As CBA hits another record high today, two of Australia’s best bank analysts are warning about the sustainability of earning’s growth. From the AFR:

Without lower provisions for bad debts, earnings at the big four banks declined 0.2 per cent a share in the second half of 2012-13, according to calculations by investment bank UBS.

The analysis helps explain how the big banks continue to report record profits and pay higher dividends when demand for loans is subdued and other parts of the economy struggle to grow.

…Paul Siviour, the banking and capital markets leader of EY’s Oceania business, which is part of Ernst & Young, said the big four banks cut bad debt provisions by $1.1 billion over the past year.

“This raises an important question around the sustainability of this low level of provisioning,” he said.

…As a result of lower bad debts, modest revenue growth and cost control, they increased their dividends 11.2 per cent in 2013.

…As well as low interest rates, a change in international accounting rules for the provisioning of bad loans has contributed to the banks setting aside reduced reserves for bad loans.

…Previously, banks provisioned on an “expected” loss or dynamic provisioning basis.

CLSA analyst Brian Johnson said it was “definitely the case” that in benign economic times provisions were lower under the incurred-loss model than the expected-loss model.

Rather than smoothing out bad debts over the economic cycle, the banks are drawing down on provisions in good times in a pro-cyclical manner.

Nice one! APRA and its warnings about holding back capital is looking looking pretty silly in this context. But the real question here is what will the banks do to grow earnings ahead? Assuming costs are cut as far as possible already, the only way is to loosen standards and accelerate lending.

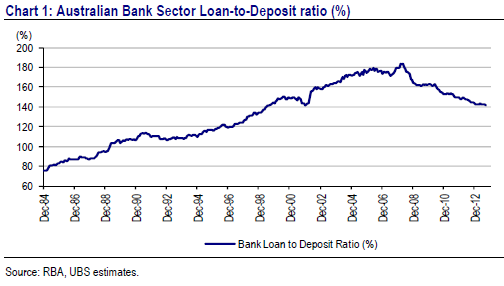

This brings me back to my notion of Australia’s credit cap. I’ve argued since the GFC that Australia can’t grow in its previous manner because by definition that means the banks’ extending wholesale (and largely offshore) borrowing. UBS offers a chart today that captures the conundrum:

The loan to deposit ratio is an imperfect measure (it has some offshore money in it) but shows roughly how APRA’s post GFC rules have forced banks to fund themselves much more through “sticky” deposits (mostly local). It has now stopped improving and I submit to you that unless this measure is allowed to blow out again then bank earning’s growth is going to come under pressure.

Truly the heat is on APRA.