The Housing Industry Association (HIA) has today released a new report claiming that prospects have brightened for a broad-based recovery in dwelling construction (with the exception of Victoria), although supply-side barriers remain:

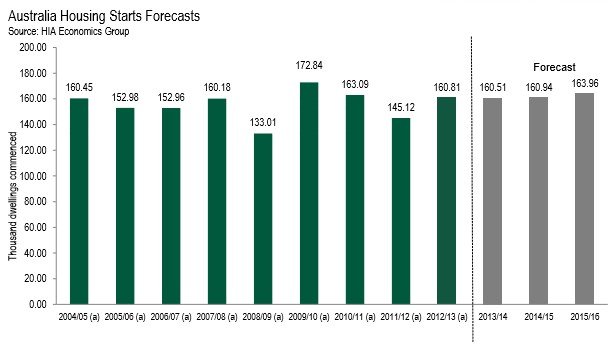

New dwelling commencements (housing starts) increased by 11 per cent in 2012/13. This result followed two consecutive years of decline which saw commencements bottom out at their third lowest level of the last 15 years. The same time that commencements posted this first round recovery, renovations activity hit a ten year low, so the recent news hasn’t been all one way.

Admittedly the ‘first round’ new home recovery last financial year was narrowly driven. Dwelling commencements in New South Wales and Western Australia increased by 31 per cent in 2012/13 to deliver the lion’s share of the 11 per cent growth in commencements we saw nationally. With the netting out of NSW and WA, commencements increased by only 1 per cent last year.

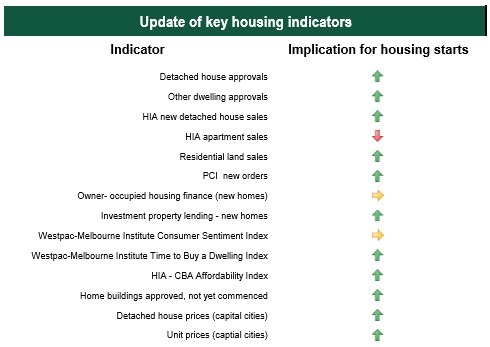

The recovery had to start somewhere though and it did. Furthermore, eleven out of fourteen indicators we have identified (not in itself meant to be an exhaustive list) imply a further short term increase in housing starts…

Building approvals figures for the September 2013 quarter signal further upward momentum in dwelling commencements for both WA and NSW. In that quarter building approvals in WA increased by 7.7 per cent (driven by both detached house and ‘other’ dwellings, especially the former). For NSW the increase was 25.2 per cent (driven by both detached house and ‘other’ dwellings, especially the latter).

The key now is to observe further growth in commencements in these two markets against the backdrop of excessive and inefficient taxation and regulation, while seeing other geographical areas hitching a ride on the growth train.

That prospect appears increasingly likely.

There are, however, a large number of variables currently in play when considering the future of new home building (and renovations) activity. These include: the historically narrow base to the first stage of a new home building recovery – noted above; the significant increase in the taxation and regulatory burden on new home building over the last 15 years; the tightest credit conditions the industry has experienced since the 1970’s; the largest household deleveraging process Australian households have undertaken in many, many decades; the unknown quantum of productive capacity lost to the industry over the last ten years; and the difficulty in determining what the natural, non-stimulus assisted upper threshold to new home building levels is in the post-2000 environment where GST is levied on new housing but not on existing property.

These variables do, in their own right, bias sentiment and forecasts for new residential construction activity towards the negative.

However, there is clear momentum building in a range of leading indicators for new housing which provides a basis for a reasonably positive outlook…

We consider it most likely that the two fast growth states to date – NSW and WA – maintain levels of dwelling commencements comparable to those in the latter half of 2012/13 rather than continue along the strong upward trajectory we saw throughout 2012. This outcome would nevertheless still provide another strong annual increase of 11.1 per cent and 8.5 per cent for NSW and WA, respectively, in 2013/14…

A large decline in Victoria is set to weigh heavily on the national total in 2013/14. Relatively strong recoveries in activity in Queensland and SA (of 7.7 per cent and 10.5 per cent, respectively) combined with the increases in NSW and WA mentioned above, are likely to be insufficient to offset the decline. The net result of this contrasting activity around the key states appears set to provide around 160,500 commencements in 2013/14.

Beyond 2013/14, activity levels in NSW, Victoria and WA are forecast to remain at levels comparable with those we expect this financial year. However, the recoveries in Queensland and SA are forecast to gather momentum and drive a modest increase in dwelling commencements nationally in 2014/15. Further growth of 1.9 per cent is forecast for 2015/16 which would take starts back to a level around 164,000.

As noted last week, the forecast pick-up in dwelling construction is actually fairly lackluster. Despite record low interest rates, established house prices rising, widespread stimulus aimed at first time buyers of newly constructed dwellings, and near record population growth, housing starts are forecast to rise only modestly to 164,000 homes by 2015-16. There is mounting evidence in the data that the rebound as already peaked.

Advertisement

Clearly, unless reforms are made to: free-up land supply and competition amongst land holders and developers; reduce taxes and regulatory changes on development; streamline development approval processes; and improve the provision of housing-related infrastructure, then the cost of new homes are likely to remain above what many people can afford or are willing to pay, and the construction pick-up will remain muted.

Continuing to pump demand via cheap credit and home buyers grants will provide a modest short-term sugar hit to construction (as it did in 2009-10), but it does nothing to fix the underlying structural barriers that prevent affordable and desirable houses from being supplied to the market.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.