Goldman Sachs has a neat note out today looking at mining costs and arguing that deflation is the new super cycle:

Potential for a protracted reversal of cost inflation

While currently there are signs of recovery in the GLI, we could still see global growth in demand for commodities undershoot capacity additions over the coming years, as EM growth softens in the face of a less resource intensive DM recovery. If this happens, commodities are likely to endure a protracted period of marginal cost pricing, depressing industry returns. This would force corporates to once again focus their efforts on productivity gains / cost reduction in a reversal of the dynamics of the past decade, where falling productivity and rising commodity currencies were major drivers of cost inflation in the sector approaching 2x.Lessons from the ‘80s and ‘90s – structural vs. cyclical costs

The recent period of cost inflation was preceded by a 15 year period of significant cost deflation into the early 00’s which we believe is instructive in analysis of the current outlook for the sector. At that time, industry response to the pricing pressure was to focus on productivity and asset utilization. This resulted in productivity gains driving much of the sector’s cost deflation in the ‘80’s and ‘90’s. Our analysis shows that costs were able to be reduced despite the industry suffering some significant structural pressures. We analyse this risk in a historical context and model the potential impact of a repeat scenario on returns.Structural vs. cyclical costs

Much has been made of the difficulty in taking out structural costs; however, we believe the perception of the structural costs in the industry is distorted. Contrary to popular belief, a large part of the cost increase in the industry during the last decade appears to be cyclical rather than secular and therefore could be removed if companies respond to falling returns. To assess this thesis, we constructed a ‘generic’ copper mine and analyzed the impact of the structural versus cyclical costs. Our analysis suggests structural pressures would have generated only a 37% increase in costs from 1987 to 2003 assuming no other changes in input costs for the mine. Comparison to the actual cost impact highlights the importance of currency, leading us to believe that a normalization of currencies (i.e. stronger USD and weaker commodity currencies) will have a big impact on the cost outlook moving forward.

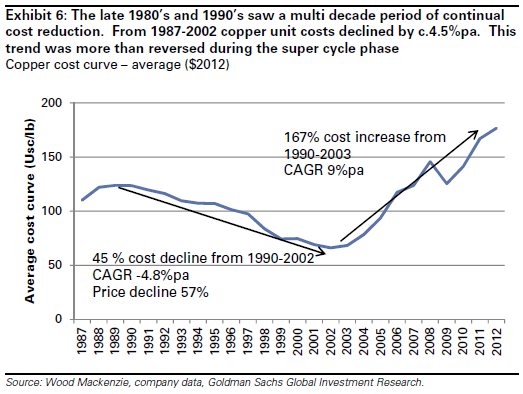

Here is the chart of the history of copper costs:

The same historical trend is apparent in the bulk commodities and gold.

With massive oversupply coming in all of the bulks and Chinese demand going through a step change, this Goldman thesis of a decade of “cost out” deflation is very compelling to me. In LNG, the new wave of Australian projects are all at the wrong end of the cost curve and as the US ramps up its exports a similar result is very plausible.

For investors, growth in mining profits is going to be much harder won in the decade ahead than that just passed.