APRA has released its monthly banking statistics for October and deposit growth has stabilised.

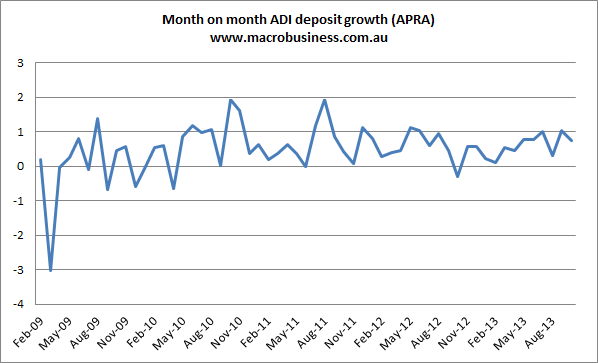

Monthly growth eased:

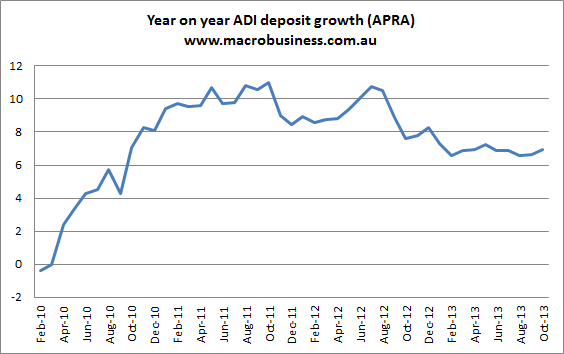

But year on year growth is stable above 6%:

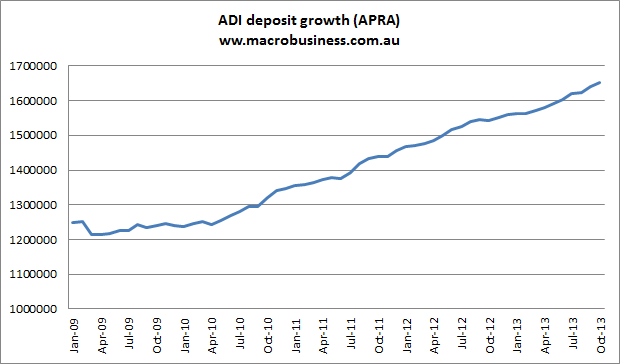

The aggregate trend is solid:

Advertisement

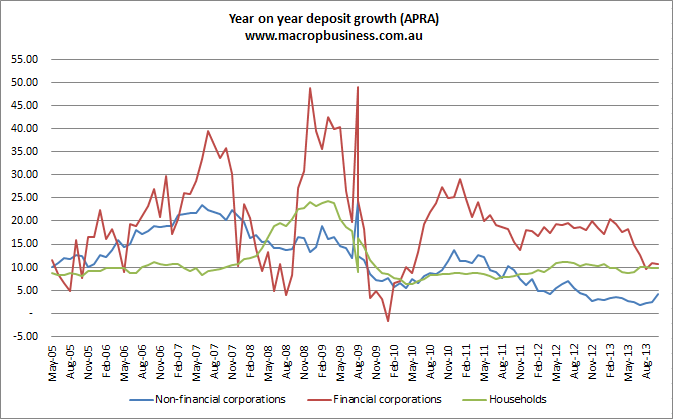

And households are sustaining their savings habits nicely:

Amid falling income growth across the nation this says to me that households remain prudent.