The Kouk’s recent run of uber-optimism continues today with a call that interest rates are about to rise:

The economy is doing well and the financial system is in good shape. That said, the Reserve Bank knows that this owes a lot to very easy monetary policy settings that have been in place for the past year or so. While there is no overt comment on the monetary policy outlook in the FRS, a close reading of the whole document should lead one to an assessment that the bank has a scenario in mind where interest rates will need to rise. The only questions are when and by how much.

OK. Let’s clarify a few things. First, the economy is not doing well. Growth of 2.4% is materially below trend and unemployment is rising steadily with all surveys suggesting it will continue. House prices in Sydney are rising. Melbourne prices have risen as well but are well behind. Perth house prices appear to have topped out and declines are in prospect. The other capitals haven’t budged. The positive is that this has generated a modest rebound in housing construction. Consumption growth remains modest and combined government spending is flat. The second positive is strong exports.

In prospect for this weak economy is the greatest fall in business investment in 75 years and we’re still carrying a dollar that remains a crushing force upon the economy at 94 cents.

Internationally, Europe is barely out of recession, the US is slowing from only a moderate pace and has postponed its “taper” and China has a temporary rebound that is worsening its imbalances. Commodity prices are not going to rally further from here.

There is absolutely no way the RBA is going to hike interest rates in this environment, or in the next twelve months and probably for two years.

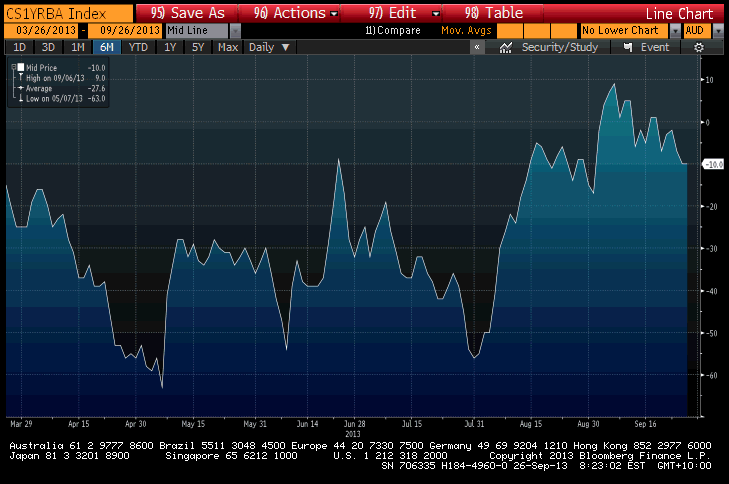

Interest rate markets have begun to realise it with 10bps of cuts now forecast over the next twelve months, falling back from a recent bullhawkian flirtation:

There is one caveat. The only scenario is which the RBA will raise rates is if the Sydney bubble keeps inflating and Melbourne joins in. But even then the RBA will first jawbone the market and look to APRA to contain the bubble with ‘behind the scenes’ macroprudential maneuvers first.

Deputy RBA Governor Phil Lowe is on record saying central banks should use the cash rate control property excesses and if forced to by maniac investors the RBA will do so. A combined jawboning and and sharp two hike campaign replicating 2003 would be the approach. The problem is that if Sydney property was stopped in tracks like 2003, there is no growth offset like there was then. No cheaper nation to follow Sydney’s debt-drive upwards and no mining boom to boost investment.

Take it from me, you do not want this scenario to play out. A housing bust as the mining boom unwinds is an 1890s scenario.

I still believe that the next move in rates will be lower but the timing has been compromised by the Sydney property blowoff. Having clearly signaled concern about the Sydney bubble yesterday, the RBA has made it a policy consideration and I can’t see how it can cut while that market takes leave of its senses. For now, rates are on hold.

But that means a higher dollar for longer, more hollowing out, and more economic drag next year, ensuring rates will fall again in this cycle.