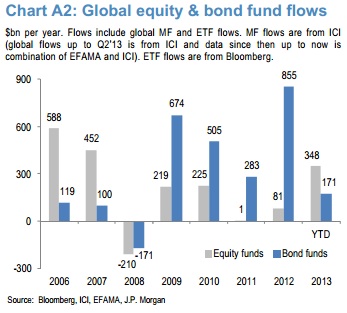

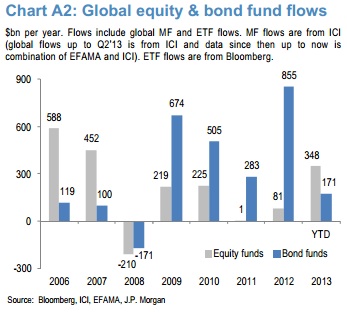

Year-to-date buying of $171bn of bond funds is relatively healthy by historical standards, helped by what we previously called the “saving motive” of bond fund demand, i.e. zero or close to zero policy rates are inducing retail investors to replace money funds with bond funds as their preferred saving vehicle. We estimate that more than 70% of the YTD bond fund inflow globally reflects outflows from money funds.

…With data/reports only available for Australia, China, Korea, Kuwait, Libya, Singapore, UAE, New Zealand and Norway, we calculate that the AUMweighted allocation to public equities for SWFs was 56% in 2012 followed by 25% for bonds. Cash and other alternatives were at 6% and 13% respectively.

…The world’s largest SWF, Norway’s Government Pension Fund, appears to have refrained from buying equities in Q3 this year, following purchases of $12.8bn and $24.4bn in Q1 and Q2 respectively. In fact they sold a small amount of equities in Q3 They instead bought $15.6bn of bonds in Q3, up from $7.7bn and $10.3bn in Q1 and Q2 respectively.

The fund has set a strategic allocation of 60% in equities, 35% in bonds and 5% in real estate. In Q3 2013, the Government Pension Fund’s allocation to equities increased to 63.6%, its allocation to bonds fell to 35.5% while real estate accounted for 0.9%. So at the end of Q3, Norway’s Sovereign Wealth Fund was overweight equities and underweight in real estate relative to their strategic targets.

It seems likely that given the strong rise in equity markets this year, many of these Sovereign Wealth Funds are currently overweight in equities. This could induce them to either take some profit in the coming quarters or invest a higher portion of their incoming funds to bonds or alternatives rather than equities.

So bonds are still more in favour than in the past. As Alphaville notes, what appears to be happening is a general inflation of all asset classes driven by financial repression everywhere. For me this confirms again how vulnerable to reversal the economic and asset price cycle remains. Enjoy it but do not believe in it.

Advertisement

About the author

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

Advertisement