One of the AFR‘s better commentators, David Bassasnese, chimes in today with a forecast for more rate cuts:

…My base case remains that the next move in official interest rates remains down, and most likely in February next year. After all, the RBA reaffirmed in the latest minutes that – based on current evidence – economic growth likely remained below trend last quarter, and is still expected to remain “below trend over the next year or so.”

February is too early. We’re going to go through a little inventory cycle here and a decent Christmas bump as well so March or April is a better bet. But that is held hostage by one factor:

Given Australia’s now highly leveraged housing sector, unnecessarily aggravating household balance sheets in this way is best avoided if at all possible.

The RBA is also watching the lift in housing indicators carefully, though sort to play down fears of a house price bubble by noting it the minutes that “the value of the dwelling stock relative to household income remained below the levels that had prevailed for most of the past decade.”

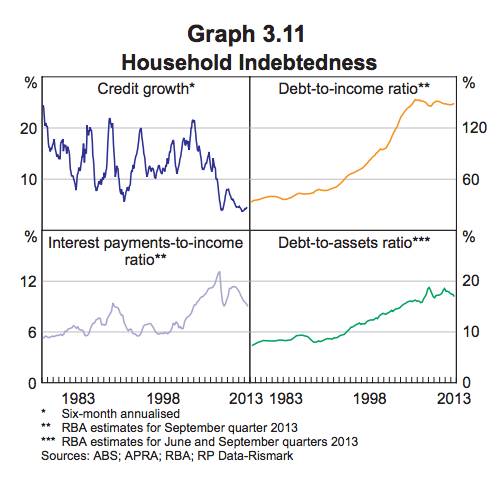

If Sydney property continues at its current pace there’ll be no more rate cuts. The ceiling on the ratios that Bassanese and the RBA refer to are not far away. The deleveraging is, in fact, barely perceptible:

The RBA will not be able to let it run far without income growth. They need macroprudential before they can cut again.