The European economy has recently taken an upturn and there is some evidence that the economic crisis that began post-GFC is coming to an end. The question is therefore whether the recent good news is part of a sustainable recovery or simply a seasonal or business cycle recovery that will soon fade.

To better understand whether Europe is now at a stage of recovery in a way that makes sense to the investor, it is important to understand the root cause of Europe’s recent economic issues.

Since the late 1990s European monetary policy has been driven largely by German domestic policy. German labour and trade policy, in fact their entire economic model, was shaped by the then recent absorption of East Germany which aimed to tackle the problem of high unemployment by producing structural trade surpluses. That is, via an exports-led growth model.

There was nothing wrong with this per se, but by doing so Germany was by definition creating trade deficits with its closest trading partners, many of whom happened to be under the single currency. As euro-wide monetary policy was also being set with the German economy at its core, an economic architecture was created in which debt fuelled consumption in southern Europe, and to some extent France, was left unchecked in the belief that the single currency, and single market, were strong enough economic structures to absorb the growing imbalances.

In hindsight this was, of course, a huge mistake. The Eurozone’s economic architecture was more “gold standard” than it was a US-style fiscal union and in the end the large structural deficits built up over 10 years caused balance of payments crisis across southern Europe. No one in the zone was immune, because by definition the recycling of trade surpluses through the large northern economies of Europe had left their banking systems highly exposed to the now defaulting south.

The fallout

Since the beginnings of the crisis, private sector wealth has shrunk considerably with house prices in countries like Spain having fallen non-stop for 5 years. The banking systems in Greece, Cyprus and Spain have all but collapsed. Italy’s economy continues to struggle with lethargic growth, falling industrial production and a rising wave of demographic issues ahead. Unemployment in many Eurozone countries is at levels that are unbelievable to much of the rest of the world. Spanish unemployment continues to rise and is now approaching 30%.

These statistics are shocking enough, but the most extraordinary outcome of this entire economic event was that it displayed that Europe lacked the mechanisms or organisations to deal with the fallout in a holistic way. Fiscal sovereignty still remained with individual nations, while monetary policy was set by a central bank, who at the time, was controlled by the highly conservative board with German policy still at its centre.

The crisis of the past few years grew worse as one Euro-group meeting after another failed. Under the leadership of Germany and its strong creditor allies, the EU and the IMF attempted to enforce a regime of fiscal austerity across southern Europe while failing to come to terms with the fact that, without fiscal support from creditor nations, debts owed were never going to be paid back. As austerity-based policies were implemented the GDP of targeted nations shrank dramatically and unemployment rose rapidly. The inevitable result was massive private sector retrenchment and a government sector that required continuing external support, as we still see in Ireland, Greece, Cyprus, Portugal and to some extent Spain, today.

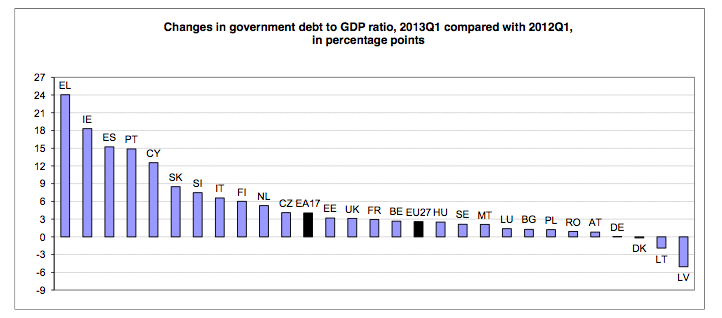

The end result of this policy was and is that public debt to GDP ratios continue to rise across Europe as can be seen by the latest Eurostat figures.

The big save

Eventually, as was inevitable, the European central bank released a number of measures in order to provide market and bank support as these bad public debt mounted. The ECB released the Long Term refinancing Operation (LTRO) program that provided large amounts of liquidity to the banking system in order to offset the fiscal tightening that was being attempted. Later the Outright Monetary Transactions (OMT) was announced as a secondary backstop when it appeared Spain was in serious trouble and Italy was looking down the barrel of contagion.

In short the response was hopelessly haphazard and uncoordinated. But many lessons were learnt along the way. The crisis and its associated fall-out do appear to have taught Europe’s financial leaders some valuable lessons and these potentially put Europe in a far better economic place going forward. Of note are:

- The European Central Bank has proven its willingness to support the monetary system as times of crisis even by the use of unconventional policy.

- Growth sapping fiscal austerity requirements of debtor countries have been slowly loosened in recent times allowing economic growth to begin to return to the region as witnessed by the latest PMI data.

- The European authorities realise the need for a central authority for the banking system to better manage any future crises.

- It is now understood that the European economic architecture is incomplete and there is a need for further fiscal integration.

- Although from a low base, and not widely recognised, German wages inflation has been steadily growing ahead of the EU average which will give German nationals increased spending power in the coming year, potentially allowing for a slow re-balancing of spending power across the region.

There are obvious caveats to these lessons. There is still the potential for default by debtor nations, and certainly Italy is a region of concern in that regard. There is also the question of how exactly any banking union will effect the day-to-day operations of individual banks. However, the uncertainty about the Eurozone’s future has been lifted in most part. All European crisis-hit countries are now running current account surpluses.

There is no doubt there will be future issues, certainly the growing debt to GDP and lack of growth in some countries is still unaddressed. The current account surplus model of growth that Germany has now engineered for the entire Eurozone (which means growth is export-led) virtually ensures slow growth because the global economy is simply not big enough to fill the demand gap for such a vast continental economy.

But the crisis measures taken will rebound growth modestly making all issue far easier to address hence forth.

Healthy banks

Of special note from an investment perspective are those banks who maintained a strong balance sheet during the crisis, or those who have been able to regain one via the leverage of the tax payer.

For example, in 2008 the Royal Bank of Scotland, RBS, along with Lloyds became mostly state owned via the massive UK bank rescue package. The bank issued a number of tranches of shares to the UK government and by the end of 2010 was 82% own by the state. These payments also included loans that were eventually paid back by May 2012. Over last 5 years the bank has divested some of its branch network, sold off certain parts of the business, trimmed its workforce by over 30,000 and was able to write-down huge losses on ABN-AMBRO all thanks to the good will of UK citizens. There are still outstanding issues with the bank, and there is talk that we could see a share split in a “good bank/bad bank” arrangement in the near future. But with the economy looking up and the bank now well placed, with a far cleaner balance sheet, there is good potential upside.

The RBS story is not unique, all across Europe the banking system has received state support with the tax payer burdened with the failings of the banking system during the economic crisis. Lloyds in the UK, Intesa in Italy, Societe Generale SA in France to name a few all received government assistance in some form or another, but have used the crisis to restructure their balance-sheets and are now seeing a return to, or increases in profit. You may not agree with what has occurred to get them here, but certain banks across Europe look to be in a strong position to leverage any major improvement in the broader economy.

Conclusion

Most recently there have been some good signs. Sovereign lending rates have continued to fall and the associated cost of lending in the private sector has begun to fall with them. We are yet to see growth in private sector lending but, the services and manufacturing Purchasing Managers Indexes have significantly improve across the zone suggesting economic activity is on the rise again. The results of the German election also showed that anti-euro sentiment in the country is waning, suggesting on-going domestic political support for both further fiscal integration and economic support for debtor nations, and in recent days we have seen some progress with the broader architecture including the banking union.

If these trends continue then we are likely to see some upside surprises from Europe in 2014 and the predicted 1.6% growth will actually materialise.

For the investors the lessons of Europe at this point are threefold. Long term the zone is likely to struggle with further crises as sovereign defaults return. In the short and medium term, however, so long as fiscal deficits are allowed to grow and Germany entertains some stronger consumption growth the tail risks associated with a European breakup or a bank freeze have been significantly mitigated and modest growth is in prospect.