With the Syria premium effectively removed from the Gold market in early September as the Russian brokered deal to dismantle Syrian chemical weapons capability diminished the possibility of a military intervention, the market again focused on the issue of US tapering.

The Federal Reserve surprisingly kicked the tapering decision further down the road, with the next window of opportunity for announcing cuts in asset purchasing program now not likely until December at the earliest. Gold promptly rallied by 4.6% to $1,364/oz, the biggest upside move since March 2009.

Does this mean the end of the downtrend in Gold? In our view, the clear answer is no. The rally ran into significant volumes of producers selling before the end of the day, suggesting gold producers themselves have little in the way of positive price expectations, while US data continues to surprise.

In particular, US starts in August beat expectations, while consumer confidence continues to recover, along with auto sales. The tapering debate is back to a case of ‘When’, not ‘If’ in our view.

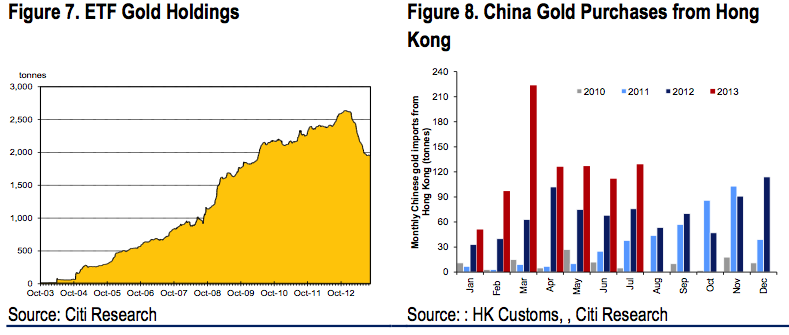

Physical ETFs have represented the most visible signal of negative investor sentiment towards the gold market, with the outflows becoming somewhat self-reinforcing, in that the outflows remove confidence in investing in an ETF in the first place, and in turn prompt further outflows. In the year-to-date, outflows reached 694 tonnes on by September 17th. However, the rate of outflow had slowed appreciably in August on Syria concerns and the timing of tapering debate. Given the FOMC decision to delay the introduction of tapering, we expect a reversal of the downtrend over the next month. However, any such reversal would in our view, be only temporary in nature, with a downtrend returning when the timing of tapering is clearer.

Where investors have fled, price sensitive retail buys have stepped up purchasing, most notably in China, where year-to July net imports from Hong Kong were up a remarkable 96% over the same period in 2012 at 688 tonnes. However, there are indications that the rate of purchasing is slowing as the premium of Shanghai gold prices over Comex has disappeared as metal from ETF outflows has flowed into China. While the upside price moves in gold on September 18th will no doubt spurETF uptake, the reverse is like to be true for retail buying. Indeed, we believe the Chinese market is now very well stocked with gold, suggesting import data from Hong Kong will slide over the remainder of the year.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.