Cross-posted from Kate Mackenzie at FTAlphaville.

The official China manufacturing PMIs for July are not helping any bearish narratives. Unless you are of the opinion that the official stats are often manipulated from one month to the next.

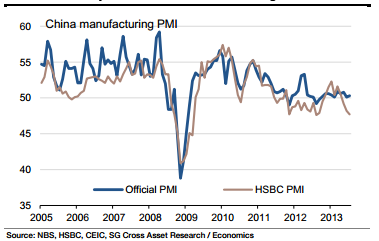

HSBC/Markit’s number, meanwhile, stayed firmly at 47.7, in contrast to the official PMI rising to 50.3 from 50.1 in June. Yep, we’re here, again, attempting to understand the mysteries of the China PMIs.

Let’s be clear, however, divergence is nothing new here:

… although this is the largest for 15 months.

Let’s look at the official one first. Wei Yao of SocGen points out that, unusually, all the sub-indices moved in a positive direction. The input price component rose sharply to 50.1 from 44.6. HSBC/Markit’s PMI found that input costs fell, but at the slowest rate for four months.

Employment, notably, remained below 50 despite improving for the first time in five months.

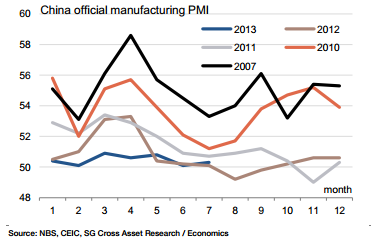

Some analysts are jumping to declare this a “first sign of stabilisation/recovery” — some analysts here being BAML’s Ting Lu and Xiaojia Zhi, who believe that Premier Li Keqiang has signalled that he won’t let growth go below 7.5 per cent this year and 7 per cent over the decade. As a result, measures constituting “small stimulus” package of both demand- and supply-side measures should see official PMIs go higher in coming months, they write.

But really, what should one make of the official PMIs these days, anyway? A couple of years ago, the official ones seemed to be favoured as a better measure because it was a bigger sample and supposedly a broader one too (Markit Economics rejects that criticism).

Then some ambivalence set in as the two diverged and the HSBC/Markit survey looked better. Early this year the sample for the official PMI sample had been greatly increased (from about 820 to 3,000), but the government agencies who compile it (the China Federation of Logistics & Purchasing and the National Bureau of Statistics) didn’t provide much more detail on this change, as far as we can tell.

Then for June, the industry sub-sections in the official PMIs were “suspended” because “time is limited — there are many industries, you know”. Yes, that’s exactly what CFLP vice-president Cai Jin reportedly actually said.

SocGen’s Wei Yao says the lack of seasonal adjustment in the official PMIs, historically a problem with this measure, seems to have diminished since the second half of last year:

She also writes that HSBC/Markit’s sample, which has a relatively bigger share of SMEs than the official survey, might have been hurting more from the June liquidity squeeze. BAML’s Lu and Zhi make a similar argument, and they think the state-owned enterprises that get bigger representation in the official survey have probably been more comforted by the recent stimulus-y declarations than smaller, private manufacturers. The BAML pair also argue that the declining role of exports in Chinese growth makes the HSBC sample — who are more export-oriented — less relevant.

Zhiwei Zhang from Nomura points out a possible flaw in that argument:

We believe this divergence reflects the high level of uncertainty over China’s growth outlook, although it is unclear why it emerged. The HSBC PMI tends to cover more exporters and smaller firms, but this difference in sample cannot explain it as both the HSBC and official PMI show domestic demand seeming to slow more than external demand and the small firm subcomponent in the official PMI showed an improvement to 49.4 from 48.9 in June.

More importantly, Zhang thinks the policy implications of a rise in the official PMI survey, despite the effects of the June liquidity tightening, are that more monetary easing this year is unlikely.