Here’s Paul Bloxham’s latest in which he argues that rate hikes will be needed in the second half of 2014:

Growth is showing further signs of rebalancing – from being mining investment-led to being driven by the non-mining sectors. Low interest rates are lifting the established housing market and this month brought more evidence that the upswing in residential construction is picking up pace. There are also signs that the rebalancing is broadening, with the purchasing manager’s indexes for construction, manufacturing and services all rising. Helpfully, despite slowing down, mining investment has not yet fallen away sharply – it has levelled out – which is allowing more time for growth to rebalance.

The RBA will be heartened that its low cash rate setting is supporting Australia’s great rebalancing act. However, as noted in speeches by the Governor and Deputy Governor this month, it would still like financial conditions to be looser – to allow a faster rebalancing. The challenge is that it is unlikely to want to cut interest rates further to achieve this, for fear of over-heating the housing market. It would prefer a lower AUD: the recent modest decline in the currency would, no doubt, be welcome.

We expect the cash rate to be left on hold next week, at its historic low of 2.50%. What about 2014? Our central case is that the rebalancing of Australia’s growth will continue into 2014, supported by low interest rates and a modest decline in the AUD (we forecast it to be US86 cents by end-2014). The lower AUD is expected to be partly driven by tapering by the Federal Reserve, which we expect to begin by early 2014. In this central case, we expect that the RBA might have to start lifting rates in H2 2014, as the housing market boom continues, and we expect that a pick-up in growth and lower AUD will start to lift underlying inflation into the upper half of the RBA’s target band by then.

There are clearly risks to this view: weaker global growth, lower commodity prices, the lack of a Federal Reserve taper and AUD strength are key risks. Locally, tighter fiscal policy is a key risk, with next month’s mid-year budget update worth watching carefully.

Fair enough and such cyclical bullishnes now has the capex survey data to support it. But I still don’t agree.

The rebalancing we are seeing is still muted and the capex cliff is yet to appear. That does not mean it isn’t coming. It is very obvious in the stock of resource projects produced by BREE that the cliff still looms even if it has not yet materialised in official measures of the flow of spending (though go ask an engineering services firm about that).

Once it arrives in full, the capex cliff will continue for a long period. So I would couch things differently to Bloxo.

The delay in the full-throated tumble of capex is giving us a longer window than may have been feared to get other activity going. This is a positive. But it depends what kind of activity it proves to be. If the patchy housing recovery becomes a full blown beast then the RBA may be forced to act on rates (though macroprudential is still possible instead) in Bloxo’s time frame. In that event I do not expect a happy outcome as rate rises while capex falls is a recipe for instant stagnation or worse.

If housing slows and activity is derived from a lower dollar and improvements to competitiveness then they will be sustainable only so long as the RBA refuses to hike rates (unless we get a real dollar dump on an aggressive taper which is unlikely).

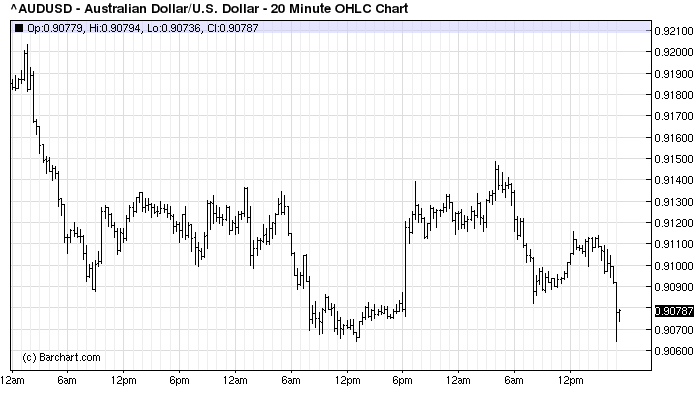

So, the base case remains that no hikes are coming in 2014 and further cuts are possible. I note that today both the Australian dollar and interest rate markets have sensibly discounting the capex report (though the former may be in part owing to North Asian tensions):

The risks for next year are also tilted to the downside. US housing is slowing. China’s current round of stimulus activity is peaking. In sum, rabalancing has won a little more time but it still faces formidable structural headwinds.