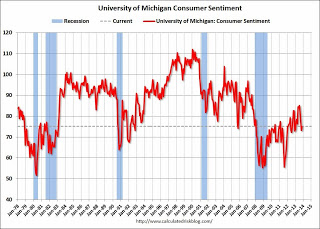

Another taper day on Wall St. The data was more strong than weak and supported my view that an inventory rebuild following the shutdown will keep US activity buoyant through year end. First up, final UMich Consumer Sentiment rebounded. From Calculated Risk:

The final Reuters / University of Michigan consumer sentiment index for November was at 75.1, up from the October reading of 73.2, and up from the preliminary November reading of 72.0.This was above the consensus forecast of 73.3. Sentiment has generally been improving following the recession – with plenty of ups and downs – and one big spike down when Congress threatened to “not pay the bills” in 2011.

The November Chicago Business Barometer softened to 63.0 after October’s sharp rise to a 31-month high of 65.9. November’s slight correction came amid mild declines in New Orders, Production and Order Backlogs after double digit gains in the prior month.

…“The Barometer might be down in November, but this was another impressive month with companies reporting firm growth”.“Having kept inventories lean for so long, a pick-up in demand has led to a sharp rise in stock building among the companies in our panel. And to handle the latest production and new orders boost, companies are hiring at the fastest pace for two years,” he added.

Advertisement

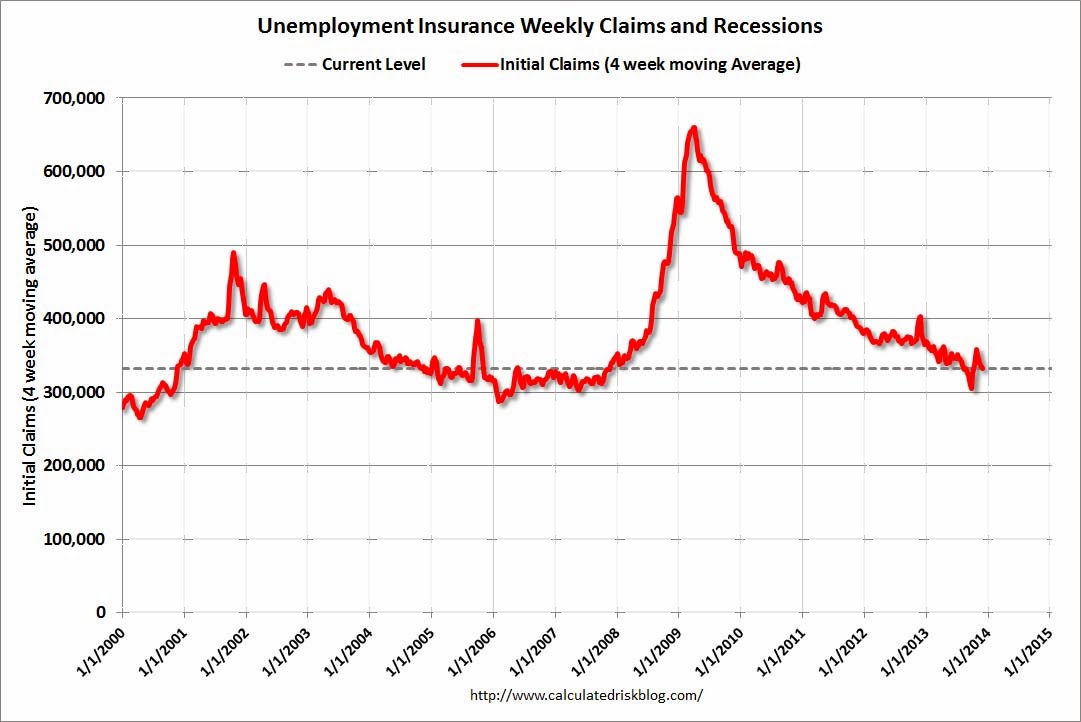

Consensus was for 60 so a decent beat. The same transpired for Weekly Jobless Claims (chart from CR):

In the week ending November 23, the advance figure for seasonally adjusted initial claims was 316,000, a decrease of 10,000 from the previous week’s revised figure of 326,000. The 4-week moving average was 331,750, a decrease of 7,500 from the previous week’s revised average of 339,250.

Mortgage applications decreased 0.3 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending November 22, 2013.

The Refinance Index increased 0.1 percent from the previous week. The seasonally adjusted Purchase Index decreased 0.2 percent from one week earlier.

…The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($417,000 or less) increased to 4.48 percent from 4.46 percent, with points decreasing to 0.31 from 0.38 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

In wider analysis, Merrill Lynch is bullish for next year:

Advertisement

As we have been arguing for more than a year, we think 2014 is the year when the economy finally exits rehab and starts growing at a healthy 3% (4Q/4Q). In our view, the economy would have already exited rehab this year if the politicians had not hit the economy with a double dose of austerity and confidence shocks. Two keys to better growth—the housing market and the banking sector—had already shown serious signs of improvement in 2012, with solid gains in home prices and construction and a modest improvement in bank lending.

… Absent the shocks out of Washington, we believe growth this year would have been 3 to 3.5%….Not only are structural headwinds fading, we expect Washington to be less shocking. While the sequester shock is not over—there is about a 0.2pp hit to GDP in 2014—the vast majority of the 2%-plus in fiscal austerity has already been absorbed into the economy. At the same time, with the election looming, we expect moderate politicians in each party to assert themselves and avoid another shutdown.

…While some of the cyclical bounce has already happened, it is important to recognize that the US is still in the early stage of the business cycle. Business cycles don’t die of old age, they die from overexpansion and inflation.

… In our view, the auto recovery is fairly well-advanced, but there is a long way to go in other consumer durables, housing, and business investment. Even more important…inflation seems a distant concern.

So long as you ignore assets of course. Meanwhile, Alan Greenspan appeared to talk down the economy. From Bloomie:

Greenspan said that even with the rise in equities, the U.S. economy is restrained by a “degree of uncertainty” that is reducing investment. Economists who forecast 2.5 percent to 3 percent growth next year may be too optimistic, he said.

“It’s a little on the upside, frankly,” Greenspan said. “There’s no doubt that there’s been some acceleration going on, but there’s an overall suppression that is going on in the economy” largely because of lingering uncertainty, he said.

Greenspan said his 2014 growth forecast is “closer to 2 percent.” That’s below the median estimate for a 2.6 percent expansion next year after a 1.7 percent growth this year, according to a Nov. 8-13 Bloomberg survey of 73 economists.

Advertisement

But talk up stocks:

Former Federal Reserve Chairman Alan Greenspan said the U.S. economy probably will grow more slowly next year than some forecasters predict and indicated that a near-record U.S. stock market isn’t in a bubble.

“This does not have the characteristics, as far as I’m concerned, of a stock market bubble,” Greenspan said in an interview on Bloomberg Television’s “Political Capital with Al Hunt,” airing this weekend. “It could come out that way but I don’t see it at this stage.”

I agree on growth but obviously not on bubbliciousness.

The upshot of all that was stocks to marginal new highs, long bonds selling off close to one percent, the US dollar rallying a little and gold, as well as the Aussie, falling half a percent. We might test the Aussie’s 2013 lows before too long.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.