The Shadow RBA is out with it’s monthly “hold” call. I prodded this body last month to aim for something a little more innovative, alas, no such luck. If anything the body has become more conservative, failing to discuss the issue of potential tradable inflation, alternative monetary tools, the mining investment cliff, China’s prospects or the general environment of currency wars.

I really don’t get it. If the Shadow RBA is simply going to follow the same guidelines as the RBA, it has no purpose. If it were exploring the issues the RBA is unable or unwilling to canvass in public it would be making a very valuable contribution.

More of the Same

Uncertainty about the global economy is rising and bond, equity and currency markets are reacting violently. China’s authorities are attempting to rebalance their economy by reining in credit and imposing tougher financial rules. This has led to a temporary spike in the interbank rate as financial institutions are scrambling for liquidity. On Monday, 24 June 2013, the Shanghai stock index suffered its worst one-day loss in nearly four years. The big question is whether China’s authorities will be able to engineer a soft landing or whether Chinese markets, and the economy, will experience further severe disruptions.

Bond markets were spooked by the Federal Reserve hinting at its intention to taper off QE3 going into 2014. While fundamentally good news, as it implies that the Fed sees the US economy on the road to recovery, the market’s reaction reveals how addicted investors have become to cheap credit.

In Europe there has been no progress towards a cooperative resolution of the Euro crisis. Cross-country imbalances persist, banks are still undercapitalised, and the fiscal outlook is dire as many Euro countries are flirting with recession.

In Australia, first quarter GDP data points to a slight reduction in the economy’s growth rate, largely due to a fall in investment, both public and private. The continued depreciation of the Aussie dollar should help to relieve the pressure on the exporting sector but the dollar may need to fall further to counter any significant slowdown in the rest of the world.

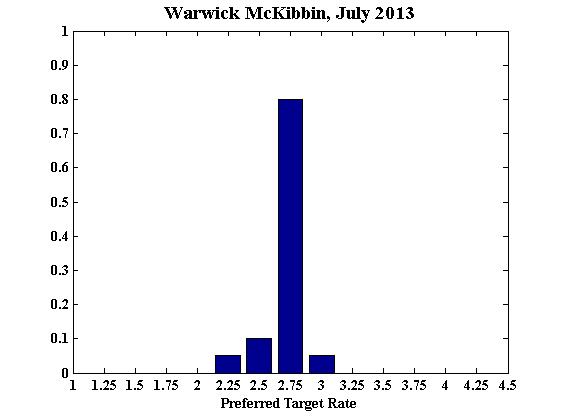

The consensus of the nine members for keeping the cash rate unchanged at 2.75 percent has strengthened in the last month, with members continuing to see more risks to inflation on the upside than the downside.

At the 6-month and 12-month horizon, the distributions for preferred interest rate settings remain virtually unchanged: the probability that rates will need to rise in the next six months still equals approx. 30 percent and that rates will need to fall approx. 40 percent. A year out, the shadow board members attach about 45 percent probability that the cash rate will need to rise and 37 percent probability that the cash rate will need to fall.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.