The Fed minutes were out last night and the taper is back on:

Participants generally saw the direct economic effects of the partial shutdown of the federal government as temporary and limited, but a number of them expressed concern about the possible economic effects of repeated fiscal impasses on business and consumer confidence. More broadly, fiscal policy, which has been exerting significant restraint on economic growth, was expected to become somewhat less restrictive over the forecast period. Nonetheless, it was noted that the stance of fiscal policy was likely to remain one of the most important headwinds restraining growth over the medium term.

…During this general discussion of policy strategy and tactics, participants reviewed issues specific to the Committee’s asset purchase program. They generally expected that the data would prove consistent with the Committee’s outlook for ongoing improvement in labor market conditions and would thus warrant trimming the pace of purchases in coming months.

Advertisement

…As part of the planning discussion, participants also examined several possibilities for clarifying or strengthening the forward guidance for the federal funds rate, including by providing additional information about the likely path of the rate either after one of the economic thresholds in the current guidance was reached or after the funds rate target was eventually raised from its current, exceptionally low level. A couple of participants favored simply reducing the 6-1/2 percent unemployment rate threshold, but others noted that such a change might raise concerns about the durability of the Committee’s commitment to the thresholds. Participants also weighed the merits of stating that, even after the unemployment rate dropped below 6-1/2 percent, the target for the federal funds rate would not be raised so long as the inflation rate was projected to run below a given level. In general, the benefits of adding this kind of quantitative floor for inflation were viewed as uncertain and likely to be rather modest, and communicating it could present challenges, but a few participants remained favorably inclined toward it. Several participants concluded that providing additional qualitative information on the Committee’s intentions regarding the federal funds rate after the unemployment threshold was reached could be more helpful. Such guidance could indicate the range of information that the Committee would consider in evaluating when it would be appropriate to raise the federal funds rate. Alternatively, the policy statement could indicate that even after the first increase in the federal funds rate target, the Committee anticipated keeping the rate below its longer-run equilibrium value for some time, as economic headwinds were likely to diminish only slowly. Other factors besides those headwinds were also mentioned as possibly providing a rationale for maintaining a low trajectory for the federal funds rate, including following through on a commitment to support the economy by maintaining more-accommodative policy for longer. These or other modifications to the forward guidance for the federal funds rate could be implemented in the future, either to improve clarity or to add to policy accommodation, perhaps in conjunction with a reduction in the pace of asset purchases as part of a rebalancing of the Committee’s tools.

Participants also discussed a range of possible actions that could be considered if the Committee wished to signal its intention to keep short-term rates low or reinforce the forward guidance on the federal funds rate. For example, most participants thought that a reduction by the Board of Governors in the interest rate paid on excess reserves could be worth considering at some stage, although the benefits of such a step were generally seen as likely to be small except possibly as a signal of policy intentions. By contrast, participants expressed a range of concerns about using open market operations aimed at affecting the expected path of short-term interest rates, such as a standing purchase facility for shorter-term Treasury securities or the provision of term funding through repurchase agreements. Among the concerns voiced was that such operations would inhibit price discovery and remove valuable sources of market information; in addition, such operations might be difficult to explain to the public, complicate the Committee’s communications, and appear inconsistent with the economic thresholds for the federal funds rate. Nevertheless, a number of participants noted that such operations were worthy of further study or saw them as potentially helpful in some circumstances.

As well as hawkish minutes, FOMC dove James Bullard was out suggesting Dectaper is possible if the November employment report is strong.

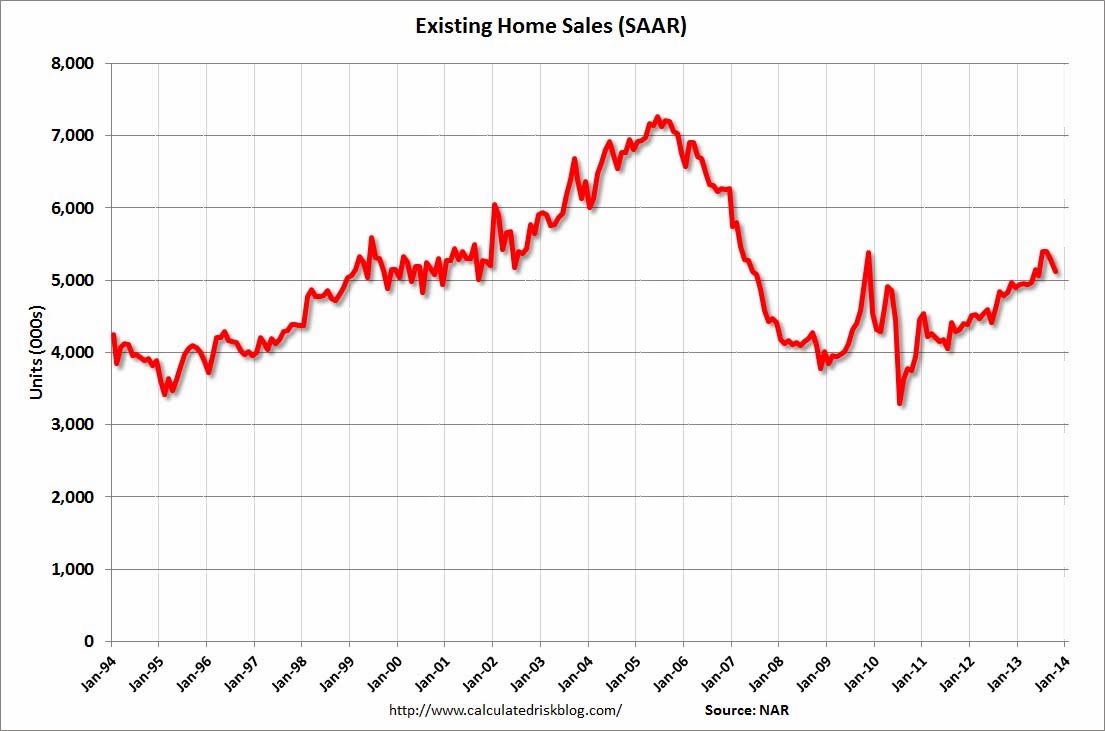

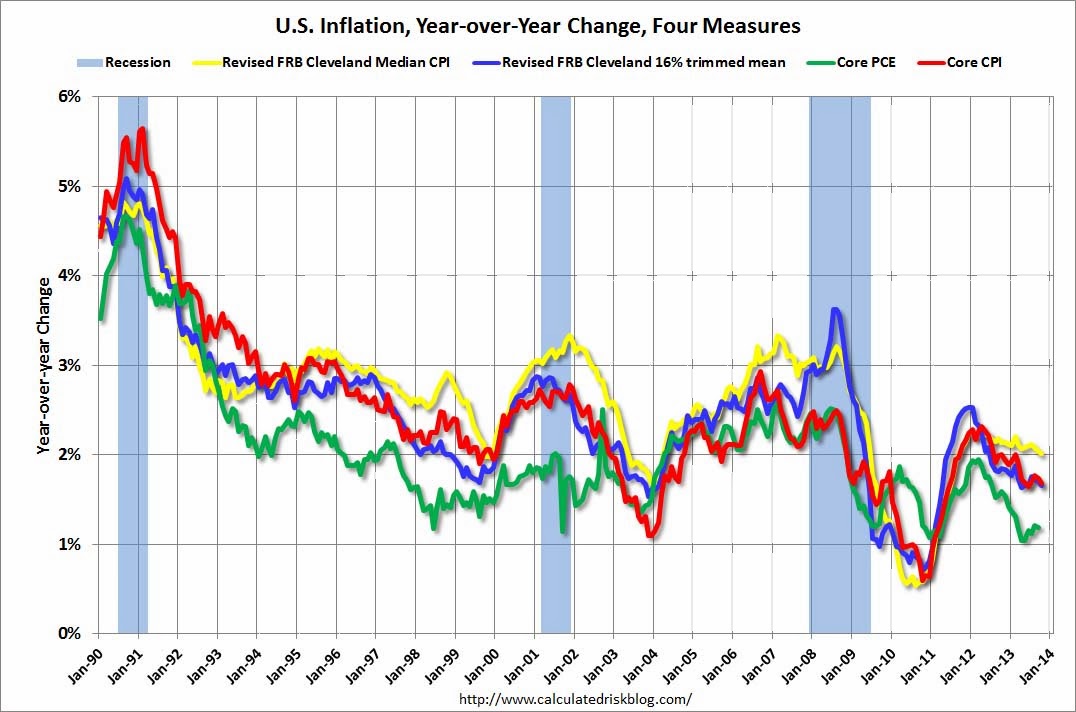

This followed an evening of largely taper-unfriendly data. On the soft side, existing home sales fell (all charts from Calculated Risk):

Advertisement

Total existing-home sales, which are completed transactions that include single-family homes, townhomes, condominiums and co-ops, fell 3.2 percent to a seasonally adjusted annual rate of 5.12 million in October from 5.29 million in September, but are 6.0 percent higher than the 4.83 million-unit level in October 2012.

Total housing inventory at the end of October declined 1.8 percent to 2.13 million existing homes available for sale, which represents a 5.0-month supply at the current sales pace; the relative supply was 4.9 months in September. Unsold inventory is 0.9 percent above a year ago, when there was a 5.2-month supply.

Mortgage applications decreased 2.3 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending November 15, 2013. This week’s results include an adjustment to account for the Veteran’s Day holiday.

The Market Composite Index, a measure of mortgage loan application volume, decreased 2.3 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 13 percent compared with the previous week. The Refinance Index decreased 7 percent from the previous week. The seasonally adjusted Purchase Index increased 6 percent from one week earlier. The unadjusted Purchase Index decreased 8 percent compared with the previous week and was 3 percent lower than the same week one year ago.

…The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($417,000 or less) increased to 4.46 percent from 4.44 percent, with points decreasing to 0.38 from 0.44 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans. The effective rate decreased from last week.

According to the Federal Reserve Bank of Cleveland, the median Consumer Price Index rose 0.1% (1.4% annualized rate) in October. The 16% trimmed-mean Consumer Price Index also increased 0.1% (1.1% annualized rate) during the month. The median CPI and 16% trimmed-mean CPI are measures of core inflation calculated by the Federal Reserve Bank of Cleveland based on data released in the Bureau of Labor Statistics’ (BLS) monthly CPI report.

Earlier today, the BLS reported that the seasonally adjusted CPI for all urban consumers fell 0.1% (-0.7% annualized rate) in October. The CPI less food and energy increased 0.1% (1.5% annualized rate) on a seasonally adjusted basis.

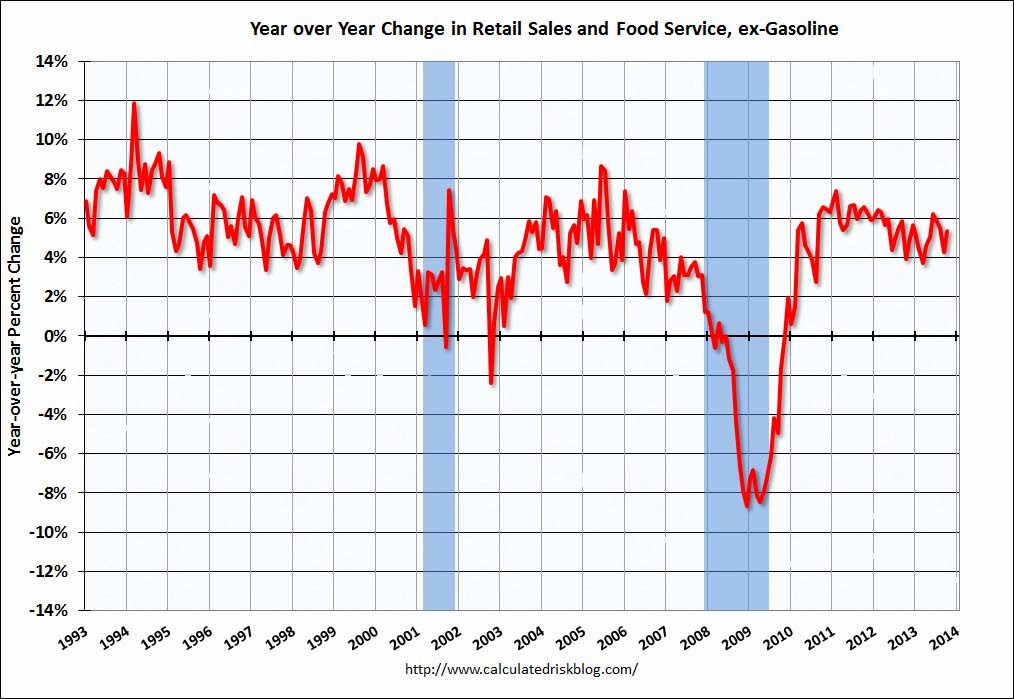

But retail sales were solid for October, ignoring the shutdown:

The U.S. Census Bureau announced today that advance estimates of U.S. retail and food services sales for October, adjusted for seasonal variation and holiday and trading-day differences, but not for price changes, were $428.1 billion, an increase of 0.4 percent from the previous month, and 3.9 percent above October 2012. …The August to September 2013 percent change was revised from -0.1 percent to virtually unchanged.

Advertisement

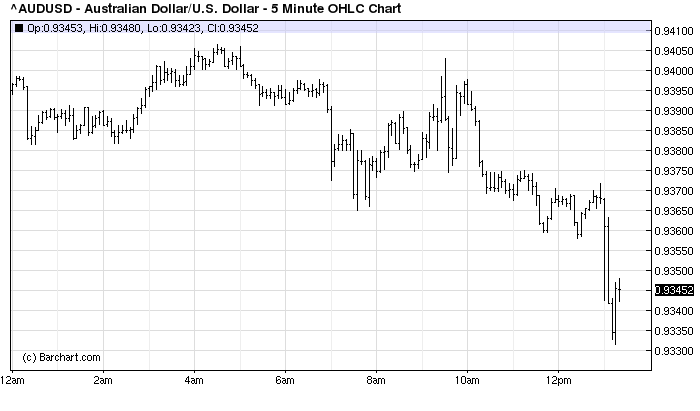

Mixed data but the Fed tipped the scales heavily towards taper and the 30 year yield jumped 3% to 3.9o%, right on a breakout. The Fed may taper but rates are not going to play nice. Stocks reversed earlier gains on the mediocre data. The US dollar rose half a percent, gold was crushed 2% and broke support and the Australian dollar sagged one percent but is still above support around 92.8:

With Capt’ Glenn delivering a bellwether speech today on Thirty years of Floating, he’s surely going to kick it while it’s down.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.