From Goldman today comes a useful and sobering update on the progress in bridging the mining investment cliff:

Taking a step back from a handful of flagship road infrastructure projects, ABS time series data on engineering construction work done presents the challenge for Australian policy-makers from slightly different perspective. These data highlight that surging engineering construction activity in the mining sector has boosted nominal GDP by 1ppt in each of the past two years – rising to 4% of GDP, up from ~2% of GDP in 2010. Looking ahead, as mining construction activity retreats towards longer-run averages, the question is whether there is any capacity across the non-mining components of construction to provide a material offset. We make a few observations in this respect:

i) If, as a broader group, non-mining engineering construction did add 1ppt to GDP growth over each of the next two years, it would be an unprecedented development over recent decades.

ii) Given that there is some mining-related construction which has been spilling over into the roads/rail/ports categories, this might be expected to also ease back as direct construction at the mines themselves starts to wind-up. This would see downward pressure in these components – in synch with the fall in the “mining” component itself.

iii) Looking across the various non-mining components in the context of our own project listings, the outlook is fairly subdued. Specifically, we note:

a. Roads: As explained above the new road projects being prioritized by the Government might be expected to contribute less than $5bn to activity over the next two years (ie, only 0.3% of GDP).

b. Rail: There are no new major projects in pipeline likely to get go-ahead in near term. And on a generous assumption on existing projects like the North-West Link (and about 8 other projects) we are probably looking at $3.3bn spending pa (~0.2% of GDP).

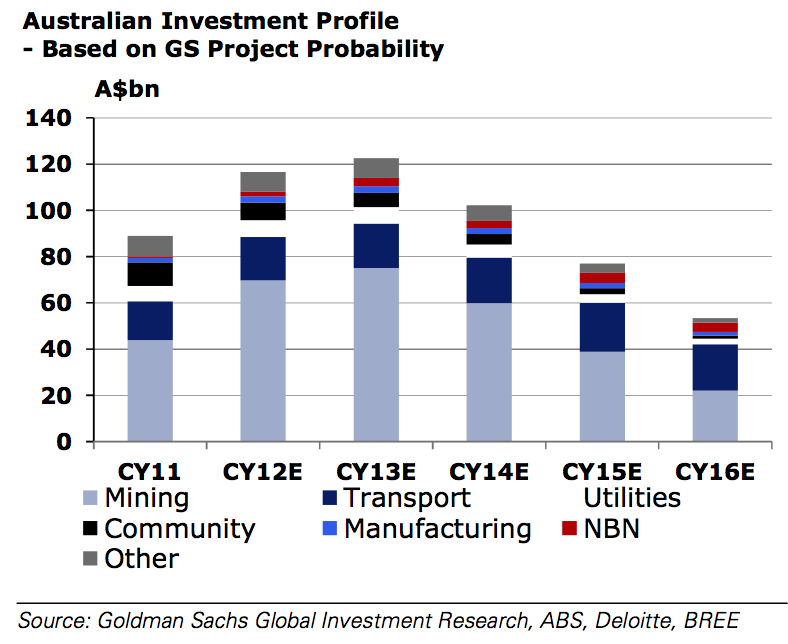

To put it in context, here is Goldman’s updated mining investment cliff with broader capex included and including Roy Hill:

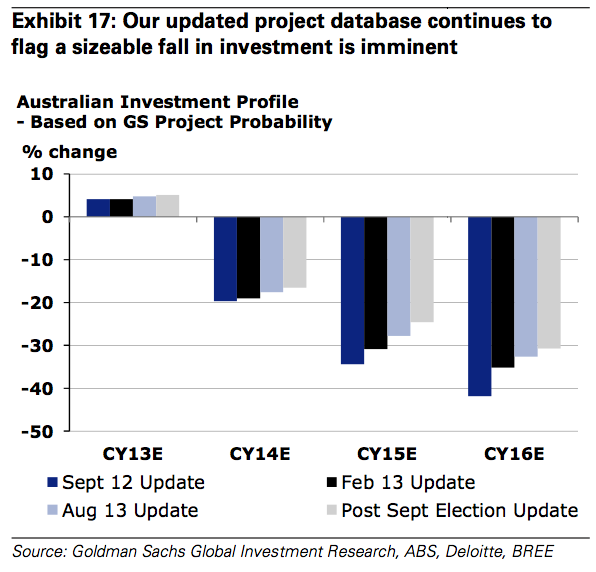

And in percentage terms:

These are enormous drags on growth and employment prospects. The exports will fill some some of the growth hole but the different composition of GDP is much less labour intensive. The risk to jobs is huge.