Chinese macro data have been on a good run recently. Today’s release of August industrial production was particularly strong, beating consensus forecasts by a relatively wide margin, although not in a way that bodes especially well for long-term growth sustainability.

Here’s a summary of key data published today, courtesy of BAML:

From July to August, industrial production (IP) growth jumped from 9.7% yoy to 10.4% (vs 9.9% consensus), power production growth surged from 8.1% yoy to 13.4%, retail sales growth rose from 13.2% yoy to 13.4% (vs 13.3% consensus), and FAI ytd growth rose from 20.1% yoy to 20.3% (vs 20.2% consensus).

Advertisement

Trade data released yesterday also beat expectations, although imports missed them. Inflation data showed that consumer price data was a subdued 2.6 per cent, year-on-year, in August, down from 2.7 per cent in July. And producer price deflation slowed somewhat.

With all these promising signs for the near-term, sell-side analysts have been raising their Q3 GDP forecasts accordingly, and Goldman raised its full-year growth forecast from 7.4 per cent to 7.6 per cent. BAML is saying its own existing 7.6 per cent forecast faces upside risks. You get the picture.

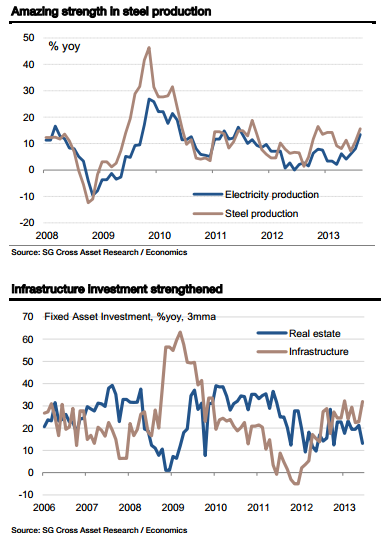

So, where did the growth come from? Here are some charts from Societe Generale’s Wei Yao:

Advertisement

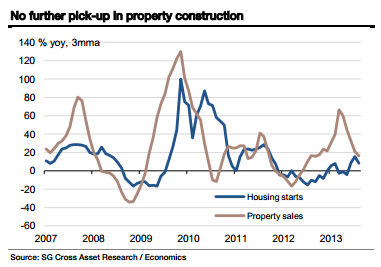

Interestingly, property construction weakened, although Yao says the sharp drop in August (year-on-year property starts fell 20 per cent, compared to a 45 per cent rise in July) is partly due to a base effect, and possibly a hot summer:

Advertisement

It does appear that the “mini stimulus” outlined in July might be having some effect. BAML’s Xiaojia Zhi and Ting Lu say that Premier Li Keqiang “will likely “taper” his pro-growth rhetoric started in late June” now that the 7.5 per cent growth target looks well within reach.

SocGen’s Yao is wary of how this number is being reached:

The significant acceleration in infrastructure investment was clearly the major push. Although this set of data puts clear upward pressure on our short-term forecast, the dominating role of infrastructure played in the sudden turn-around confirms our concern over the sustainability.

Advertisement

She is not the only one with such concerns. Mark Williams and Qinwei Wang of Capital Economics point out that the biggest rise in output came from state-owned firms —hardly the most competitive part of the economy. They write:

Bringing this together, the stronger data over the last couple of months have settled nerves about a possible hard landing, but there are strong echoes of the turnaround in 2009. The economy is once again being propelled, unsustainably, by state-led investment.

Williams and Wang believe this will be the big question:

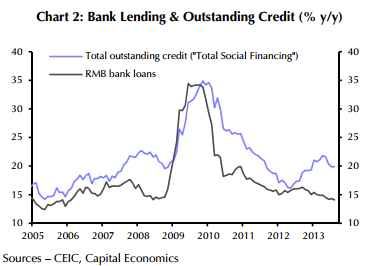

Looking ahead, the expansion of credit is probably the best guide to what happensnext. Today’s figures showed that bank lending growth has dropped to the slowestpace since 2006. On a broader measure though, growth of total outstanding creditactually picked up slightly last month, thanks to a rebound in designated (i.e.company-to-company) loans and issuance of bankers acceptance bills. (See Chart 2.)

They conclude (emphasis theirs):

Advertisement

More generally, overall credit is still growing at a 20% y/y rate which should sustainstrong investment spending for a while. The omens for the short term are good, but at the cost of making the economy’s structural problems worse.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.