Recent RBA statements suggest the central bank is comfortably on hold and we have decided it is more likely that the next easing of policy will be delayed until February.

However, the big picture remains intact with the economy expected to under perform over the year ahead, more so for domestic demand, leading to rising unemployment.

Higher unemployment and the commensurate downward pressure on inflation will be the triggers for a further easing by the RBA but probably not until early 2014.

We still do not see upward movements in the cash rate until 2015.

For months NAB’s view has been that the RBA would react to a softening economy ahead and come back with more monetary accommodation. That big picture view remains firmly intact.

Indeed, our analysis suggests that the economy will slow, with GDP growth softening to around 2% by the end of the year, rising to a still sub-trend 3% by the end of 2014. Private domestic demand is even worse in our forecasts, slipping to about 1¼% by the end of 2013 and likely to be near flat through 2014. GDP is stronger only because net exports will keep rising, as new resources projects come on stream with substantial contributions to annual GDP of about 1.8 percentage points through 2014. With the Federal Government shedding jobs, this is a recipe for rising unemployment, which, in our view, will peak at 6¾% in the second half of 2014. Higher unemployment means slower wages growth and, in turn, downward pressure on underlying inflation. Essentially, this evolution of the economy will convince the RBA of the need for a more accommodative monetary policy stance.

While this big picture story remains well and truly in place, the RBA’s recent statements have indicated that Board members are comfortable enough with recent developments and there is no imminent interest rate cut coming.

Yesterday’s post meeting statement noted that business and consumer confidence had improved but said it was too early to judge how persistent this will be (and we would add, to what extent this leads to stronger activity). The statement also noted that savers were moving out of declining returns in low-risk assets. That is in keeping with the view that the traditional transition mechanism of monetary policy may be starting to gain traction. While not the same thing as worrying about a housing bubble, clearly the extent to which house price inflation accelerates will be watched carefully. Both of these ‘new’ comments are consistent with the RBA waiting for a while before considering any further easing.

Accordingly today, we have decided to delay our rate cut call from November to February, allowing the RBA time to pause and watch the data. With the big picture still unmoved, we continue to see a cut coming but right now there is no rush.

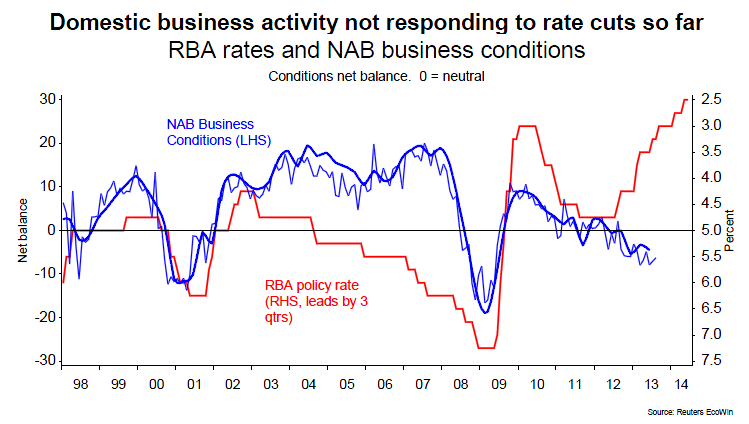

As the chart above shows, to date the domestic economy has not responded to the lower nominal cash rate. Part of that story may reflect the impact of a still high currency on monetary conditions.

I agree with this and can only repeat that we had macroprudential in place so rates can go lower and the dollar far lower as well. Only then will we recover.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.