An interesting day in the US on Friday. Markets pulled back firmly from taper expectations with stocks advancing to record closes (Dow above 16,000, S&P above 1800), long bonds rallied firmly and yields pulled back from more than 1% to 2.85%, a little way below their recent breakout levels:

Data was thin so some of the pullback can be seen as technical but what there was was not taper friendly. Regional and state unemployment levels and job openings were unchanged in October:

Regional and state unemployment rates were little changed in October. Twenty-eight states had unemployment rate decreases from September, 11 states and the District of Columbia had increases, and 11 states had no change, the U.S. Bureau of Labor Statistics reported today. Thirty-eight states had unemployment rate decreases from a year earlier, 10 states and the District of Columbia had increases, and 2 states had no change. The national jobless rate was little changed from September at 7.3 percent and was 0.6 percentage point lower than in October 2012.

In October 2013, nonfarm payroll employment increased in 34 states, decreased in 15 states, and was unchanged in the District of Columbia and Pennsylvania. The largest over-the-month increases in employment occurred in Florida (+44,600), California (+39,800), and North Carolina (+22,200). The largest over-the-month decrease in employment occurred in Kentucky (-12,600), followed by Washington (-8,100), New Jersey (-5,500), and Virginia (-5,400). The largest over-the-month percentage increase in employment occurred in Wyoming (+1.0 percent), followed by Delaware, Florida, and Nevada (+0.6 percent each). The largest over-the-month percentage decline in employment occurred in Kentucky (-0.7 percent), followed by South Dakota (-0.6 percent) and Washington (-0.3 percent). Over the year, nonfarm employment increased in 49 states and decreased in Alaska (-0.9 percent) and the District of Columbia (-0.1 percent). The largest over-the-year percentage increase occurred in North Dakota (+3.5 percent), followed by Florida (+2.5 percent) and Idaho and Texas (+2.4 percent each).

The Kansas City Fed manufacturing index was decent:

The Federal Reserve Bank of Kansas City released the November Manufacturing Survey today. According to Chad Wilkerson, vice president and economist at the Federal Reserve Bank of Kansas City, the survey revealed that Tenth District manufacturing activity continued to grow, and producers’ expectations for future activity improved moderately.“Factory activity in our region continues to hum along at a moderate rate of growth” said Wilkerson. “The marked improvement in hiring plans was a nice development”.

…The month-over-month composite index was 7 in November, up from 6 in October and 2 in September … The new orders index jumped from 3 to 15.

But there was bad news for new housing, from the WSJ:

A monthly survey of builders across the U.S. by John Burns Real Estate Consulting, a housing research and advisory firm, has found that respondents’ sales of new homes declined by 8% in October from the September level and by 6% from a year earlier.

Last month’s result marked the second consecutive month in which the survey yielded a year-over-year decline in sales volumes, the first dips since early 2011.

In addition, the percentage of builders disclosing that they raised prices continued to decline, registering 28% in October in comparison to 32% in September and 64% in July. Of respondents, 12% lowered prices in October, in comparison to 12% in September and none in July.

“October was basically a crummy month for a lot of builders,” said Jody Kahn, a senior vice president at Irvine, Calif.-based Burns. “Their frustration is about the government shutdown and how it probably trumped any seasonal (sales) lift that builders were hoping to see. Most did not have very good sales.”

Shutdown, yes, but also interest rates, which are going to go 50bps high if there is a taper.

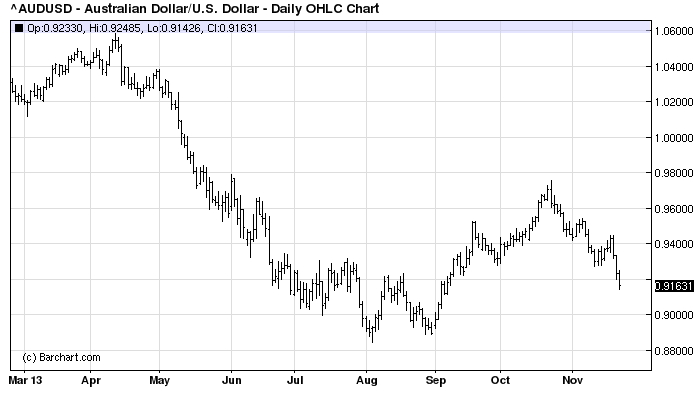

In line with a pull back in taper expectations, The US dollar lost half a cent on the night. The good news is that the Australian dollar fell anyway and sits on one ugly chart:

Marvelous what an activist central bank can do.