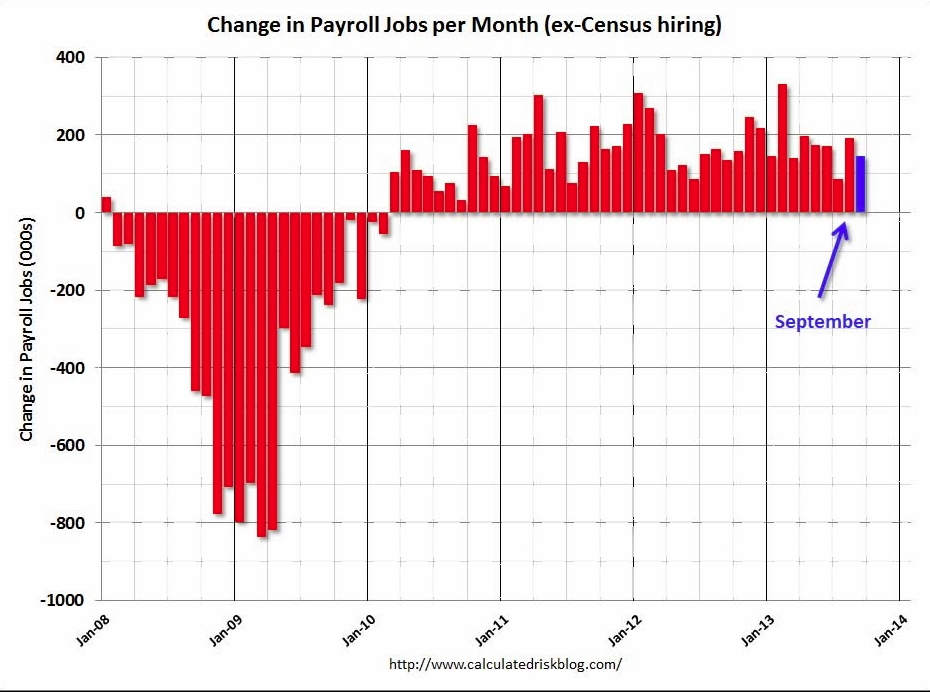

The delayed US jobs report from the BLS is out and is a continuation of the recent past’s weak reports:

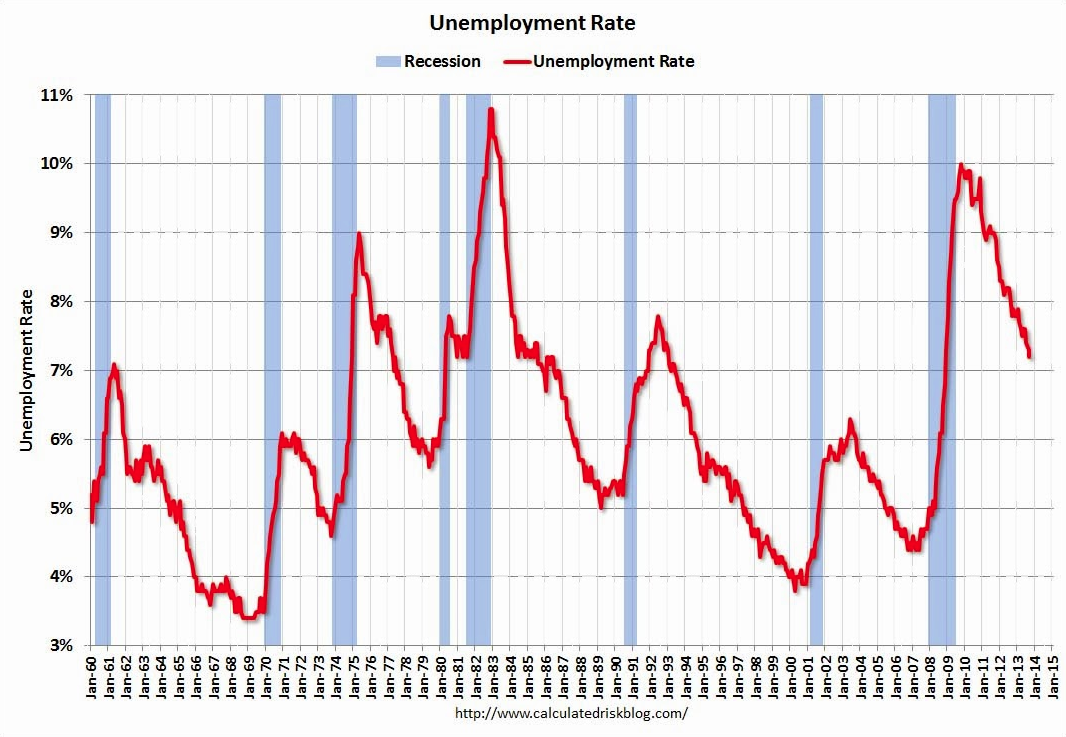

Total nonfarm payroll employment rose by 148,000 in September, and the unemployment rate was little changed at 7.2 percent, the U.S. Bureau of Labor Statistics reported today. ……The change in total nonfarm payroll employment for July was revised from +104,000 to +89,000, and the change for August was revised from +169,000 to +193,000. With these revisions, employment gains in July and August combined were 9,000 more than previously reported.

Here’s the view from Goldman Sachs:

The unemployment rate ticked down, but benefitted from favorable rounding and a small decline in the participation rate on an unrounded basis. Although December remains a possibility, this report makes it more likely that the Fed pushes the first reduction in the pace of its asset purchases into 2014. While the uncertainty is considerable, we think that March is the most likely date under our economic forecast, and the assumption that the next set of fiscal deadlines proves less disruptive than the most recent set.

MAIN POINTS:

1. Payroll employment rose 148k in September (vs consensus 180k). While August employment growth was revised up?as has been the typical pattern in recent years?July employment growth was revised down, leaving the net revision to the prior two months only +9k. By industry, all of the slowdown in job growth relative to August was found in private service-providing industries, as employment in leisure and hospitality fell 13k (vs. +21k in August) and employment in health and education services rose only 14k (vs +61k in August). In contrast, construction employment rebounded (+20k), potentially due in part to more favorable weather in September, while government added 22k jobs, entirely due to the state and local sector. This morning’s report leaves the 3-month trend in payroll job growth at +143k and the 12-month trend at +185k.

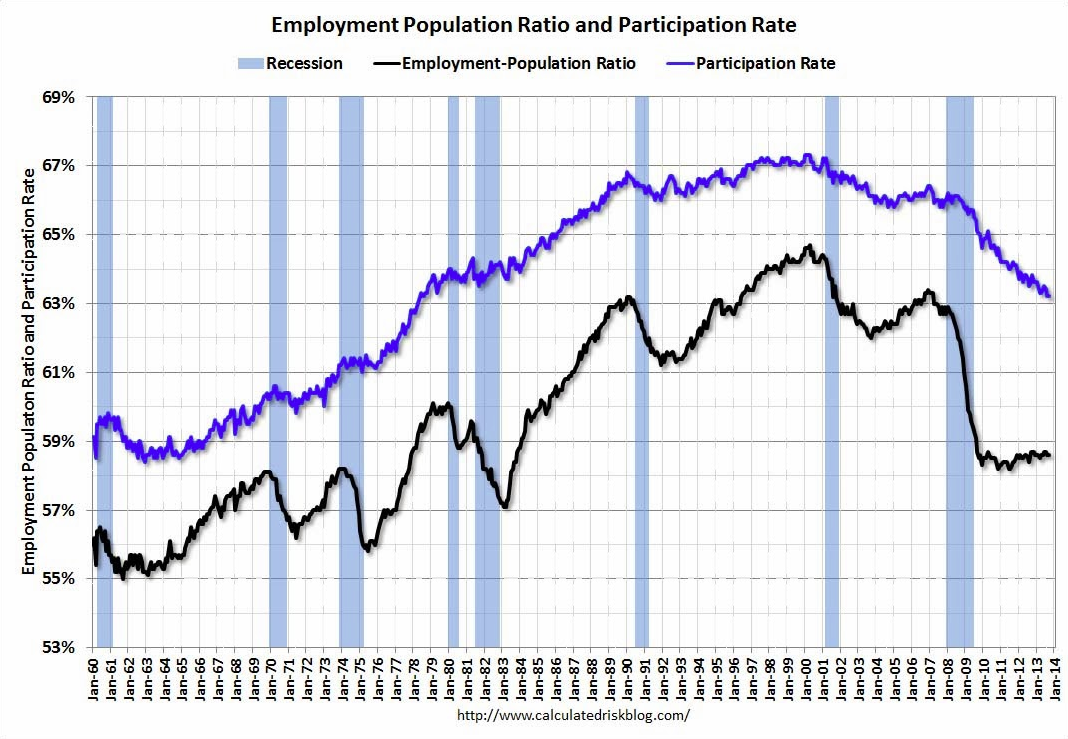

2. The unemployment rate declined by one-tenth to 7.2% to one decimal place (vs consensus 7.3%). On an unrounded basis, the decline was a smaller four basis points to 7.235%. Although employment grew by 133k according to the household survey, on a payroll-consistent basis?adjusting for definitional differences between the two surveys?employment declined 195k. While the labor force participation rate held constant to one decimal place at 63.2%, on an unrounded basis the rate continued to edge down slightly.

3. Average hourly earnings grew only 0.1% in September (vs consensus +0.2%), leaving the 12-month rate of increase at 2.1%. The average hourly workweek was unchanged at 34.5. The index of aggregate weekly hours?the product of workers and hours per worker?grew at an only-modest 1.1% annual rate during Q3.

4. Although December remains a possibility, this report makes it more likely that the Fed pushes the first reduction in the pace of its asset purchases into 2014. While the uncertainty is considerable, we think that March is the most likely date under our economic forecast, and the assumption that the next set of fiscal deadlines proves less disruptive than the most recent set. We continue to expect the first increase in the fed funds target rate in 2016 Q1.

5. With the employment report, manufacturing data, and sentiment surveys in hand, we start our September CAI at 2.6%, down from 3.1% in August.

There is a small chance this could be right. As I’ve noted before, the last debt-ceiling shock set off a little inventory cycle that could boost jobs for six months. But I still reckon this is long shot. The Fed will know this and want to see more persuasive evidence of an enduring jobs recovery. Check out the tumbling participation rate in the above charts. It appears headed back to pre-sexual revolution levels. And that’s before we get to round two of budget negotiations and the fiscal drags contemplated there. The tumbling US dollar appears to agree.

But at the AFR, Bill Lee, a former US Federal Reserve economist and International Monetary Fund financial stability expert, is warning about bubbles in housing and share markets worldwide:

“One of the things we are concerned about is if you put all of this extra liquidity out into the economy and distort financial markets by pushing people into risky assets – namely equities – what will that do to financial stability?

…He said it was important the Fed begin to wind back its $US85 billion monthly bond-buying program, which has helped sharemarkets around the world to surge.

“It’s better to start hauling back on this stuff as soon as you can…The private sector, ex-government, is actually doing quite well,” Mr Lee said.

…After the US last week ended its 16-day government shutdown and avoided defaulting on its debts, Mr Lee said the country was facing a “trifecta” of problems: rising entitlement spending, an ageing population and high debt.

…It was a misnomer that incoming Fed chair Janet Yellen was a “dove” on monetary policy, Mr Lee said.

“Back in the day of Greenspan, she was the first to say ‘hey you’ve got to raise rates’. The right way to characterise her is that she is an activist policymaker.”

We shall see.