Overnight, FTAlphaville published another in a series looking at China and the middle income trap. Here is an excerpt:

Not many countries – namely Japan, South Korea, Taiwan and Singapore -were successful in the last 50 years in moving up from middle income group to advanced economies. Most of the other emerging countries either did not yet made it to the upper stage of development or have been trapped in a stage where economic growth is driven by the exploitation of cheap labour or natural resources, known as the “middle income trap”.

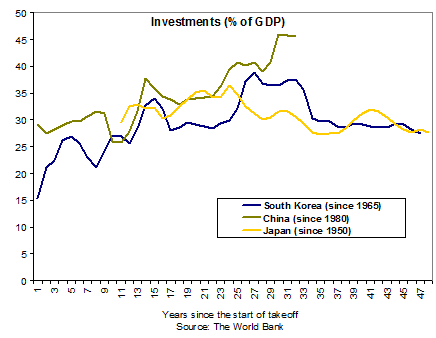

But those that did make it where characterised by long periods of high levels of investments after their economic takeoff, exactly like China is at the moment.

…the comparison shows China diverged from the other countries in the last few years, when its investments continued to grow and reached a level higher than the peak levels of any other country. It also suggests that China should be nearing the end of its period of unbalanced growth, as the other countries began rebalancing after three decades of high investments.

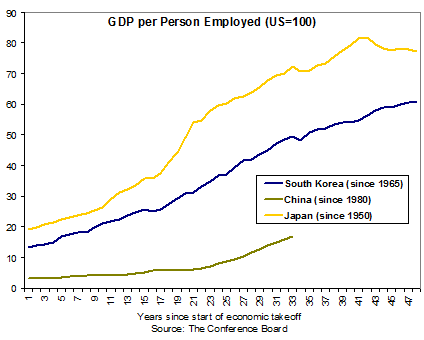

Chinese labour productivity started from much lower levels than in other developing Asian countries and economic growth was translated into significant labour productivity only in the last decade.

When South Korea started rebalancing in the 1990s, its level of labour productivity was nearly half of that of the US. Japan started rebalancing already in the 1970s when its labour productivity was nearly 60% of that of the US.

Despite the fast growth in the last decade, Chinese labour productivity is still less then a quarter of that of the US, similar to that of South Korea in the late 1970s and smaller than that of Singapore or Japan in the 1960s.

This is why, as I’ve argued all along, I remain a bull on the development of the Chinese economy. So much latent productivity potential can drive high rates of growth for a long time to come.

However, as the article concludes, productivity is already slowing “considerably” in China and the reason why is that it has over-invested in unproductive fixed assets. The answer to continued rapid growth in productivity, incomes and GDP is to shift gears into higher value-add production and more efficient allocation of capital.

Advertisement

Whether you subscribe to this model of the problems of Chinese development, or to the model made famous by Michael Pettis, that it is the debt resulting from over-investment that is the problem, the solutions are the same. As are the implications. Less commodity intensive growth.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.