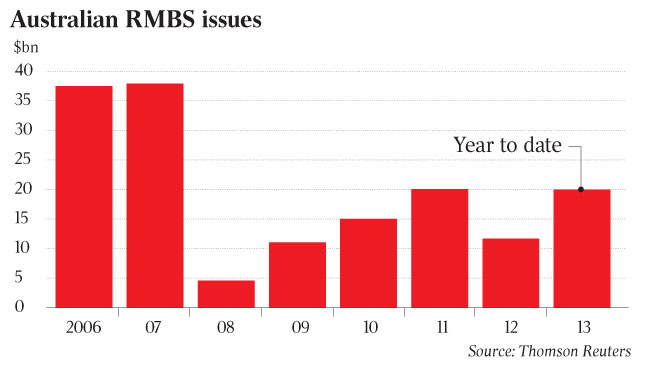

HOME-LOAN lenders are on track to this year raise the most money from securities backed by mortgages since the global financial crisis, boosting competition as the property market picks up steam.

…Last week, non-bank lender Pepper Australia upsized a non-conforming RMBS deal to $350 million, from $300m, after strong demand. Signalling the level of appetite, Pepper’s deal priced even as credit markets were stalled by the prospects of the US defaulting on its debt obligations.

…”It does feel very, very healthy,” said Mr Arnold. “It’s likely to continue, with similar volumes next year from a number of the banks. The market has been able to remain open over some reasonably volatile periods, like the issues with the US debt ceiling, which is not conducive to transactions.”

Hmmm, well, sort of. It’s not the market it once was, nor is it as healthy as this story is making out. But it has certainly bounced back. Remember that in recent years it only functioned because you subsidised it via your taxes buying various tranches.

Last week was an example of some recent robustness. But the fact is, except at the very short end, credit markets all ignored the US debt-ceiling debacle. The Pepper issue was non-conforming and priced at 120bps over BBSW. It included 10 domestic and two international investors. Compared with pre-GFC levels when RMBS was swamped by foreign investors, and spreads were at 10 or 20 bps, the market is still positively sick.

As well, earlier this year, when Chinese markets seized up for a month or so, RMBS pricing was no so sanguine and suddenly got uneconomic.

Bank CDS prices today remain at 107bps so the general credit environment is solid versus the recent past but these prices are still above the post-European crisis floor around 100bps (after a brief dip to 70bp early this year).

But I’m afraid any enduring shock will close the RMBS market again, unless the government supports it quick smart. It’s still another banking quango.

Advertisement

About the author

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

Advertisement