The Reserve Bank of New Zealand (RBNZ) yesterday released its biannual Financial Stability Report (FSR), which warns on housing risks and assesses the initial impact of its speed limits on high loan-to-value ratio (LVR) mortgage lending, which were implemented on 1 October 2013. According to the RBNZ:

“The main threat to the financial system is the risk associated with imbalances in the housing market. The previously announced loan-to-value ratio (LVR) measures, starting from 1 October, are intended to reduce systemic risk by slowing housing credit and house price inflation, and by reducing risk on bank balance sheets.

“The household sector has high and rising levels of debt relative to both historical and international norms. Both households and banks are highly exposed to the housing market. Further, we have a situation where house prices are rising from already-overvalued levels, particularly in Auckland and Christchurch. This is increasing the risk of a future house price correction that could result in significant financial system stress.

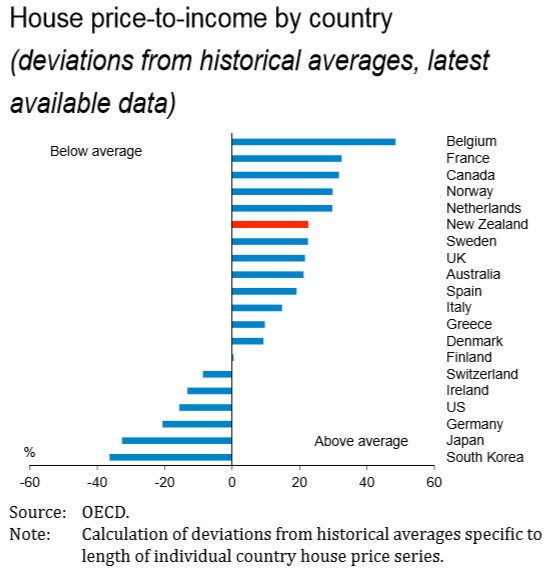

House prices are currently high by historical standards (relative to fundamental measures), and are overvalued by international comparison.

[RBNZ Governor, Grant Wheeler] said that several factors are contributing to the strength in house prices, including supply side constraints, a pick-up in net inward migration, relatively low interest rates, and relaxed credit conditions. “Dealing with the supply side issues is of primary importance. However, it is also important to avoid a prolonged build-up of excess demand while the supply issues are being addressed”…

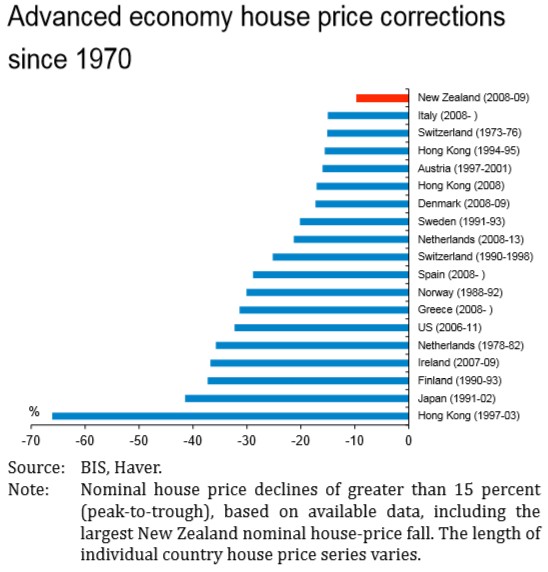

If unchecked, further near-term growth in house prices increases the likelihood of a disruptive adjustment in the housing market. Periods of large nominal house price declines have been experienced by a number of advanced countries over the past 40 years [see below]. More recently, the GFC has highlighted the severe financial and economic damage that can arise from a rapid correction in house prices, as witnessed in the US, Ireland and Spain, where prices fell by 30 to 40 percent. In the US, for example, a quarter of borrowers found themselves in a position of ‘negative equity’ – owing more than what their houses were worth.

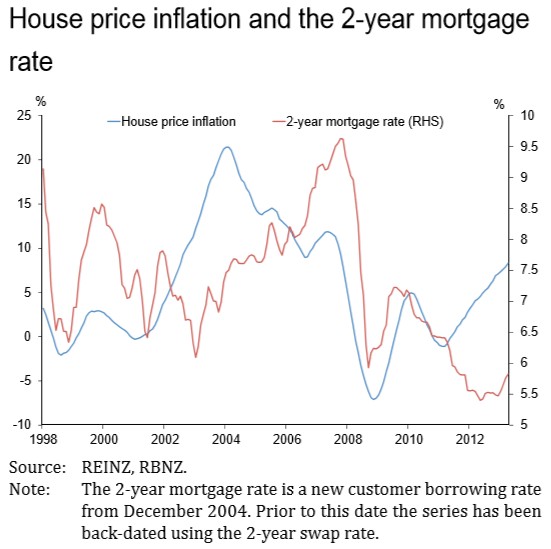

The increase in housing demand that has helped to fuel rapid house price inflation, has been enabled by an easing in bank lending standards and an increased share of low-deposit, or high-LVR, residential mortgage lending. High-LVR lending accentuates loan losses and worsens the subsequent economic disruption when overinflated house prices correct abruptly. High-LVR lending reduces the margin of collateral above the value of the outstanding loan and this margin may become negative if house prices fall, leading to loan losses for the lender if the borrower defaults.

High-LVR borrowers often have a higher debt servicing ratio – apportioning a higher share of their disposable income to meet their principal and interest payment obligations – so are more vulnerable to financial or economic developments such as a sharp rise in interest rates, or a change in their employment circumstances. High-LVR borrowers are therefore more likely to be forced to sell when house prices are falling, reinforcing the wider house price adjustment…

Mr Wheeler said that the Bank is closely watching the impact of the LVR policy. “The early evidence shows that banks have significantly reduced high LVR lending approvals, while increasing the cost of high LVR loans. However, it is too early to assess the impact of the measures on house price inflation”…

Advertisement

Separately in a Finance and Expenditure Select Committee (FEC), RBNZ Governor, Graeme Wheeler, noted that he is targeting a slow melt for house prices. From Interest.co:

“If we had inflation currently at around 1.2% at an annual rate and we have an objective under the Policy Targets Agreement of maintaining inflation over the medium term in the order of 2%, then you wouldn’t want to see house prices for the country as a whole growing at around 10% as they are at present. You would want to see a figure much closer over time to the level of Consumer Price Inflation,” Wheeler said.

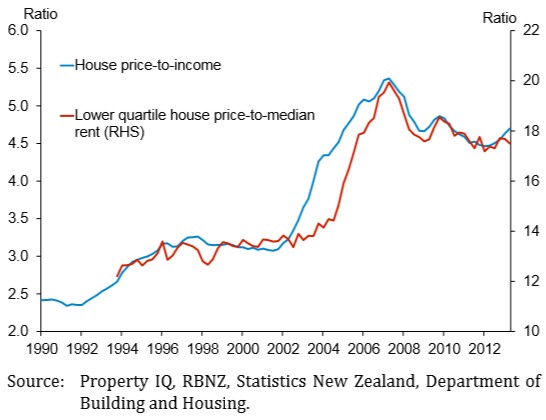

Wheeler agreed the bank would not want to see signficant falls in house prices. He pointed to OECD research showing New Zealand’s house price to disposable income ratio of around 4.5 was above its levels of 2.5 in the early 1990s and was 20% above its long term average.

“One doesn’t want to see a significant adjustment in house prices happening quickly, by that I mean house prices falling in nominal terms, which would pose risks to the financial sector. What one wants to do is to slow down the rate of house price appreciation and our measures are basically trying to affect the demand for housing while the supply side comes into much better balance,” he said.

He added the Reserve Bank would like to see the house price to disposable income lower over time.

And he added one of the reasons why:

Advertisement

Reserve Bank governor Graeme Wheeler says a potential downturn in the Chinese economy is the biggest risk to New Zealand and is the type of external shock the central bank wants to protect homeowners from with its restrictions on low equity house lending.

…”What could cause an adjustment here, what could do great damage to the economy and to the financial sector and to the housing sector? The biggest risk, my guess, would be around China,” Wheeler said. “China’s growth slowed from 10 percent on average, what it’s been for the last 30 years, and the issue is can it continue to grow at 7 percent or thereabouts.”

Comparing this with the RBA’s reliance on speeding housing up as China slows and its risks grow does not cast Australian authorities in a favourable light.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.