Cross-posted from David Collyer at Prosper

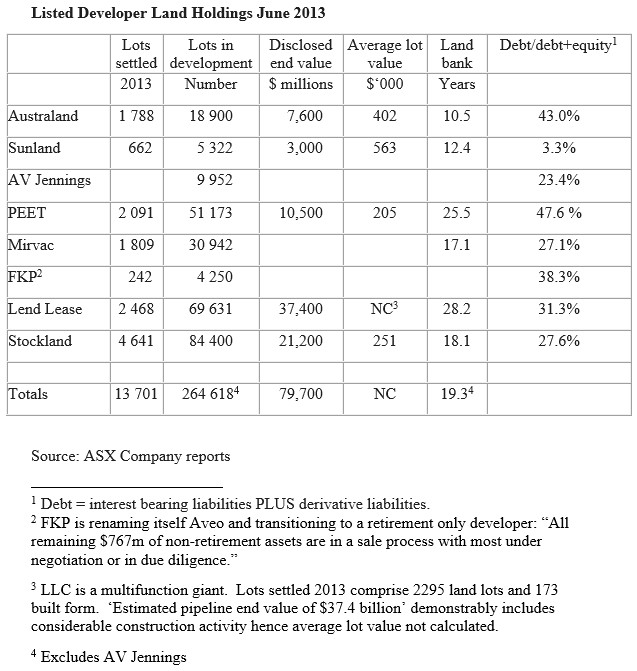

Sharemarket-listed property developers hold 264,000 residential lots in their development pipeline – 19.3 years supply with a disclosed end value of $80 billion – in a year when they sold only 13,000 lots, according to analysis by Prosper Australia.

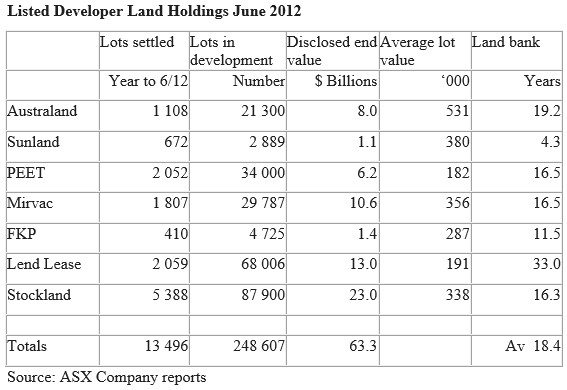

The largest holder is Stockland, followed by Lend Lease, with a giant 28.2 years supply of undeveloped land, firmly reduced from last year’s 33 years supply on higher sales. PEET has added substantially to its landbank, up from 34 000 lots to 51 000.

Listed developer land holdings by time extend well beyond government planning time frames, the classic definition of ‘landbanking’. They have land – hundreds of thousands of lots in development – but choose to ration it.

Listed developers are a minority of developers. Their lot sales last year were around a tenth of building approvals, but their behavior is publicly visible – and instructive.

It can be argued this is far-sighted corporate behavior, like a winery holding vintage wine while it matures. In practice, landbanking developers hold new home buyers to ransom by limiting supply and driving up prices. High prices for parcels on the periphery boost the price of all better located land with shorter transits and already-built facilities.

Land in Australia should be dirt cheap. Outstanding access to land ought be a national advantage, generously conferred by a loving government upon the citizens it represents.

Developer selfishness can be changed by astute application of State Land Tax. Broadacre land in Precinct Structure Zones ought be taxed as if it were already in use. Developers would turn their holdings as quickly as possible, rather than hoarding it.

Withholding vacant land from use displaces activity and drives up land prices – to the great advantage of all existing landowners. While developers can rightly argue they are constrained by government planning controls, their behavior speaks loudly.

They respond to falls in sales volumes and prices by further reducing the size of lots to maintain margins and turnover.

Previous land price downturns have been characterized by developer bankruptcies as banks made margin calls on this traditionally highly-geared industry. The listed group now carry very little or no debt against their landbanks. All have a level of debt, mostly secured against commercial and industrial projects or ready-for-sale lots.