Credit Suisse today asks the question on every gold bug’s mind:

After printing the low of the year so far at the end of June ($1,180.50), gold has rallied 20% (although is still down -15% year to date). The turn higher was initially a function of another surge in physical buying after the slump through the second half of June, plus a degree of profit-taking by speculative shorts, and was aided by a reversal in US real yields as Treasuries regained some ground after a marked sell-off.

Since early August the rally in gold has gained renewed momentum from a combination of three primary factors, in our view:

1. Instability in emerging markets – which was evident first in rates, and more recently and starkly in another lurch lower in the currencies of three key gold buying countries – India, Turkey, and Thailand.

2. Worsening geopolitical unrest in the Middle East (Egypt, Syria) and the potential knock-on effects on Iran, Saudi Arabia, and Turkey, with a resulting rise in the price of Brent crude.

3. Growing uncertainty (or less conviction) about Fed tapering beginning in September, particularly since the poor New Home Sales and Durable Goods orders of last week, plus increased attention to the US debt ceiling (due to be hit again in October).

That has resulted in:

Strong physical demand across the Middle East, the Indian sub-continent, and South East Asia. Although the Indian government and the Reserve Bank of India’s attempts to talk down gold buying and a further increase in import duties to 10% have had a dampening effect on imports through official channels, we think the high local premiums (still reported to be in the $25 to $30 per oz range) and ongoing slump in the rupee are likely to be incentivizing unofficial import trade.

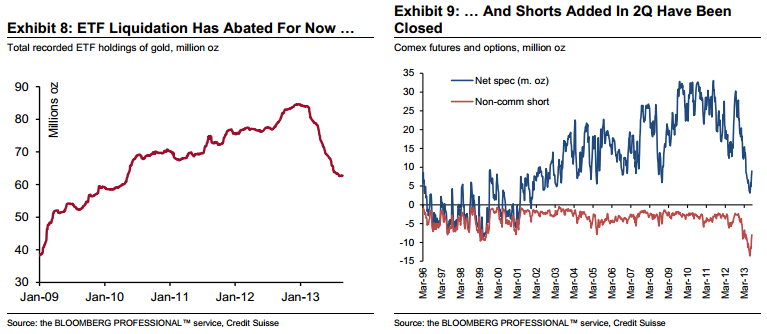

A pause in gold ETF liquidation. A total of almost 22 million oz (684 tonnes) of gold was liquidated from physically backed gold ETFs between January and early August. However, the pace of liquidation started to slow in early July and the selling had halted (at least temporarily) by the second week of this month.

Short-covering on Comex to the tune of ~6 million oz since early July.

The question now is, can the rally be sustained? In our view, the emerging market sell-off is now largely “in” the gold price, as is a re-adjustment of expectations regarding tapering (note that our economists still expect the Fed to reduce the pace of QE by $20bn/month at its September meeting; see US Money Matters: KC Fed Symposium). Further sizeable short covering in gold is unlikely, in our view, unless the price breaks above the early May high of $1,488 and then the $1,500 level. In our assessment that would require further substantial deterioration in the security situation in the Middle East.

I agree. So long as the Fed is considering tapering then gold is a “no go” zone fro anything other than short term speculation, unless you think the yield spike to date will cause the US economy to grind to halt reinvigorating expectations for QEternity.

Advertisement

Of course in Australian dollars it might be different but there other ways of playing that without the risk of gold price falling alongside dollar.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.