Deutsche has interesting note today examining why the Australian to US bond yield has blown out:

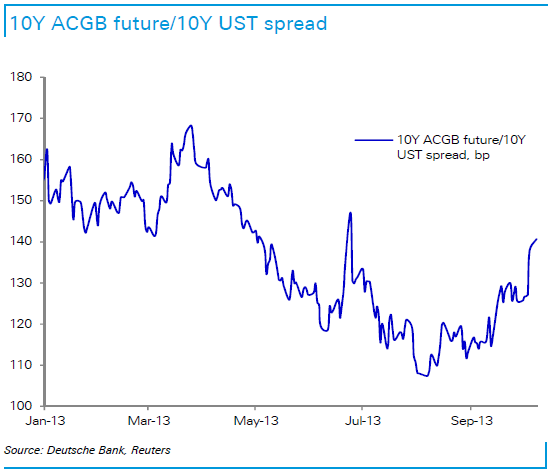

The 10Y ACGB/UST spread has widened sharply since the start of October to more than 140bp. Given the debt ceiling impasse in the US this seems counterintuitive.

The widening also seems to be more than can be explained by any front-end underperformance. On previous occasions in 2013 when relative front-end pricing has been around its current level the 10Y ACGB/UST spread has been in a 120-130bp range.

But we need to be careful about our time frame for comparison. On a longer-term horizon the 10Y spread looks to be in line with relative front-end pricing and the recent jump can be seen as ‘correcting’ a period of undershooting in the spread.

But why the jump now, especially given the debt ceiling impasse in the US?

It seems to us that the market has concluded that a US default is extremely unlikely and that even if the debt ceiling is not lifted in time any default will be ‘technical’ in nature and short-lived. In which case, does it really matter from the perspective of a 10Y UST? This may or may not be the right conclusion to make, but we suspect the UST market will hold to something like this view until a default actually occurs.

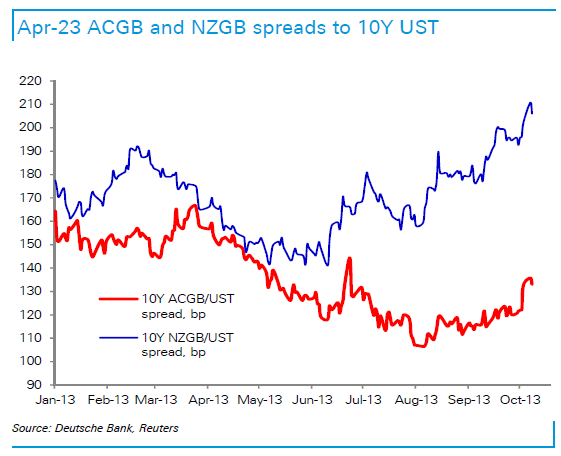

On the question of why now, we don’t have a convincing answer other than to refer to flows in what is a ‘nervous’ market given the uncertain outcome of the US debt ceiling impasse. The NZ market has been similarly affected, with the 10Y NZGB/UST spread also moving quite a bit wider in the past few days. Perhaps there has been some selling to take advantage of the recent rally in the currencies of both.

We don’t think the spread widening is evidence of a structural shift against AUD or NZD assets. It hasn’t gone far enough to support this conclusion and the currency strength referred to argues against it in any event.

Does the recent underperformance present a trading opportunity? We think the unknowns flowing from the debt ceiling impasse make such a trade difficult to recommend, particularly when we don’t think the entry point for the 10Y ACGB/UST spread is too wide relative to the fundamentals as represented by the front-end spread. In the event we do get a meaningful default in the US (as against a short-lived technical default) we think the 10Y spread will compress as the AUD front-end prices in a series of rate cuts by the RBA and investors exit UST holdings to at least some extent. But if the impasse is resolved in a credible manner and not just delayed for a month or two then the spread could widen if the AUD front-end decides the RBA has definitely finished easing and the next move is up.

There is also the possibility that the US 10 year is over-performing on safe haven flows owing the shutdown. Lot’s of uncertainties here.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.