The US fiscal debacle is one of the few recent crises to not have caused Australian bank bond rates to spike. Throughout the past two weeks, bank CDS prices hovered around 107bps, neither up nor down on the previous period.

However, there is area where the banks’ offshore borrowing are about to become more expensive and that’s in the derivative charges that make the borrowing possible. From Jonathan Shapiro at the AFR:

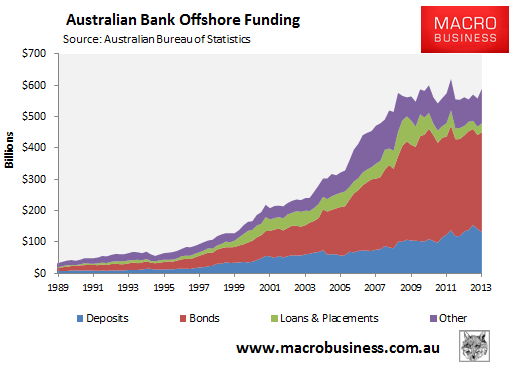

The large offshore borrowing needs of Australia’s banks mean they are heavy users of over-the-counter (OTC) derivatives to hedge their currency exposures. The instruments the banks use to hedge their $100 billion of outstanding offshore debt – known as cross-currency swaps – will attract high margins under new global standards.

The offshore debt reliant on swaps is far larger, somewhere between $350 and $400 billion:

Anyway, it’s the bank’s mastery of these swaps in the late nineties that ushered in the great Australian credit expansion (and housing bubble). The swaps protect the banks against a currency devaluation scenario so they don’t end up in a Latin American style debt crisis and can thus borrow to their heart’s content. Or could before the GFC! It is the use of these instruments that inclined me in my book the Great Crash of 2008 (written with Ross Garnaut) to see the banks as not so separate to “shadow banking” activities as many suggest.

Still, they are essential if the borrowing is to take place. I question whether they should remain OTC (that is, over the counter, or not on an exchange) and so do global regulators, who are driving up capital charges on these kinds of opaque instruments to build some redundancy into global markets.

The banks have applied for exemptions from the new rules and of course Australian regulators have backed them, but hopefully both will be ignored and the charges be forthcoming. It doesn’t really matter. You would expect those not using safer instrument to have to pay more for their debt anyway.

Another wee tightening of the growth straight jacket.