J.P.Morgan is out with a note today summarising the surprises of earnings season and the news is interesting:

During reporting season we have been keeping track of company results using True Market Surprise (TMS) as well as watching out for Earnings Surprises, Dividend Surprises and revisions to both EPS and DPS based on Bloomberg Consensus to FY14.

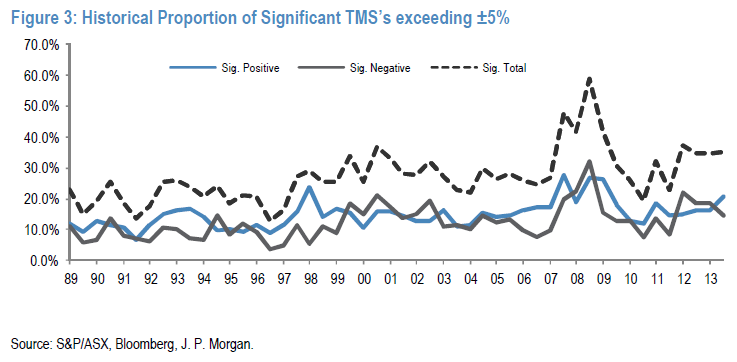

This seasons surprise levels for the ASX200 are ‘surprisingly’ positive, after a negative skew for the last three reporting periods! The ASX200 has seen 21% of reporting companies posting a positive surprise, and 14% recording negative surprises – a slightly positive skew on top of larger levels of total surprises (the typical ratio is 17% positive to 14% negative). The total proportion of surprises was 36%, which is high compared to the historical average of 31% as shown in Figure 3 below.

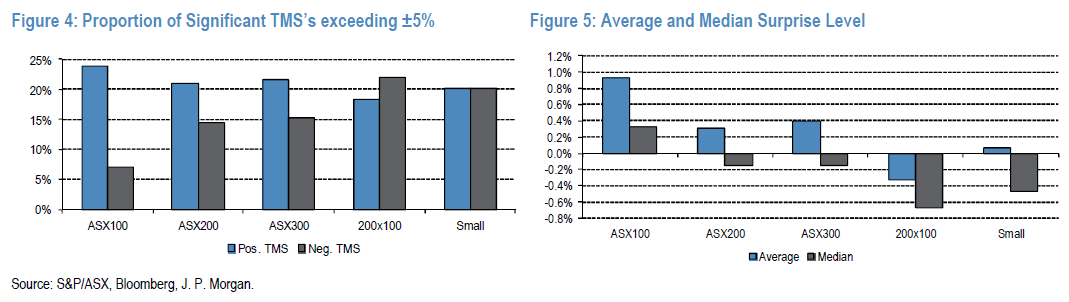

When we examine the proportion of significant surprises by market segment, we note that the skew of positive surprises was favoured by the large caps, with the proportion of negative surprises increasing as the market cap of the members decreased. Just 7% of the ASX100 had a negative surprise, while 22% of the second 100 had a poor reaction to their result (stocks 101-200) as shown in Figure 4.

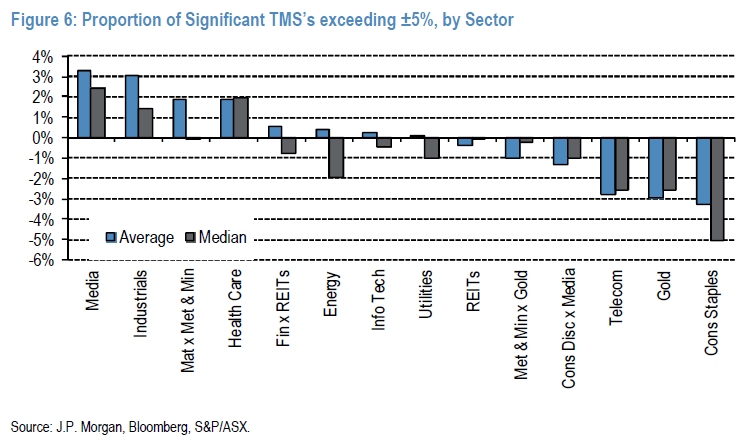

When we look at surprises by sector (Figure 6), there was a reasonable spread between the levels of average surprises amongst the GICS-14 sectors. On average, the Media, Industrials, Materials x Metal & Mining and Health Care received the most consistent positive surprises this season, about 2% to 3% each on average. The Telecom, Gold and Consumer Staples sectors performed the worst with an average surprise of approximately -3% each.

It’s interesting to note just how much better the large caps are faring. Typically in recovery cycle, which I suppose you could describe this as, large cap out-performance leads the small caps and as the cycle accelerates small caps gain the momentum once inflationary forces kick in.

This time around it’s been the same, in a distended and exaggerated way, with large caps operating in tasty oligopolies retaining far more pricing power than smaller players who compete for a living. One could argue that with authorities pursuing the great rebalancing theme via inflating asset prices that small caps are likely to out-perform in the year ahead. This could be encouraged by outflows from safe haven stocks into higher risk plays and by a little flourish of activity following the election.

Advertisement

But I still question the sustainability of this thesis. The year ahead will likely only see a little easing in household prudence and not much pricing power returning to domestically focused businesses. Large caps will be better positioned to extract their rents and continue cost cutting capex and opex which will continue to hit smaller businesses. As well, the falling dollar remains the key equities play and it’s better done via large caps.

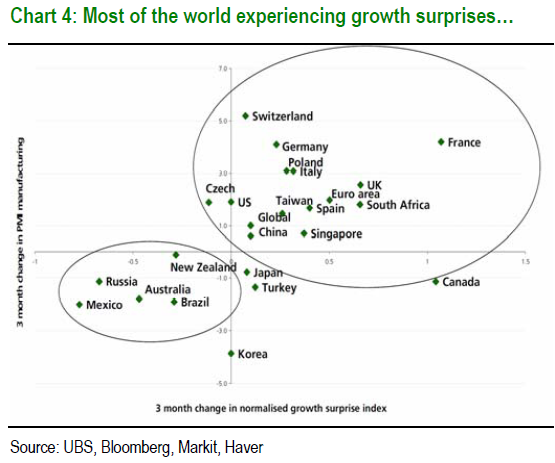

Basically, so long as the domestic economy under-performs, small capos will too. Let’s finish on a chart from UBS which shows just how badly Australia’s economy has surprised to the downside this year:

Advertisement

Third worst in the world, with more to come next year in my view.

My preference definitely remains with the larger dollar-exposed industrials or going elsewhere entirely.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.