Cross-posted from Wolf Richter at Naked Capitalism.

The Senate hearing on Monday was the culmination of a three-month investigation into virtual currencies, said committee chairman Sen. Tom Carper (D., Del.). “Virtual currencies, perhaps most notably bitcoin, have captured the imagination of some, struck fear among others, and confused the heck out of the rest of us, including me.” He was worried that they could facilitate the sale of “weapons, child pornography, and even murder-for-hire services.”

So you’d expect some saber-rattling by the government officials who’d been asked to testify. But instead, it practically turned into a love fest.

Officials from the Secret Service, the Treasury’s Financial Crimes Enforcement Network, and the Justice Department bragged to the committee about successful investigations of crimes where bitcoin or other virtual currencies were used, including the busts of Silk Road, eGold, and Liberty Reserve. They were confident that they knew how to tamp down on criminal use of virtual currencies. No one expressed outright alarm about the new world of bitcoin.

Since every transaction of every bitcoin is forever recorded and part of the system, Mythili Raman, acting assistant attorney general at the Justice Department’s criminal division, pointed out that “cash is still probably the best medium for laundering money.” And she admitted that “many virtual currency systems offer legitimate financial services and have the potential to promote more efficient global commerce.”

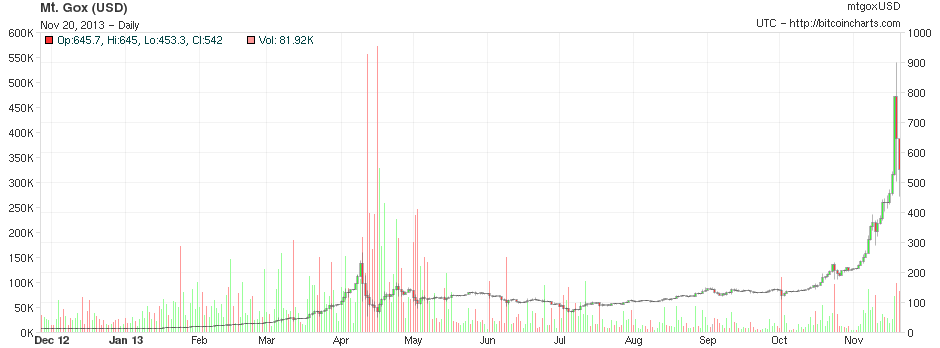

At the word legitimate, bitcoin soared. And I mean, SOARED.

Even if they don’t agree on what bitcoin is, regulators clearly don’t want to go through the hassles of banning it or policing it. So if it’s a “security” where in the end a lot of people will lose a lot of money, so be it. That happens every day with securities.

Yet they are fretting about transactions. It seems they would like to prevent bitcoin from competing as a currency with the dollar. But they don’t want to get their hands dirty. And they found out how to do that. It’s so simple, it’s beautiful: Encourage bitcoin to become so phenomenally volatile with such mindboggling jumps and brutal crashes that no one can afford to use it as a currency to buy or sell anything, licit or illicit.

Taking on the dizzying risks of getting crushed by price swings can be fun for speculators, but they would be debilitating for buyers or sellers. So you want to buy a house valued at $500,000 and pay in bitcoins. You sign the contract on September 19, when bitcoins change hands at $134 each. So the contract specifies that you have to pay 3,731 BTC at closing. Closing was last night, after bitcoin had soared to $900. The transaction price of the house, in dollar terms, would then be $3.36 million. You’d get crushed by a $2.86 million loss on a $500,000 house. You’d never, ever do that again.

Another day, the price could swing the other way, and then it would be the seller’s turn to get crushed. That’s the idea. If regulators can keep it that way, while allowing speculators to play with it and have fun with it and drive the price up and down maniacally, bitcoin will die as a currency that can be used to buy or sell anything.

Turns out, all this drama can actually happen in time-lapse. Not in weeks, but in hours. Yesterday around midnight, after an already crazy run-up, bitcoin traded for $575. Then, triggered by the word “legitimate” or some other word, or something in the water, it spiked to $900 for the briefest moment at around 5 p.m., only to crash to $502 by around 4:45 a.m. today. It since jumped to $745, and now, as I’m writing this, re-crashed to $640 $599 $489. You can’t do business with a “currency” like that. You can only have fun with it or lose your shirt. And the Fed, the SEC, and a myriad of other regulators can pat each other, or themselves, on the back.