Can we stop with the ‘central bankers are powerless’ line now? Glenn Stevens hammered the dollar lower yesterday with a blunt warning:

Another part of the balanced growth path would involve an expansion in some of the trade-exposed sectors that have been squeezed by the high exchange rate. The foreign exchange market is perhaps another area in which investors should take care. While the direction of the exchange rate’s response to some recent events might be understandable, that was from levels that were already unusually high. These levels of the exchange rate are not supported by Australia’s relative levels of costs and productivity. Moreover, the terms of trade are likely to fall, not rise, from here. So it seems quite likely that at some point in the future the Australian dollar will be materially lower than it is today.

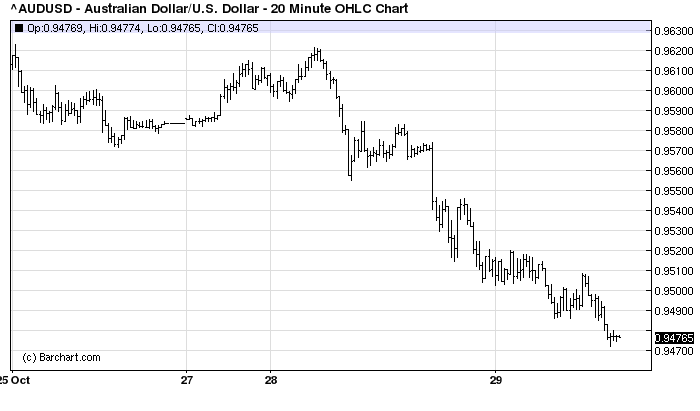

The dollar kept falling last night, even as markets went bald-faced “risk on”:

Yes, the US dollar rose but the Aussie undershot everything:

So, why did it work yesterday? In a word: fear. For the first time, Captain Glenn put fear into markets that the Aussie is not a one way bet. His speech was by some distance the most blunt warning that the RBA has delivered to currency bulls. Second, he’s just had his balance sheet juiced and that has given markets reason to wonder if the RBA won’t come after the longs. The bank could wade into options markets with $9 billion and force major squeezes either way if it wanted to.

Perhaps the good Captain was helped by the timing of yesterday’s PBOC moves, as it injected liquidity into Chinese money markets but tightened rates as well. But that is all part of the jawboning art form, finding the right moment. Besides, as said, markets were generally “risk on”.

Warwick McKibbin chimed into the debate yesterday to argue that the RBA should give up affecting the dollar:

“Monetary policy should be on neutral because it can’t fix structural problems [caused by the high dollar],” professor McKibbin told <i>The Australian Financial Review</i>. “We’ve got to get away from the idea that monetary policy is the policy of last resort – we always lean on it for every shock.”

Professor McKibbin, who left the board last year, called on both sides of politics to adopt an alternative “two-pronged attack” by using debt to fund quality infrastructure projects and tackle the nation’s high cost base, including wages, green tape and energy prices. “Nothing we do on the exchange rate is going to do much for competitiveness. We have to do it on input costs because it looks like the exchange rate is going to keep heading north.”

“I don’t know why they kept putting rates down [to 2.5 per cent],” he said. “I would have stopped at 3 per cent or 3.5 per cent and made the argument that [the dollar] is not a problem they could fix.”

With respect, this is not Europe and the currency is still floating. If the RBA had stopped cutting at 3.5% then the Australian dollar could very well be flirting with a record high right now which would most likely have us close to or already in recession as the mining boom went bust, fiscal instability spread and consumers spent every penny they could offshore.

I’m a fan of the Austrian approach to business cycles and would embrace a small recession if I thought it would serve the purpose of cleaning out bad bets. As well, McKibbin is absolutely right that we need a wage freeze, need to raise productivity and to improve infrastructure to restore competitiveness.

But these measures alone won’t engineer the magnitude of real exchange rate adjustment required to get a sustained rebalancing away from mining going. Or, more to the point, the level of asset and labour price deflation required to pull it off would be a decadal shock to the economy and, with historically leveraged household balance sheets, I have grace concerns we’d push ourselves into a deflationary spiral to rival peripheral Europe.

I entirely agree with McKibbin’s previously made point that as we speak low interest rates are triggering widespread capital misallocation in the economy. But the right approach was (and remains) to break the interest rate-currency nexus either through macroprudential tools or Tobin taxes. I doubt the efficacy of the latter and know the former works so opt for it.

The fact is, the RBA can lower the Australian dollar any time it chooses. It’s actions are an huge component in the currency’s value. Which brings us to the final reason that yesterday worked so well. Such short term movements won’t last unless accompanied by actions. Yesterday’s RBA speech hinted that such action was possible. It warned on the currency, housing markets and lending standards, the three components that come together in macroprudential rules which, if installed, would terrify currency longs. That warning was reinforced in a speech by APRA chairman John Laker:

A sustained period of low interest rates can mask the creditworthiness of borrowers, and the combination of keen borrowers and buoyant housing markets can be temptations to brake the shackles of low volume growth and lend aggressively. If the benefits of low interest rates are to prove enduring, it is essential that ADIs, mutual and otherwise, maintain prudent lending standards and a clear understanding of borrowers’ circumstances and their capacity to service debt. Low interest rates can also encourage a ‘search for yield’ to compensate for lower returns from traditional investments and other activities. Such a search should not take ADIs into new markets or activities without robust due diligence and appropriate risk management.

Housing markets have been heating up in some capitals and, no doubt, temptations may be growing. Let me help you to resist their siren song! And how might that song sound?

…One area of higher risk that APRA is monitoring closely is high loan-to-valuation ratio (LVR) housing lending. You may be aware that the Reserve Bank of New Zealand has placed speed limits on this type of lending in their market. We are keeping our powder dry on that option but we will take supervisory action if an ADI is skewing its housing loan portfolio too heavily in favour of high LVR lending. We are also monitoring interest-only lending to owner-occupiers more closely, so that we can understand whether this is sensible lending or a speculative play by the borrower.

Transferring part of the risk to lenders mortgage insurers (LMIs) does not negate your responsibility to maintain the quality of the lending book and to ensure that all the terms and conditions of LMI policies are met. Just as you would not accept a lending policy that says serviceability does not matter as long as there is sufficient security, you should not accept a lending policy that says security values do not matter as long as there is lenders mortgage insurance.

I don’t recall APRA describing macroprudential rules as an “option” before. This is much better stuff from our regulatory pair and just such a discussion should be formerly ramped up henceforth.