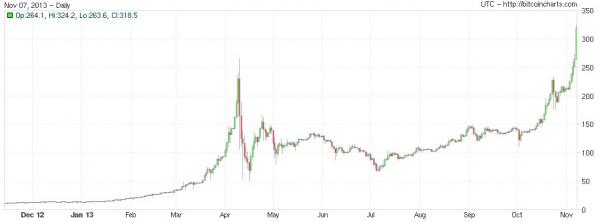

Meanwhile, if the digital currency Bitcoin is any guide to the value of fiat currencies worldwide then we’re on the road to Hell. As the ECB cut rates to record lows, Bitcoin also went nuts. Of Two Minds is discussing it as a new reserve currency:

Advertisement

The idea is intriguing on a number of levels. In terms of retaining value though thick and thin, the ultimate reserve currency cannot be printed (and thus devalued) with abandon by a government. Gold and silver have served as the ultimate reserve currency, as precious metals can be traded for commodities and services, provide collateral for debt and serve as reliable stores of value.

While many observers believe gold is still the only reliable reserve currency (or if you prefer, the only reliable backing for government-issued paper money), it’s a worthy thought experiment to ask if a digital currency could also act as a reserve currency.

Since there is no real-world commodity backing the digital currency, its value must be based on scarcity and its ubiquity as money. The two ideas are self-reinforcing: there must be demand for the digital money to create scarcity, and the source of demand is the digital currency’s acceptance as money that can be used to buy commodities, goods, services and (the ultimate test) gold.

It follows that the first step in a non-state issued digital currency becoming a reserve currency is that it isn’t created in quantities that dwarf demand. If the digital currency is issued with abandon, it cannot be scarce enough to gain any value. If I own one quatloo (our hypothetical digital currency) and a trillion new quatloos are issued tomorrow, the value of my one quatloo will decline to near-zero.

The second step is its widespread acceptance globally as money, i.e. a store of value and something which can be traded for goods and services.

There is a bit of a built-in conflict in these two requirements. To be useful in the $60 trillion global economy, the quatloo must be issued in size: there must be enough of it around to grease transactions large and small in all sorts of markets. Using the U.S. dollar as a guide (since the USD is the primary reserve currency), we can estimate that a minimum of $1 trillion in quatloos would be needed to become a practical global currency.

With respect, Bitcoin faces a far bigger constraint on its use than supply and demand. Fiat currencies are not ultimately in use because they are backed by commodities, though their value will to some extent reflect such underpinnings. They have power for one reason only and that’s the state’s monopoly on violence. Threaten state power and this baby will be gone before dinner. To describe the challenge facing Bitcoin as regulatory risk really does not cover it.

I see the rise of Bitcoin, rather, as a near perfect signal of the mad dash for anything, anywhere that has value above the zero cost of capital engineered by central banks all over.

Advertisement

If that’s true, then when do we sell this great and global souffle? Courtesy of FTAlphaville, BofAML asks that very question:

We note that nobody seems to ask about commodities and few seem to ask about China, the old leadership. And, nobody seems to talk about the “Tails” of inflation and deflation. We believe contrarians should at least consider hedges.

There is a performance chasing aspect to this. Also in our inbox is the Nacubo-Commonfund study of US endowments for the 2013 fiscal year (which tracks the academic, not the Roman calender).

Preliminary FY2013 returns broken out by asset class are:

· Domestic equities: 20.5 percent

· Fixed income: 2.4 percent

· International equities: 14.4 percent

· Alternative strategies: 8.6 percent

· Short-term securities/cash/other: 1.0 percent

Commodities and managed futures returned -6.0 per cent, the year’s only investment strategy to report a negative return.

Commodities matter because, well, they’re about real growth and sadly:

Advertisement

…Until a virtuous cycle emerges that starts with stronger housing activity and flows to stronger bank lending and stronger small business hiring, we believe growth in the US, Japan, and Europe will struggle to expand at a pace that does not require central bank liquidity injections and zero interest rates.

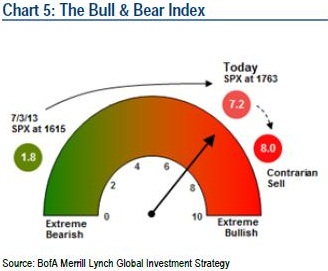

…Following a summer rally that has seen almost $7.5 trillion added to global market cap, our composite Bull & Bear Index, our favored cross-asset measure of investor sentiment, is now close to a cautionary sell signal. The Index is currently at 7.2, up from 1.8 in July. A breach of 8.0 has historically preceded a 5-8% correction for MSCI AC world over the next 1-2 months.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.