As the US dollar hits a four year high this afternoon, find below a useful note from ANZ on the Return of the King!

The market is pushing aside any contrarian USD arguments and focussing on the relativity of central bank forward guidance as the key dynamic in currency markets at present. The dollar has appreciated as a result and the prevailing expectation is that it will continue to do so. Price action clearly implies that a strong balance of opinion believes the nascent stage of forward guidance by the ECB and BoE means that the euro and GBP should weaken. The market will be very sensitive to data releases in how it trades.

US Non-farm payrolls in June were stronger than expected at +195k. Owing to upward revisions to prior months, the 3m average is now 196k and the 6 month average is 201k. This re-affirms the recovery in the US and the improvement that is taking place in the labour market. Tapering expectations are that the Fed will start reducing its asset purchases in September and end QE3 in the middle of next year. The dollar rallied in response to the data and bond yields rose sharply. The next FOMC meeting is on July 30-31 and the markets will be keenly awaiting any steer from Bernanke then. But that should only likely confirm what the market already knows: the bias in US monetary policy settings is changing.

Since the mid-June FOMC meeting and owing to the relative shifts in forward guidance by major central banks since then, there is a growing belief that the dollar will rally further. Current and expected favourable relative growth and interest rate differentials in the US are underpinning this view and the June labour market data added weight to that. The US bond market has been under severe downward pressure, which has dragged yields higher globally. From a relative business cycle perspective, the strength in the dollar seems justified based on US developments.

Both the ECB and BoE have clearly signalled that this is not appropriate for their economies to experience higher rates at this stage in the business cycle. The fear that the rise in bond yields and the general increase in expectations for the term structure of interest rates could weigh on their fledgling economic recoveries. Respectively, therefore, they have either introduced or signalled an introduction of forward guidance. This is clearly aimed at distancing their policy settings from anticipated developments in US monetary policy by introducing a neutral to downside bias for interest rates and extending the horizon over which rates can be expected to stay unconventionally low. The ECB will be reasonably happy with how Euribor futures held up in the aftermath of the NFP data as expectations of higher US rates rose.

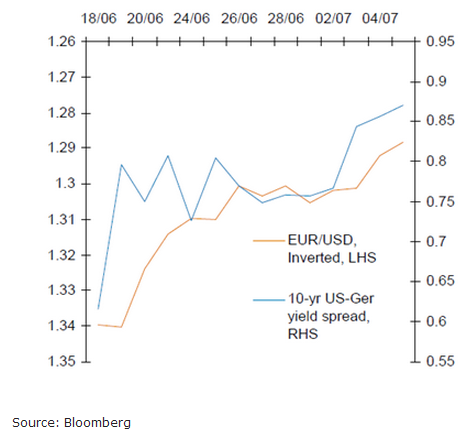

Over the past 10 months, EUR/USD has spent most of its time in a 1.28-1.32 trading range. Deviations outside of this range have proved short lived and either buying or selling opportunities as the cross has proved again to be mean reverting. Over the past three months sterling has been in a corrective phase against the US dollar. The key question now is: are we entering a period of different dynamics that drive the investment and currency process? As the US economy recovers, the cyclical bias favours equities over bonds. US labour market participation is at record lows, so corporate profits as a percentage of GDP are expected to remain high and rise as the economy picks up. The US has the deepest and most liquid equity markets in the world which, supported by its yield advantage, favour the USD and that’s where capital should flow. Is it that simple?

Cable has given the clearest signals of the shift in relative dynamics within the majors. Yesterday, the BoE broke with tradition in issuing a statement to accompany the MPC announcement. The BoE said it maintained its current level of asset purchases and kept interest rates unchanged at 0.5%. It said that the CPI was set to rise in the near term and that inflation should fall back to target further out. It said that recent data releases were broadly in line with expected developments in GDP but that the upward movement in market rates would weigh on this outlook. The implied rise in the expected future path of the bank rate was not warranted by recent domestic developments. The analysis of the case for forward guidance will have an important bearing on the August policy decision.

Sterling fell sharply against the dollar as a result. Implicit in the BoE’s statement is the adoption of flexible inflation targeting and a more growth friendly BoE. Forward guidance will probably be adopted. How this forward guidance will be framed will be of interest to the market. Will it be a simple statement that rates won’t be going up for a period of time or will monetary policy settings be linked to developments in the real economy? Will more QE be forthcoming?

The reality is we don’t know what the framework will be. But we do know that as the BoE’s communications policy is developed, the preference is for loose monetary conditions to continue for some time. This “relativity” on where central banks are on the forward-guidance or communications curve (which indicates their monetary policy preferences) is key. The market is clearly translating a preference for a continuation of loose monetary policy into the requirement for a weaker currency. After all, if interest rates have little or no scope to fall and the UK banking system is dysfunctional because of the need for balance sheet repair, the currency takes the strain. Q.E.D.

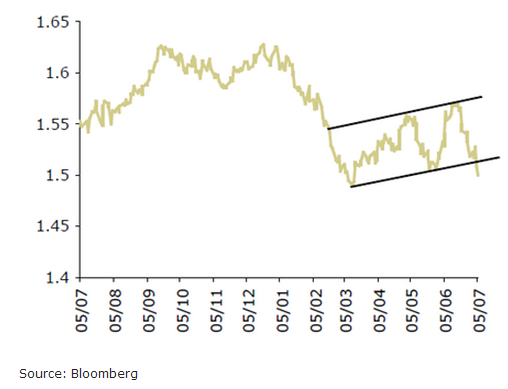

In response to the BoE’s announcement, cable broke down from the corrective flag pattern it has been trading in in recent months. Stealing from our technical analyst Tim Riddell, this could provide measured targets based on whether you think the correction will be the depth of the flag (roughly 6 big figures) or you measure the projected move (which could be equal to the pole size of 14 big figures) from the top or bottom of the flag. In round terms, this could provide targeted moves towards 1.45, 1,42 or 1.37 respectively. Stops above 1.5200.

Similarly in EUR/USD, the ECB is new to the forward-guidance/

“The Governing Council expects key interest rates to remain at present or lower levels for an extended period of time.” Draghi stated that 50 bps is not the lower bound in interest rates and that key interest rates include the deposit rate. In explaining the change in communications policy and forward guidance, Draghi went on to say that monetary conditions had tightened and that while the rise in PMIs was encouraging, they still signalled a contraction in activity. “That’s why the ECB moved to forward guidance.” This maintains and emphasises the ECB’s easing bias.

Surely, therefore the same logic must apply to EUR/USD as to cable? It is not uncommon now to hear predictions of a move down to 1.20 in EUR/USD.

Whether or not the ECB will actually cut interest rates remains to be seen. However, should the green shoots of recovery in the business cycle continue to unfold, then there would be little reason for them to cut. But the fact that any tightening in policy is very distant means that interest rates will stay low for a very long time. Anchoring interest rate expectations is key. After all, the BoE’s Bank Rate has been at 0.5% for four years. The market is taking this new communication policy from the ECB as a green light to sell the EUR. A period of further correction on some key EUR and GBP crosses cannot be ruled out i.e. vs AUD, NZD, JPY etc