You’ve got to hand it to the folks at BREE. They are the world’s greatest optimists. Today’s six monthly update to the major projects pipeline is awful but you won’t catch them saying so:

BREE’s conceptualisation of the investment pipeline is a generic model and in practice resources and energy projects go through tailored development processes that suit their proprietor’s planning requirements. The pipeline model is useful for assessing trends in resources and energy sector investment such as the rate at which projects are progressing or if bottlenecks are emerging at any particular point. Despite the strength of the resources boom over the past decade, it has been clear that not every resources and energy project is developed. As such, the projects still in the Publicly Announced and Feasibility Stages can only be viewed as potential investment and additional analysis is required to produce an outlook for future investment in the resources and energy sectors.

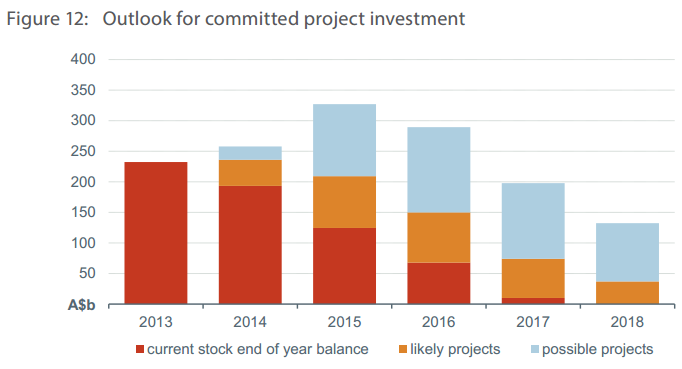

BREE’s outlook for resources and energy project investment provides aggregate estimates of investment in two scenarios, a ‘likely’ and a ‘possible’ scenario. The two scenarios model the rate at which projects currently at the Committed Stage are expected to move to the Completed Stage and are subsequently removed from the list, as well as the timing of projects assessed as possible or likely to progress to the Committed Stage. The schedules of planned projects, including both the timing of a FID and start of production, are uncertain and subject to variation.

The ‘likely’ scenario is based on the existing projects at the Committed stage and adds projects that BREE assesses as having a higher probability of proceeding based on analysis of a range of internal and external factors that historically helped determine a project’s success in being sanctioned. Where data is available, analysis of the proposed project’s position on the relevant commodity cost curve and an assessment of the internal rate of return are undertaken. As the assessments are probability-based there still remains a degree of uncertainty over projects assessed as likely and their progression to the Committed Stage is far from guaranteed. The ‘possible’ scenario includes projects already at the Committed Stage, projects assessed as likely to proceed and projects assessed as ‘possible’. A possible rating is given to a project that has some positive internal and market factors that suggest it may advance to the Committed Stage, but it also faces greater challenges than a ‘likely’ project that may limit its commercial viability.

Projects assessed as unlikely to proceed are not included in the forward projection of the value of committed investment. Although assessments are made at the project level, as some of the information provided to support the assessment is treated as commercial in confidence, individual project assessments are not provided.26 Resources and Energy Major Projects • October 2013

Outlook for resources and energy investment

The stock of committed investment in the Australian resources and energy sectors declined from $268 billion to $240 billion in the six months from April 2013 to October 2013. This large drop in investment is the result of two records being set in the period – a record high for the value of projects being completed ($30 billion) and the lowest value of new projects being sanctioned in the past decade ($1.7 billion). Both measures are initial indicators that the Australian resources boom is now transitioning from the investment phase to the production phase.

There remains the potential for further investment in Australia’s resources and energy sectors. However, the latest commodity price cycle has reached its apex and the decline in the prices of most commodities over the past 12–18 months has created more challenging investment conditions. Many (but not all) commodity markets are either already or soon to be oversupplied as the lower demand growth trajectory has undershot the rush of global investment to increase supply over the past five years. Although commodity prices are cyclical, it is unlikely they will rebound to the very high levels observed at the peak of the latest cycle. As such, the prospects for investment at levels comparable to the past five years in Australia are limited.

As outlined in the previous Resources and Energy Major Projects a substantial number of the high value projects that would have sustained the record levels of investment in the resources and energy sectors have been either delayed or cancelled. This trend has continued over the past six months and BREE has removed 37 projects from the major projects list. A further 71 projects have been delayed across all stages of the investment pipeline. BREE’s projection for the decline in the existing stock of committed investment remains broadly unchanged. The only notable variation to the projected value of the existing projects relates to the delay to completion of the Sino Iron Project ($8.4 billion) which has resulted in a higher than previously expected end of year value for existing committed investment in 2013. The value of the existing stock of committed projects is still projected to decline rapidly over the next four years in line with the completion schedules of the mega LNG projects.

By comparison, the projected value of investment in both the likely and possible scenarios reflects the revisions to project schedules. Since April 2013 there has been a marked move to the right in projected aggregate investment in both scenarios as a result of delays to several high value projects. In the likely scenario, committed investment in 2014 is forecast to increase (potentially) above the 2013 end of year level but still remain well below the peak levels of 2012.3

The approval of all projects assessed as possible in 2014 would also not support a return to such investment levels (see Figure 12).

In 2015 there is the potential for a rebound in resources and energy sector investment as there are a large number of projects that are assessed as requiring a FID in that year in order to meet their current schedule. This rebound would require a substantial portion of projects assessed as possible to be approved as committed investment in the likely scenario is projected to decline in 2015 due to the effect of LNG trains being completed in that year. After 2015, both the likely and possible investment scenarios are projected to decline with further LNG train completions being a primary driver of the decline. Later in the outlook period the committed investment projections become more heavily reliant on projects currently rated as possible.

This is mainly because detailed information on projects scheduled for FID after 2015 is still unavailable and limits the prospect of providing higher probabilities of success for those projects.

These investment projections are based on projects achieving their current schedules and as previously noted, there has been a high incidence of realised schedule risks in resources and energy projects over the past 12–18 months. Nevertheless, there remains significant opportunity for additional investment in Australia’s resources and energy sectors. While market conditions are expected to remain challenging, in the right commercial and policy environment there is the potential for committed investment to remain at high levels for several more years.

In assessing the current downturn in the resources and energy investment cycle it is important to remember that while this signals a potential end to the investment phase of the mining boom, the transition to the production phase is only just beginning. During the 12 months to October 2013 the value of completed projects was a record high $45.7 billion. In the past 12 months there have been production capacity increases of 108 Mt per year of iron ore, 13 Mt per year of coal, 182 PJ per year of gas and 1.2 million ounces per year of gold. With further production capacity of 126 Mt of iron ore, 60 Mt of coal and 61 Mt of LNG still under construction, there is still substantial growth to come in Australia’s output of mineral and energy commodities to come. To put the scale of the transition to the production phase in perspective, the increase in iron ore production capacity achieved by Fortescue Metals Group completing its expansion projects over the past 12 months is, by itself, larger than the annual iron ore exports of any country other than Australia and Brazil in 2012. Like many mining projects undertaken in the past five years, the output from Fortescue’s expansions is scheduled to continue for many years.

While the capital inflows associated with investment phase of the mining boom have brought substantial economic benefits to Australia they are realised over a relatively short period of time. The economic benefits of the production phase may not be as large as the investment phase per year, but they are expected to last for considerably longer.

So, despite the past six months seeing both the largest ever rise in the value of projects being completed and smallest ever increased in newly “sanctioned” projects and an acknowledgement that we’re moving into oversupply for many commodities, we’re going to see a “likely” outcome next year of $50 billion in new projects going ahead and almost $100 billion in 2015. That does not pass the laugh test.

Advertisement

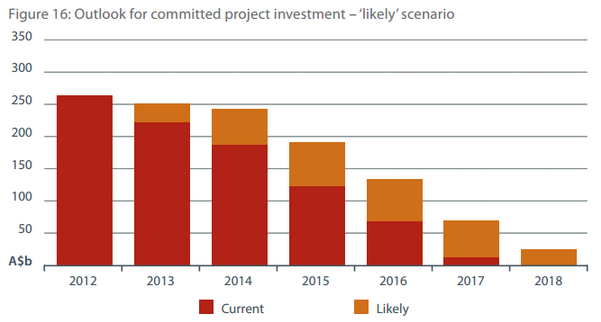

What is going to happen is that some modest fraction of BREE’s “likely projects” are going to come on stream and the underlying capex cliff is therefore bloody enormous. Compare the above chart with April’s forecasts and you will see that the stock of actually “committed projects” has deteriorated a little for each of the next three years:

Remember that this is stock not flow. But the latter will follow the former, off the cliff.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.