Tomorrow’s RBA meeting is a no-brainer hold. Following Thursday’s Pascometer alert that the low is in, the Australian dollar got smashed to a new low on Friday evening and looks to be headed under 91 cents in short order. That will be enough to keep the RBA on the sidelines tomorrow. Not that it should be. Rather, it should be preparing macroprudential tools and cutting again to build on the dollar’s weakness.

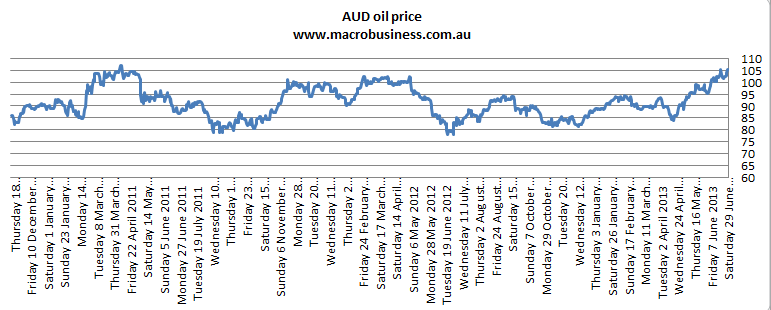

Back to today, the most interesting question is what the RBA is going to do about incipient tradable inflation resulting from the falling dollar. While I suspect the coming spike will be less severe than some fear owing to capacity slack, falling income growth and margin compression for importers, it’s still a possible shock coming down the pipe. Look at oil in Australian dollars for instance, breaking towards its highest price in three years:

Yet the RBA has so far said nothing.

Recently, Treasury Secretary Martin Parkinson declared:

”I wouldn’t wish to speak on the governor’s behalf and as a board member it is always a slightly difficult situation,” he said.

”But they could basically keep interest rates at a particular point, or they could lower them further, and just accept that inflation went out of the band for a period. Then, you know, they could try and stop the second-round effects.”

He was backed by his deputy, David Gruen, who said the Reserve Bank’s ”flexible” target meant it could allow inflation to climb above the top of the 2 to 3 per cent target band so long as it did not spark a wage-price spiral. Inflation is now 2.5 per cent. A sudden increase in rates to contain inflation as the dollar fell could harm the economy and prevent the dollar from falling further.

My view is that the RBA is not so reckless that it will hike rates as we go over the mining investment cliff. It will look through any tradables inflation spike. But should it let us know in advance? There are arguments for and against.

To tell the people now that future inflation will be ignored risks decoupling the inflation expectations that Glenn Stevens has worked so hard to bring to heal following the easy money reign of Ian Macfarlane:

Against that, however, is the risk that the opposite happens. If punters think rising prices are going to prevent or reverse interest rate cuts then they will begin to shift their behaviour, saving more and slowing the economy further.

The RBA is in a political bind here as well. If it takes the path of looking though tradable inflation, there is bugger all it can do to prevent a second round wage inflation spike from happening. That will be prevented only by the economy itself or by government intervention in microeconmics via industrial relations policy. So the RBA will be tempted to wait and see what the two political parties will do about it. Given both have so far fought the election on fantasy grounds, they may be waiting a long time. Hopefully Rudd will inject it into the debate.

Tomorrow’s monetary policy meeting is not the time to begin this discussion. But it must be addressed soon or monetary policy decisions may begin to lose their logic. The RBA would also be doing the nation a favour by forcing the issue into the election debate.