US bond yields spiked again last night, with the 30 year jumping 1% to 3.90 and 10 year jumping up 2% to 2.88%:

This is what I’ve been talking about for the past year or so about interest rate normalisation in the US being a problem. Analyst James Aitken puts it nicely:

“For the past five years, getting into credit and fixed income has been driving down a three-way highway. Getting out will be like driving down a goat track.”

Correct and now US housing faces the equivalent of six standard rate hikes in three months. It’s already rolling over.

But that’s not the immediate concern. That lies in the reversal of the flows from where global capital settled most happily in the post-GFC period, emerging markets. From the FT:

The 20 biggest emerging market currencies tumbled against the US dollar on Monday with India’s rupee particularly badly hit amid mounting market turmoil in the developing world.

The rupee slumped to a fresh all-time low against the backdrop of deepening concerns over the government’s economic management. The 2.4 per cent fall to a record 63.2 to the dollar took the currency’s slump against the US dollar this year to 12 per cent.

…Fears over the impact of the Fed’s plans to scale down its bond purchases have been compounded by slowing economic growth and deteriorating fiscal fundamentals in many countries. Investors are particularly concerned by states with current account deficits that have been plugged by inflows of more flighty investor capital, rather than stickier foreign direct investment.

“It’s the current account deficit countries that are in the most trouble,” said Angus Halkett, a bond fund manager at Stone Harbor Investment Partners. “The market is becoming a lot choosier where it puts its money, and some countries are going to find it tough.”

Indonesia provided evidence of that on Monday as its main equities index fell by 5.6 per cent after the country’s central bank reported on Friday that its current account deficit had widened sharply in the second quarter of this year.

New numbers on Monday also showed how the growth equation is changing for emerging economies with Thailand’s economy slipping into a technical recession thanks to weak exports and sluggish domestic demand.

But India remains the biggest concern for many investors with the pessimism there driven by questions about the government’s economic management following its introduction of a number of failed measures to support the currency, some of which appear to have exacerbated the country’s problems.

…The government last week issued capital controls on overseas investments by Indian companies and individuals to staunch currency outflows. But it needed to attract capital, Mr Aziz said, through measures including liberalising restrictive rules that prevent long-term foreign investors from buying Indian government and corporate bonds.

“They have only taken steps to stop money from going out. They have to worry about bringing money in,” he said.

J.P. Morgan has more on the implications for Asia:

As US 10Y yields climb (2.83%), we revisit our key theme since May: Asia has reached an inflection point on leverage & growth, and rising rates will push up the cost of capital in a region can scarcely afford it. While this applies to most of Asia, relative policy flexibility is driving near-term divergence in bank stocks.

- Countries are more vulnerable where current accounts have sharply narrowed, forcing policy to either slow import demand (via tighter credit) or attract inflows (via higher rates) to rebalance the trade account. In contrast, surplus countries have fewer constraints, but offer weaker LT-growth. This is the “pain trade”; and we don’t think it ends until we see credible solutions to BoP issues.

- In Indonesia, worse-than-expected inflation (+8.6%) and 2Q current account (4.4% of GDP) implies further tightening. After +75bps of rate hikes & new LTV measures, last week BI also reversed course on targeting higher LDRs. With system LDRs at 92% & deposit growth some 10% below that of loans, we see material downside risk on EPS as banks tighten growth or fight for deposits.

- India has also been forced to squeeze demand via tighter liquidity & excise duties, with the surge in WPI (+5.8%) a reminder of how INR weakness fuels inflation. Corporate loans are now growing +13% Y/Y, the weakest since 2009, and slower growth is broadening the impact of NPLs across PSUs & private banks, with retail lending the only area showing resilience for now (+17% Y/Y).

- China has flexibility on policy to draw a line under growth, with inflation still low (+2.7%). Before we sound outright bullish, consider banks “foot the bill” of stimulus, which consumes capital, as do rising NPLs. Capital is further hit by the shift from shadow banking & offshore credit to traditional lending seen in recent TSF data. We see cap raises as a growing risk for <10% Tier 1 banks (see right), hence have a pref for ICBC/CCB or CMB vs. other JSBs post-rights issuance.

- Taiwan is perhaps best insulated from external pressure, and we still think it a key beneficiary of rising rates, although a move in short-term rates is still far off. Strong 2Q results + a pick-up in consumer favors Chinatrust & E.SUN. In Korea, 2Q results were still weak, & we prefer the Regionals/Shinhan.

There are a few echoes here with the Asian financial crisis and there must be a tail risk here of something untoward happening – a la LTCM – as big leveraged positions could get caught on the wrong side of these moves.

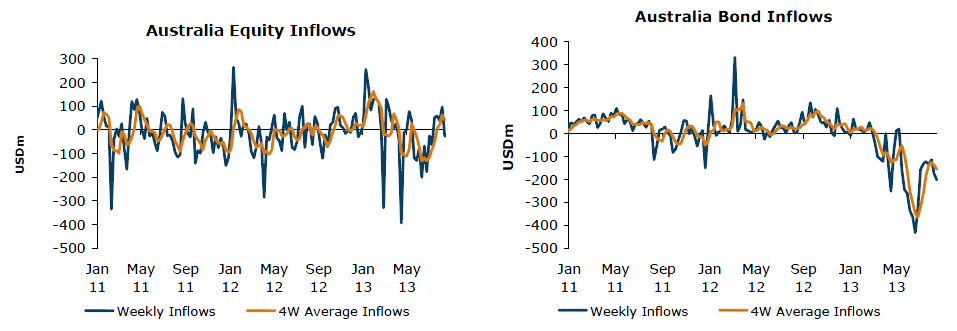

As I noted Friday, there’s a special place in all of this for Australia with local bonds being dumped like crazy:

This is not necessarily a problem, so long as it doesn’t get so out of hand and start to impact bank funding costs. CDS prices, which reflect long term bank bond rates, have risen from 70bps in April to 109bps yesterday but much of that happened in May and June and hasn’t worsened since then. In the meantime, at least the dollar is starting to get drawn into the downdraft, falling 1% last night.

So, where to now? It’s all about the Fed my friends. Its rather sensible experiment with jawboning markets in advance of any real tapering is causing some very serious yield spikes all over the emerging world, not to mention at home.

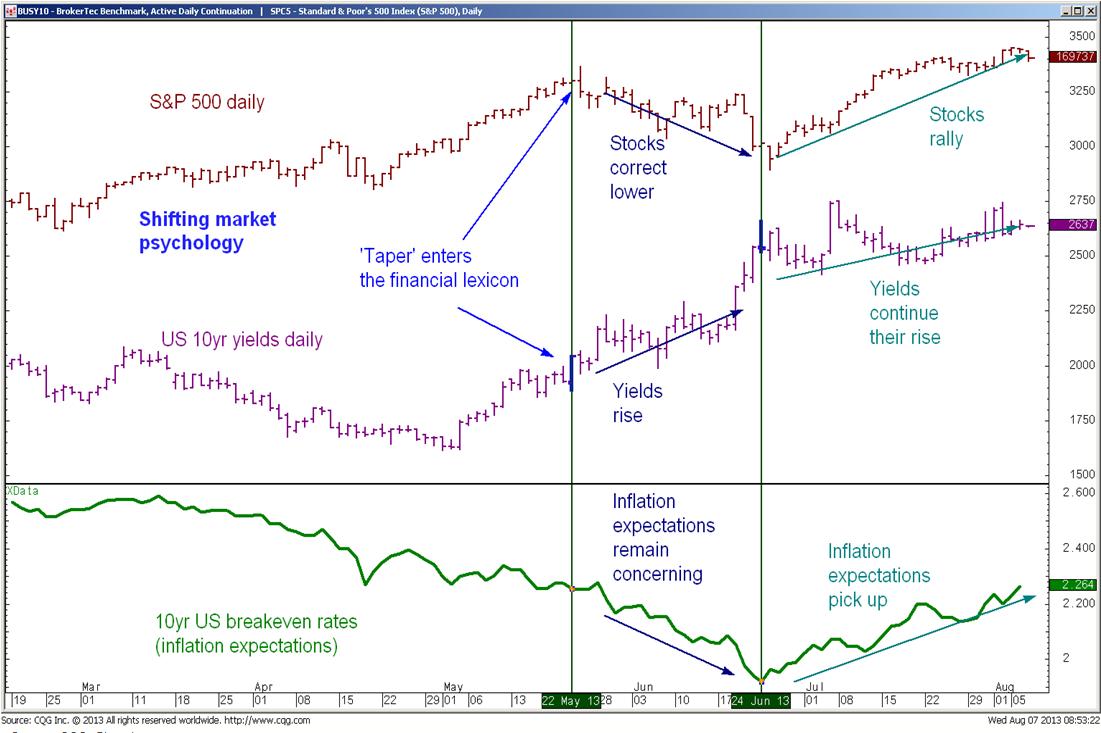

Black Swans aside, CQG had a hopeful chart earlier this week suggesting stocks could whether the shift:

But I don’t think so. These bond moves are far too far, too fast and so long as they continue, stocks are in trouble.

That shouldn’t worry the Fed, however. It explicitly said that this tightening is about preventing excess leverage in the cycle, which means capping asset markets. After it’s hawkish rhetoric it will have to deliver some tightening in the next six months, seems a shame to waste a good crisis after all, until it’s overtaken by fading growth.