Terry McCrann has written an important article today that shows just how far this country’s macro debate has moved:

BARACK Obama’s nomination of Janet Yellen to be the next and first woman head of the US Federal Reserve is of major significance for Australia.

Her certain confirmation to succeed Ben Bernanke at the end of January could well send the Aussie dollar back to parity and force our Reserve Bank to most unwillingly cut its official interest rate again.

That in turn could set in train forces that would result in quantitative restrictions on bank lending for residential property. More simply, rationing of home loans.

This all turns on the fabled Fed `taper’ – its proposed move to start winding back on its QE (quantitative easing). More simply, money printing.

…What this all though, all-but certainly guarantees, is that the Fed will decide not to start to taper, at its next meeting, at the end of this month.

I doubt we will go back to parity. The reason is that the Fed will continue to discuss tapering regardless of current outcomes. The exception is that the shutdown lingers to an extent that the Fed is forced to abandon taper for an official period and recommits to asset purchases, say, for another six months. If that happens it will be time to short the Aussie with both hands.

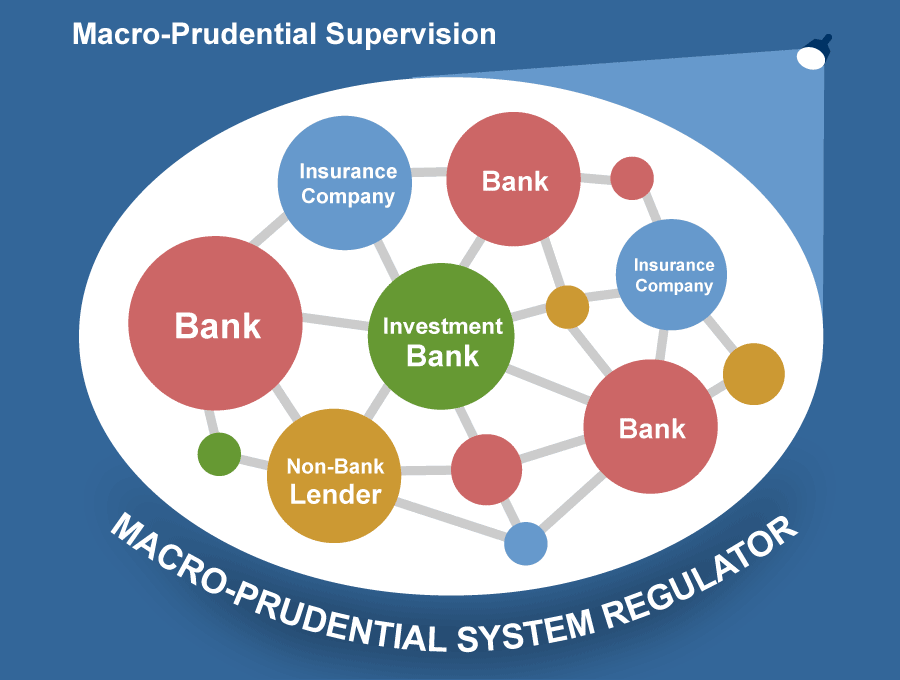

The McCrann argument, however, is just as pressing even without these scenarios. Rates are already well into the realm of financial repression. A little more isn’t going to matter much. And the dollar just as obviously overvalued. If our Terry reckons macroprudential is appropriate following another rate cut it is just as appropriate right now.