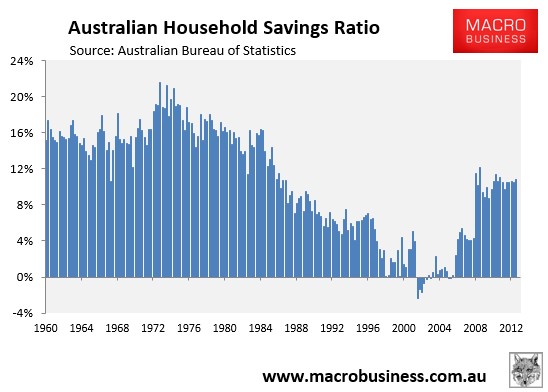

Australia’s high household savings rate, which is currently running at over 10% (see next chart), is viewed as a key plank in the RBA’s plans to “rebalance” the economy away from mining-led growth. The Rationale behind the RBA’s plan is that if it cuts interest rates hard enough, then households will save less and consume more, in turn boosting interest rate sensitive sectors of the economy such as retail sales and housing, which would then grow at a faster rate than disposable incomes.

New research from Credit Suisse’s Damien Boey, however, questions whether Australia’s savings rate is really all that high and whether Australian households are in the position to drive the economy’s rebalancing.

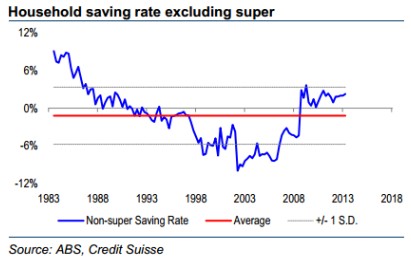

According to Boey, Australia’s official household savings rate is “somewhat illusory”, biased upwards by “compulsory saving (superannuation) and does not properly take into account principal payments on mortgages”. When adjusted by these factors, he believes that Australian “households are really not saving much at all”, making them poorly placed to offset the expected unwinding of the mining investment boom.

The issue around compulsory super is that it is locked away until retirement age, therefore, the ability to withdraw from these ‘savings’ to fund consumption is limited. And “removing superannuation from the official saving rate lowers the discretionary saving rate to 2 per cent from 10 per cent”, according to Credit Suisse.

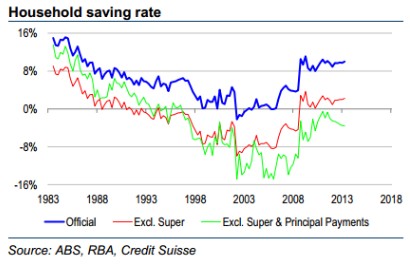

A more serious issue surrounding the ABS’ official household savings rate is that it “does not properly take into account mortgage principal payments, which currently make up a large proportion of the cash cost of housing”:

We can measure net mortgage principal payments as the difference between gross loan approvals and credit growth. Adjusting for both superannuation and principal payments, we find that the discretionary saving rate falls to minus 3.6 per cent from 2 per cent. This measure of the discretionary saving rate is not only low in absolute terms, is also low by historical standards.

Credit Suisse does, however, acknowledge some potential pitfalls in its analysis:

Perhaps [our] measure of discretionary saving understates how much households actually do save, because our measure of net principal payments includes those that are ahead of schedule – not minimum payments.

Indeed, these discretionary principal payments could be viewed as a form of saving. However, we note that if households were not making such large principal payments, debt would be accumulating at an even faster pace, and the interest burden would be considerably higher in future periods.

Nevertheless, it does still conclude that the household discretionary savings rate – i.e. the amount of savings that are actually available to fund consumption – is “…not as high as the official measure suggests [and] is actually slightly below long-run average levels. Therefore, we do not believe Australian households have a large pool of saving to draw down on and consume.”

The only way that Credit Suisse can foresee a significant rise in household spending were if Australia experienced “a significant increase in asset prices or a material easing of bank lending standards to cause households to reduce savings”.

However, it is not convinced that such a scenario is likely since “banks might tighten their lending standards in the short term due to regulatory concerns about excessive gearing. So overall, the threshold for dis-saving is quite high”.

Overall, Credit Suisse does not believe that household consumption will be anywhere near enough to offset the contraction in mining investment, which would mean that Australian GDP growth would be slower than forecast, and official interest rates will remain low for an extended period.

As explained by Houses & Holes yesterday, we tend to agree.

unconventionaleconomist@hotmail.com