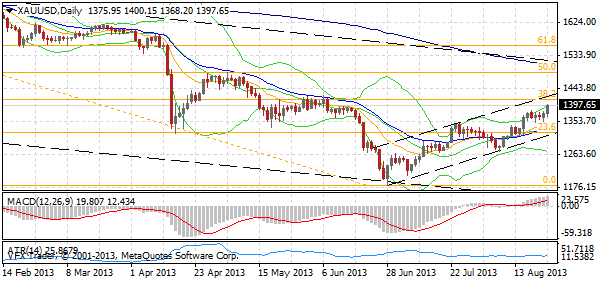

Gold surged on Friday night to $1396 oz. after the release of some very poor housing data from the US. New home sales were expected to fall in July but only 1.4% so the 13.4% drop was a huge miss and we saw the US dollar and other markets react instantly.

Gold is now just $17 away from the $1413 target I set a little while back:

On Friday the weak housing data knocked the US dollar for six against the euro (1.3380) which spiked but then drifted over over subsequent hours. Sterling (1.5573) did likewise but got hammered into the close and the yen (USDJPY, 98.67) gained as well before the US dollar strengthened into the end of the week. For the Aussie dollar it was a 40 point bounce into resistance at 0.9030/40 before it drifted off to close at 0.9025 where it is this morning.

It is going to be interesting this week for gold and FX. Over the past week we saw both euro and sterling reverse off some key levels as well and yen is very close to a topside break. Perhaps durable goods tonight are going to surprise to the topside.

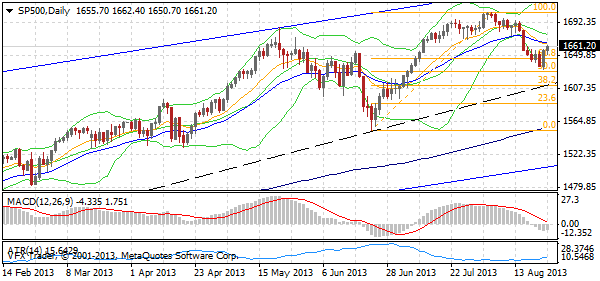

Recapping Friday trade and the weaker data helped both bonds and stocks rally in the US. 10’s closed at 2.81% while the Dow was up 0.32%, the Nasdaq up 0.53% while the S&P 500 rose back to 1664 up 7 points or 0.42%. In Europe the FTSE was 0.70% higher, the DAX rose 0.23%, CAC 0.24% while Milan and Madrid were up 0.19% and 0.66% respectively.

As noted above on commodity markets gold spiked as well on the broad US dollar weakness after the housing data closing at $1396 up 1.84%. Silver’s spectacular move continued up another 3% while oil also rose on the weaker USD up 1.32% to $106.32. The Ags were at it again with volatility the order of the day – corn rose 1.64%, wheat 0.63% and soybeans were 3.2% higher. I’m guessing margin calls have increased on these futures.

Markets are in a state of flux and it is clear that even though the stock market is still doing reasonably well bearishness has grown as seen in the AAII survey. It is kind of strange but the key to all of this is the taper and the bond markets reaction to same.

My view is that it is becoming even more difficult for stocks to push much through these recent heady levels but then again that seems to be conventional wisdom which is never a good feeling to be part of.

As you can see in the chart the 50% retracement of the recent rally pulled up the selling last week but a move back to this level and the 1610/20 seems on the cards if the S&P 500 can’t get through 1665/70 early in the week.

Data

On the data front there is some important things this week non more so than the Ifo data in Germany tomorrow night and US GDP data on Thursday. Today however sees the release of Trade data in New Zealand, Singaporean industrial production, a Bank Holiday in the UK and Durable Goods and Dallas Fed manufacturing in the US.