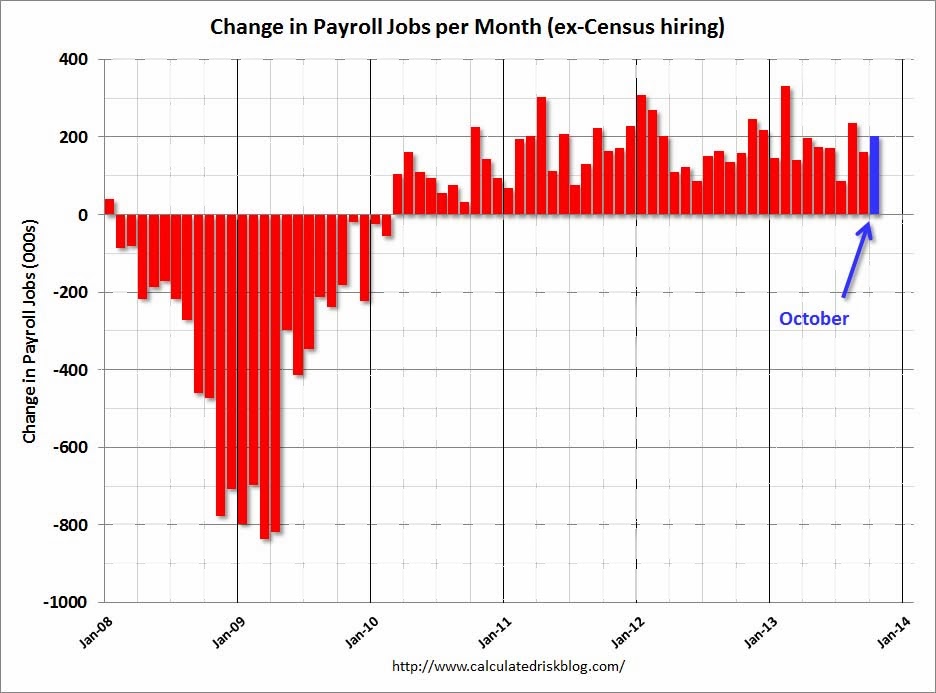

Total nonfarm payroll employment rose by 204,000 in October, and the unemployment rate was little changed at 7.3 percent, the U.S. Bureau of Labor Statistics reported today…Among the unemployed, however, the number who reported being on temporary layoff increased by 448,000. This figure includes furloughed federal employees who were classified as unemployed on temporary layoff under the definitions used in the household survey…The civilian labor force was down by 720,000 in October. The labor force participation rate fell by 0.4 percentage point to 62.8 percent over the month. Total employment as measured by the household survey fell by 735,000 over the month and the employment-population ratio declined by 0.3 percentage point to 58.3 percent. This employment decline partly reflected a decline in federal government employment…The change in total nonfarm payroll employment for August was revised from +193,000 to +238,000, and the change for September was revised from +148,000 to +163,000. With these revisions, employment gains in August and September combined were 60,000 higher than previously reported.

In these gloomy times, that’s as good a report as I can remember. There are shutdown distortions in the participation and employment-population rates. As well, the revisions to past months are excellent.

The report was so strong, in fact, that stock market fears of a taper were offset by excitement about growth. Note, finally, the strong seasonal pattern in US hiring, with the Christmas period dominating. So more solid reports over the next few months are a good bet.

Advertisement

But therein lies the problem. US long bonds ran for the door and yields spiked 3% to 3.85 on the 30 year, only 5 pips from breaking out. In short, we’ve quickly returned to where we were pre-shutdown, with an interest rate back-up threatening housing and the consumer.

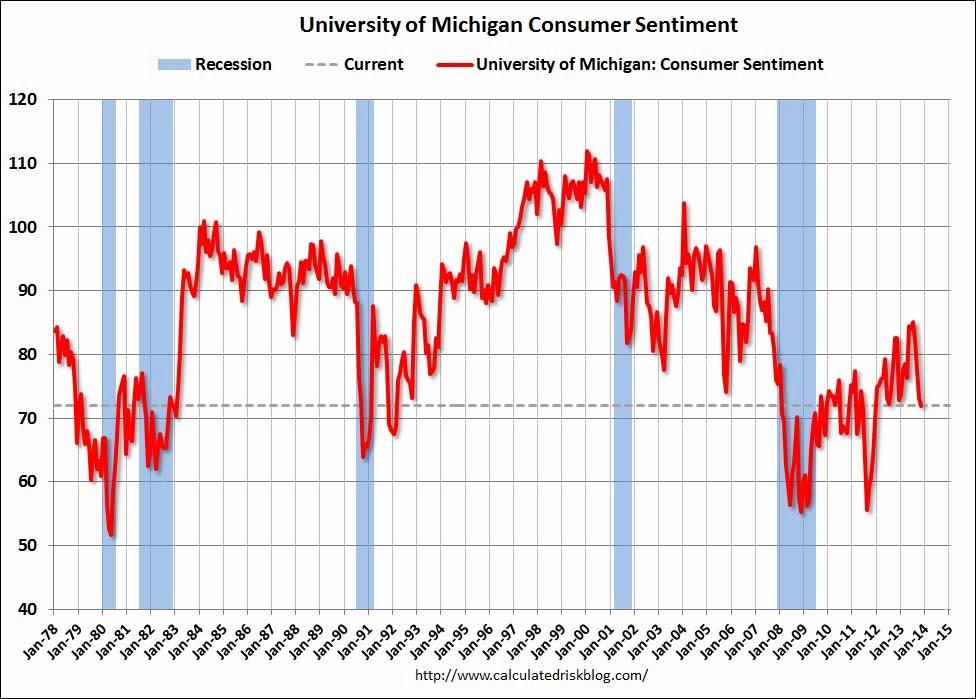

That showed up to some extent in the preliminary Michigan Consumer Sentiment Survey, which fell solidly for October (chart from Calculated Risk):

The preliminary Reuters / University of Michigan consumer sentiment index for November was at 72.0, down from the October reading of 73.2. This was below the consensus forecast of 75.0.

Advertisement

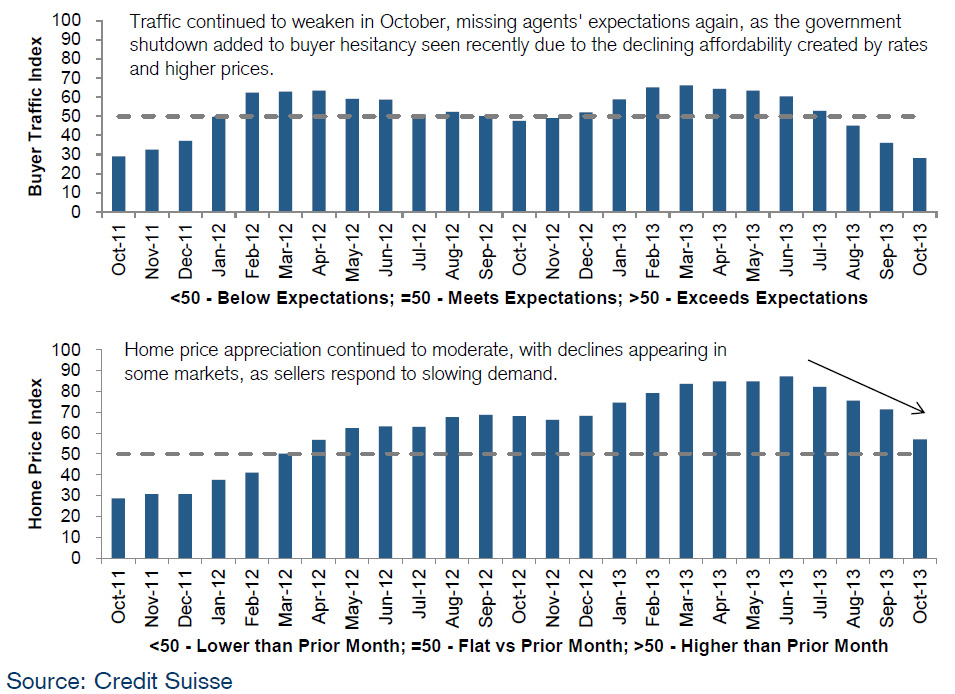

Also shutdown affected. But I do not expect the rebound this time to be as complete as it was following the 2011 shutdown. Rising interest rates are not the consumer’s friend. Credit Suisse runs a monthly housing turnover barometer and the trend is clear:

Also shutdown affected but the trend is not the Fed’s friend.

Advertisement

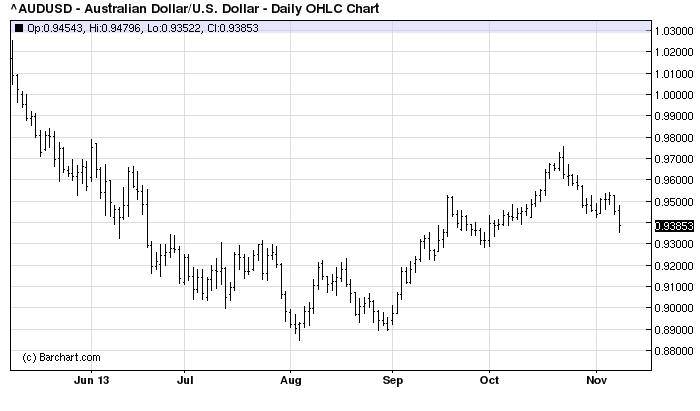

The net result of all was, however, that markets swung decisively towards an imminent taper. The US dollar jumped, gold was hammered 2% and the Australian dollar was decidedly risk off, down 1 cent against the greenback and half cent against just about everyone else. Indeed, the Aussie suddenly has a very positive bearish chart with a head shoulders top:

If we can take out 93 cents then it’s free fall time.

Advertisement

Still, I can’t yet buy the taper. Not this year, for sure. We have to get past the fiscal mess so March is the earliest. A favourable outcome then, with reduced fiscal drag, would bring it on. But by then I expect the US housing slowdown to be very obvious so anything other than a glowing fiscal outcome and it’s more delay.

The conundrum remains: how can the Fed exit and not pop the bond bubble as well as send housing markets into a tail spin? As such it’s still a delay for me, any taper that does eventually come will be puny and followed by endless low interest rates.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.