The Reserve Bank prudently maintained its easing bias in the October Board minutes. The most important aspect of the minutes was the decision by the Board to retain the following sentence: “Members agreed that the Bank should again neither close off the possibility of reducing rates further nor signal an imminent intention to reduce them”. This statement had been used in the August and September minutes but there was genuine market speculation that it would be dropped from the October minutes.

It has been our view that the statement would be retained particularly as a signal to currency markets that Australian interest rates can still come down. Of course the other significance of retaining this sentence is that a rate cut is extremely unlikely at the November Board meeting.

That seems to be despite the imminent print for the September quarter Consumer Price Index.

We expect that the Consumer Price Index print will be consistent with the Bank’s forecast of 2.25% for underlying inflation for 2013. Note that print will be in the bottom half of the 2–3% target range.

We are forecasting 0.6% for the September quarter print for underlying inflation which will see annual underlying inflation drop to 2.2% from 2.4%. A follow up print of 0.6% for underlying inflation in the December quarter would see the annual print remain at 2.2%. That information will be available to the Bank from late January and provide important input to the February Board meeting.

The second important insight from the minutes was around the exchange rate. Clearly the Bank has found the appreciation of the currency since the September Board meeting unhelpful. Recall that the September minutes noted: “some further decline in the exchange rate would be helpful …”

Note that since the September Board meeting the AUD has risen from USD 0.90 to over USD 0.96.

The most important change since the September Board meeting has been the surprise decision by the FOMC to not taper the quantitative easing program as had been the almost unanimous expectation of the market.

Westpac spent July/August/September warning customers that ‘tapering’ was likely to run into a very high hurdle – the inconsistency between a tapering decision, which the Chairman linked to the economy evolving along expectations, and the clear need to revise down growth forecasts for 2013 and most likely 2014.

The tapering debate has now moved on significantly. Consider the following events :

1. The nomination of Vice Chair Yellen to replace Chairman Bernanke implies an even higher hurdle for tapering given her clear confidence in the success of QE and her doubts around the strength of the US labour market.

2. The government closure and the debt ceiling debate are likely to unhinge US growth in the December quarter. We estimate that the spending impact of the government shutdown is likely to impact growth by 0.5ppts (annualised) in the December quarter taking growth in the quarter to around 1.0% . The additional impact on consumer and business confidence with the associated drag on spending and employment is likely to be even more pervasive. Consequently the Fed is almost certain to have to further lower its growth forecasts for 2013 and 2014. The 2013 forecast is likely to drop from 2.1% to 1.7% – hardly a foundation for beginning the taper.

3. The FOMC meeting in January 28/29 will be held in the middle of the next debt ceiling debate. The government will be funded until January 15 and the debt ceiling will be raised until February 7.

4. Businesses are likely to hold back on employing and investing until a lasting solution is agreed. That paints a fairly dismal picture for growth momentum through to January. The flow of data, particularly for the labour market and spending, is likely to take a step back.

5. Indeed, FOMC officials may seek to lift QE rather than taper. The new Chair is unlikely to oppose them.

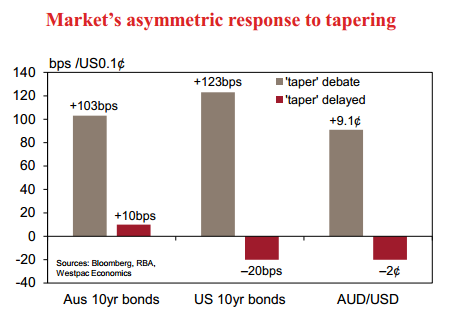

6. Some reasonable people might question the logic of the Republicans causing such chaos in an election year. However nearly 85% of Republican congressmen, all of whom face re-election, have majorities of more than 10% due to the long term gerrymander. Some Republicans fear a primary challenge from within the party Now consider where markets have moved since tapering rumours first emerged in April 2013. Long term US treasuries jumped in yield by 123bps to the day before the ‘no taper’ announcement. Ten year Australian bonds jumped by 100bps and the Australian dollar fell by US 9¢.

Since the non taper decision US bond rates have come back by only around 22bps and Australian bond rates have risen by 10bps. The Australian dollar has increased by only US 2¢.

It is clear that market responses to the taper prospects have been hugely asymmetrical (see chart). It is reasonable to assume that as markets focus on the diminishing likelihood of an imminent taper and a potential lift in QE, prices will adjust further – bond rates will fall and the Australian dollar will be boosted.

Those developments are likely to see a very different market attitude to the likely policy direction of the Reserve Bank. At present markets are giving less than a 30% chance of another rate cut from the RBA with rates confidently priced to be rising from September next year. We expect that to change quite significantly over the course of the rest of this year.

I cannot say I disagree though I do not think the RBA will cut further unless Sydney property calms down.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.