In case you didn’t know, last the Australian Office of Financial Management released its annual report last night and there are few tidbits worth a mention. First, the AOFM RMBS portfolio continues to deliver you a modest return. You may recall that:

The Australian residential mortgage-backed securities (RMBS) market is acknowledged as a critical source of funding for smaller mortgage lenders. The global financial crisis that started in 2007-08 reduced the availability of funding through the Australian RMBS market, which limited mortgage lenders’ access to funding and in turn their ability to offer competitive mortgage products.

In response, the Government decided to invest in Australian RMBS to support competition in lending for housing during the market dislocation. In October 2008 the

Treasurer directed the AOFM to invest up to $8 billion in eligible RMBS, of which up to $4 billion was to be invested in deals with sponsors that were not ADIs (Authorised Deposit-taking Institutions). In November 2009 the Treasurer extended the program by directing the AOFM to invest up to a further $8 billion in RMBS. This Direction also extended the objectives of the program to include supporting small business lending, through broadening the potential use of funds raised under the program.In December 2010 the Treasurer announced, as part of the Competitive and Sustainable Banking System package, a further extension of the program. The subsequent Direction, issued in April 2011, directed the AOFM to invest up to an additional $4 billion and thus a cumulative total of up to $20 billion in RMBS. Importantly, this direction also identified the need to encourage a transition towards a market not reliant on Government support.

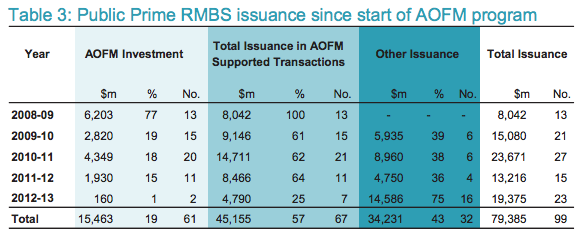

Here are the details of where the AOFM put your money:

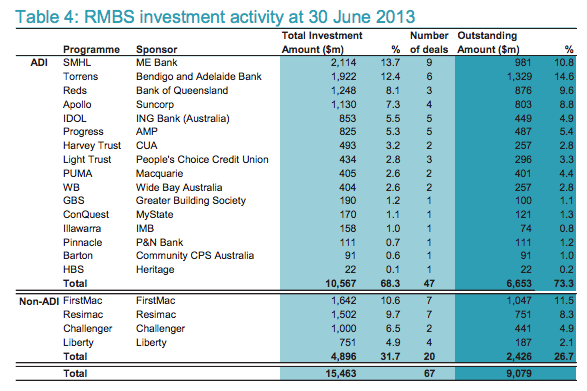

And here is your performance to date:

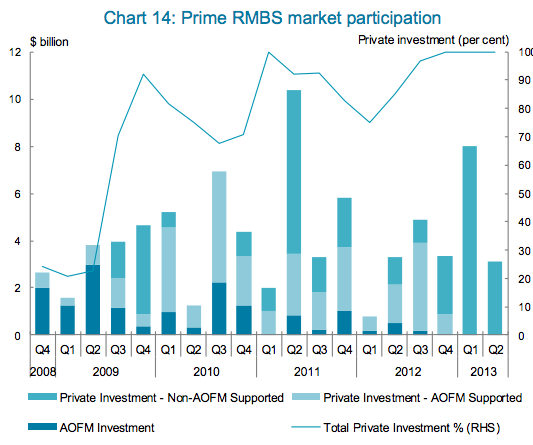

The funds raised by the RMBS issues supported by the AOFM have provided an important component of total lending for housing and small business since the inception of the program. Without this funding, new lending by the financial institutions supported would have been lower and would have impacted the extent of

competition in the market.The investments made under the program continue to provide reasonable financial returns. Interest income in 2012-13 was $472.6 million. In addition, sales through the year contributed a further $5.3 million in incremental income. Total income of $478 million represented an annualised return of 4.62 per cent on the average portfolio book value of $10.3 billion. The average margin over the one month bank bill rate (weighted by each of AOFM’s investments) for the book outstanding as at 30 June 2013 remained around 133 basis points. Capital repayments as at the end of the year totalled $6.4 billion.

The RMBS securities held by the AOFM are valued using indicative margins for secondary market trading as estimated by an independent valuation service provider. Furthermore, market bid rates are used for these purposes. Accordingly, the RMBS portfolio was valued at $9.1 billion as at 30 June 2013, implying an unrealised gain of $17 million (or 0.19 per cent of the portfolio book value). This represents an improvement in the value of the portfolio of around $170 million for the year. Losses or gains in the mark-to-market value of the portfolio change with prevailing conditions and therefore vary at any particular point in time. They are not realised losses or gains, but are referred to as re-measurements.

Remember that the money was borrowed at a rate of 3% or so on the ten year bond so it’s a pretty lousy return you’re getting for wearing the risk. Add in the second outcome of a conga line of bankers with their hands out, instead of spending their days thinking of ways to service you better, and the yield is pretty bloody awful.

Some will argue that this supported competition, but if it did, it is only between which bank and non-bank can get to the tax-payer’s door the quicker.

This is definitely something that the Hockey Inquiry must address. As it stands, these purchases are only idled and can recommence at the drop of a hat. The moral hazard is awesome.